By Westpac’s Elliot Clarke:

The lack of inflation in early 2015 has provided strong justification for the FOMC to hold off on policy normalisation, despite the unemployment rate signalling a labour market near full employment. Simply, on both a CPI (0.2%yr) and PCE basis (0.3%yr; the FOMC’s preferred measure), annual headline inflation is much closer to zero than the Committee’s medium-term target of 2.0%.

Two key trends have been behind this persistent weakness. Vice Chair Fischer discussed both in his address to the Jackson Hole Symposium on “Inflation Dynamics and Monetary Policy”.

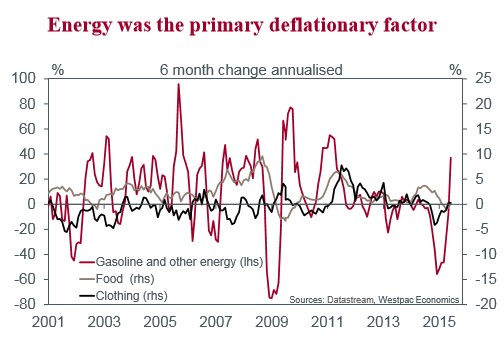

First and foremost, the recent weakness in inflation is, in large part, the result of the sharp decline in the oil price. Having declined by around 60% over the past year (as cited to by Fischer), at July the PCE energy price index was down 15.7%yr after bottoming out at –21.3%yr in January. The oil price effect on inflation has most likely reached its nadir, with positive momentum to be seen (sooner or later) as the oil price partially recovers.

The other key negative influence for inflation over the past year (the USD) has a greater capacity to linger. Vice Chair Fischer gave no specific quantitative estimates on the USD, other than to note that the nominal appreciation since last summer was “about 17 percent”. Fischer instead focused on the immediacy and duration of the impact, noting USD effects are typically “evident within a quarter” and that the bulk of the impact is felt “within one year”. On that basis, the effect of the appreciation to date “could plausibly be holding down core inflation quite noticeably this year”.

While the focus on inflation for policy makers and the markets is typically the annual change in prices, around (possible) turning points, shorter-duration estimates can be quite instructive.

While the annual pace of core inflation (ex food & energy) has been largely unchanged for over six months, shorter-term measures imply a likely acceleration in annual inflation in due course. Notably, anualised six-month inflation has risen from 0.8% six months ago to a more robust 1.7%. This is also true of three-month annualised pace, which has been stable around 1.7% for the past three months.

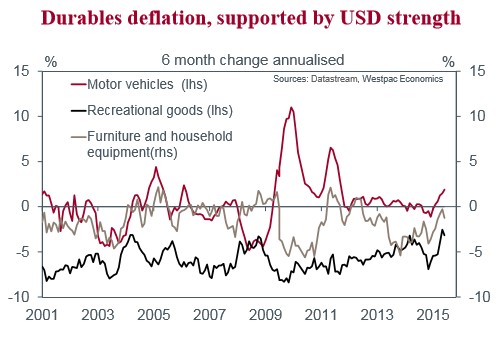

Driving this acceleration in inflation pressures has been an abating of deflation for durable goods and some non-durable items, such as clothing and footwear. A deceleration in food-related inflation has been a partial offset. Given their weight in the consumption basket, and with wages a key contributing factor, services price pressures remain critical to aggregate inflation.

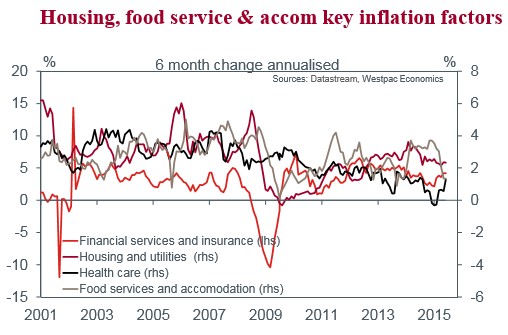

Of the sub-components, housing inflation has remained stable at a solid 2.4% annualised pace through 2015 to date, underpinned by strong tenant-occupied rent inflation (now tending towards 4.0% versus a five-year average of 2.6%) and imputed owner-occupier rent (which is also well above average, currently rising by 3.4% in six-month annualised terms against a five-year average of just 2.1%). Inflation related to medical care has accelerated once again after an early-year lull to be broadly in line with the average pace through the post-GFC period. Also financial services and insurance price gains have strengthened, as have transport costs – the latter despite the sharp decline in the price of energy commodities.

For the FOMC, a labour market at full employment and signs of underlying inflation gaining momentum are arguably enough to start the policy normalisation process. More critically, the pace of rate increases after the first hike will depend on how rapidly inflation accelerates towards the FOMC’s medium-term target. This will be crucial for the outlook for rates and overall financial conditions.