A number of readers have asked me at various times whether now, or now, or now, is the time to buy beaten down mining and LNG stocks. Today there will no doubt be more with the Fed firing up a relief rally overnight, though neither oil nor BHP and RIO benefited overly.

The answer to the question of course depends upon your time frame. If you wish to trade these stocks within the cycle then, sure, BTFD. I suggest you use sophisticated capital management strategies to do it to ensure loss limits and leveraged upside when it comes.

But, to me, a more sensible, less stressful and more realistic approach for those that are not full time traders to be investing in these markets is to ignore the day-to-day noise and invest in the trend. By this I mean see that mining and LNG stocks are caught in a gigantic bear market. The macro settings that are driving it are nowhere near yet resolved, nor are the market dynamics driving the weakness, so the bear will continue.

There are two levels to this “bearishness” (though I’d rather call it downside bullishness). The first is the macro settings that are destroying commodity prices:

- China adjustment to lower and less commodity-intensive growth, and

- a US dollar bull market that will continue irrespective of Fed hikes, adding a monetary headwind to commodity prices.

The second level of bearishness is market dynamics for iron ore, coal and LNG, all of which are entering grotesque periods of oversupply as miners have dramatically miscalculated the above, lumbering themselves with levels of surplus so large that some have to be considered “stranded assets”.

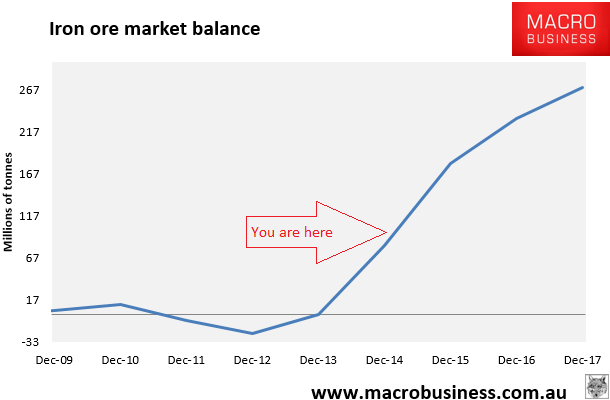

The iron ore surplus is vast:

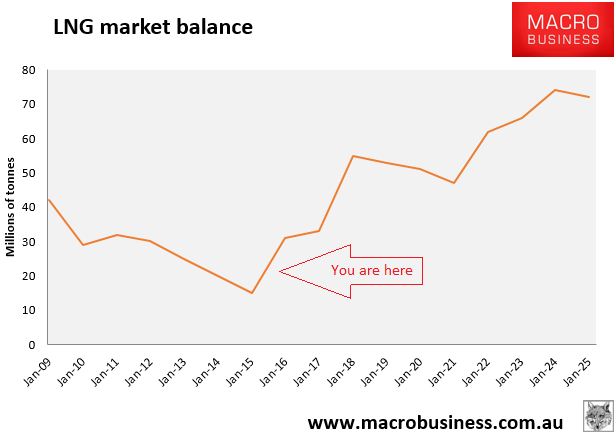

The LNG surplus is vast:

The iron ore surplus is locked in. The second leg in the LNG surplus, from 2021, is questionable given some projects will never be built but it does not change the basic outlook given demand is also going to disappoint.

It’s a little less daunting for the two coals but both remain in oversupply and are chasing falling demand lower.

For iron ore, then, the shakeout has therefore barely started. Within eighteen months I expect:

- all major producer margins to compress virtually to zero;

- all juniors to go out of business;

- FMG to either be dead or a Chinese zombie, and

- majors to eventually cut production as well.

For LNG the challenges are awesome and even longer term:

- Australia’s magnificently expensive seven LNG projects are at the wrong end of the cost curve;

- oil has a long correction ahead of it and no big upside;

- LNG contracts are going to be renegotiated as the spot price crashes;

- marginal cost breakevens will come under pressure and volume cuts will come, and

- massive write downs and equity raisings are in the pipeline.

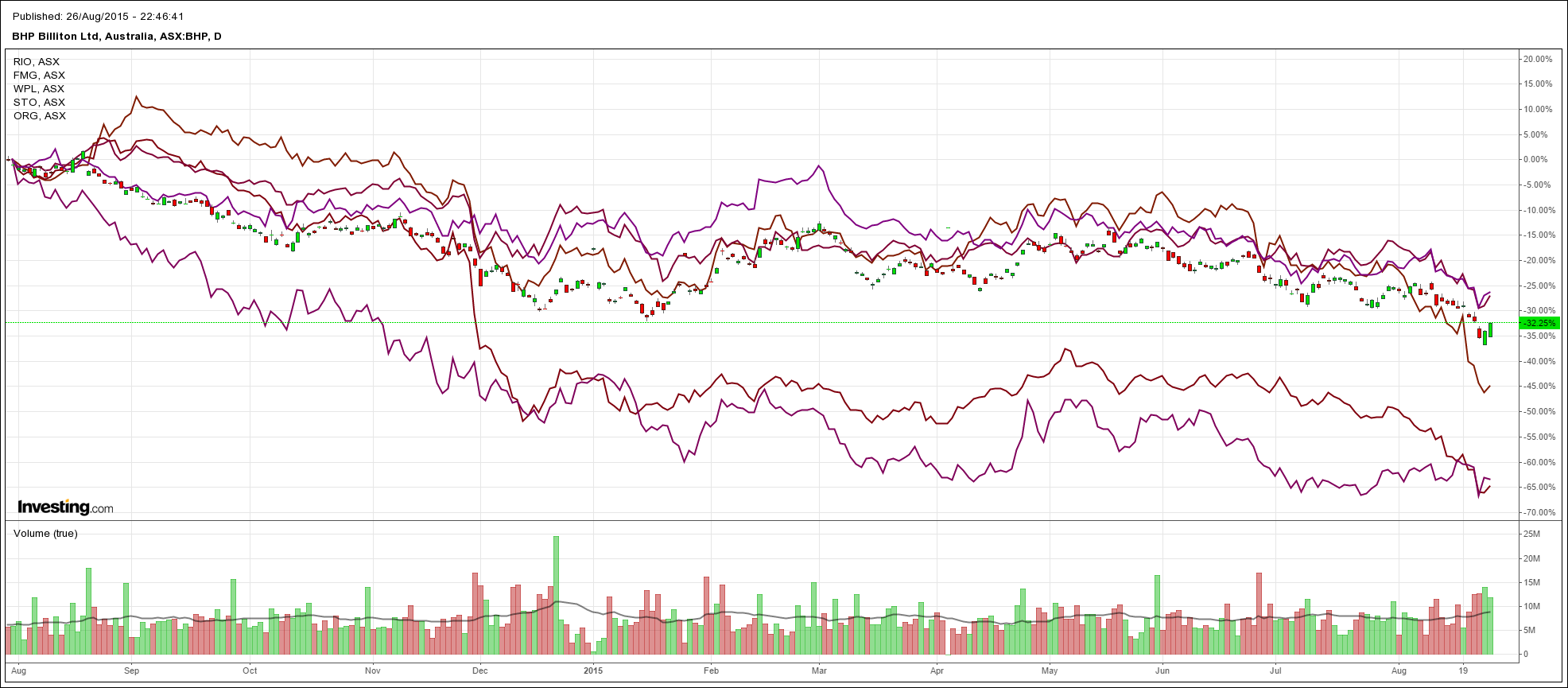

Is it any wonder that we see the following declining trend for all major producers in both commodities?

One final factor should be added. The global economy is very likely headed into its end-of-cycle event in the next eighteen months. It could be sooner, it could be later, but it is certainly visible as China adjusts, the US tightens, Europe squeezes and emerging markets tumble.

My own view is that events look quite likely spin out of control specifically around emerging markets and commodities debt. But one does not have to be that bearish to understand the investment implications for miners and LNG producers. As we head into the next global shock and recession, the above commodity shakeouts will dramatically accelerate as prices crater, volumes evaporate, asset values collapse, debts are written off and equity changes hands for pennies.

To cut a long story short miners and LNG producers are the dot-bombs of the cycle and they are going to go lower than any respectable analyst dare mention. That will be when to buy commodities again and until then the percentage play is to keep adding shorts on any rebound.

Of course given the centrality of mining income to the economy, the same argument can be extended to banks and industrials.