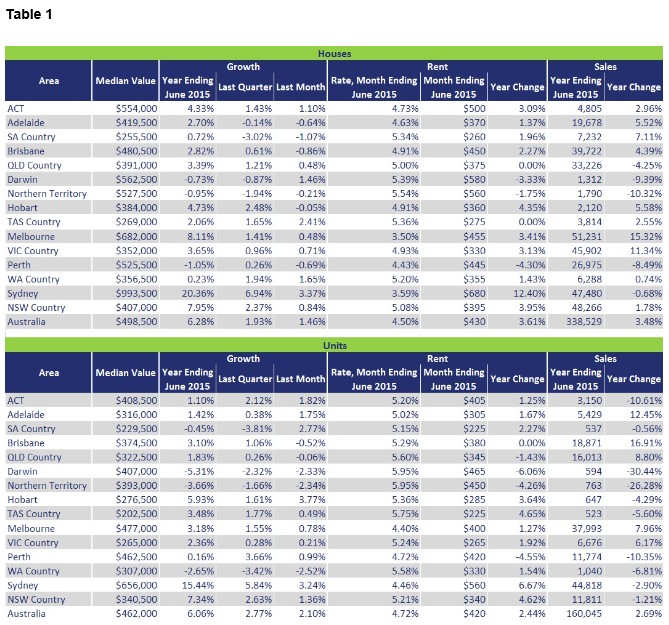

Residex has released its house and unit price results for June, which revealed a 1.46% jump in Australian house values over the month and a 2.10% surge in unit values. Over the year, house values rose by 6.28% nationally, with unit values up by 6.06%:

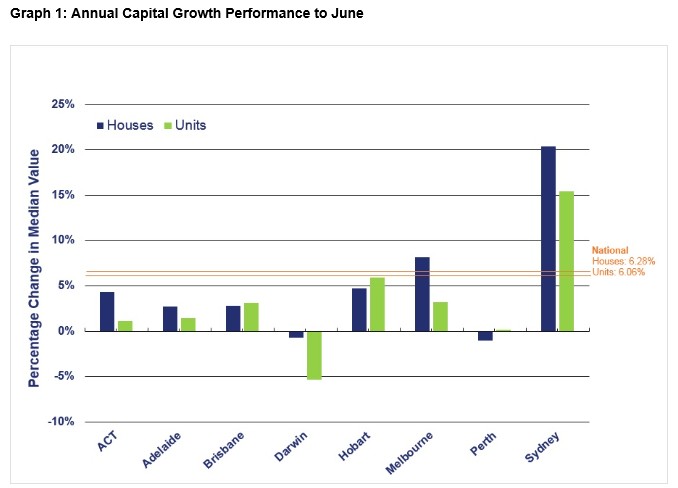

As shown above, Sydney continues to be the primary driver of house values nationally, with values in Sydney jumping another 3.37% in June, and by 20.36% over the year, bringing the median house value there to a whopping $993,500!

Back in April, Residex’s (On-The-House’s) new market analyst, Eliza Owen, described Sydney housing affordability as “a tad ridiculous”. She then followed up in May with an assessment of whether Sydney housing represents a “bubble”, which she seemed to come down in the affirmative.

Advertisement

This month, Ms Owen has provided an analysis of the Perth and Darwin housing markets, which are in the gutter:

The Sydney market is again the clear growth driver. The resource markets – Darwin and Perth – have both suffered a contraction in growth, with the decline in volumes and values of iron ore taking its toll on these markets. The unit market in Darwin suffered the worst contraction in the year to June, falling by -5.31 per cent.

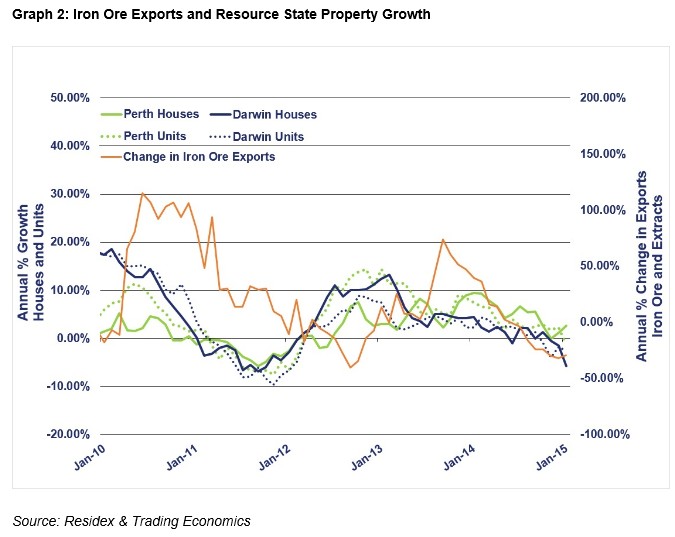

The impact of iron ore exports on the property markets in the resource states can be seen in Graph 2.

Available export data shows the percentage change in the value of exports up to January of this year, compared with the change in values of properties in Perth and Darwin. Unless the resource businesses based in Perth and the Northern Territory can sustain low prices for exports, there is no reason to expect an improvement in these housing markets for the next few months….

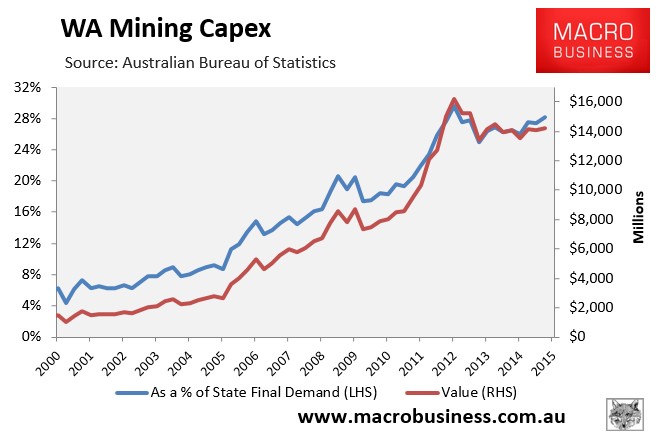

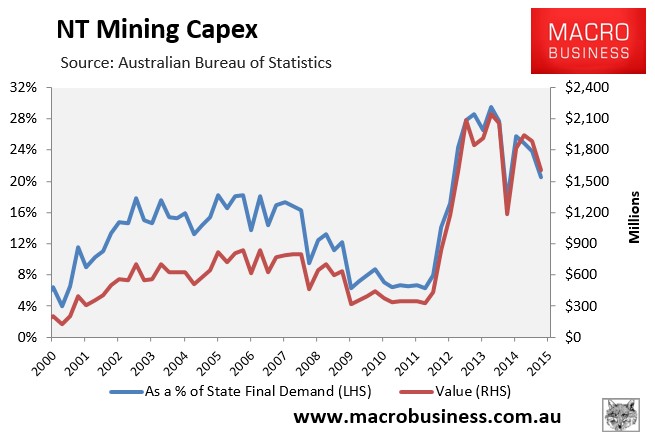

Forget about the next few months, these markets will be hemorrhaging for a few years yet as mining investment collapses from all-time highs:

Advertisement

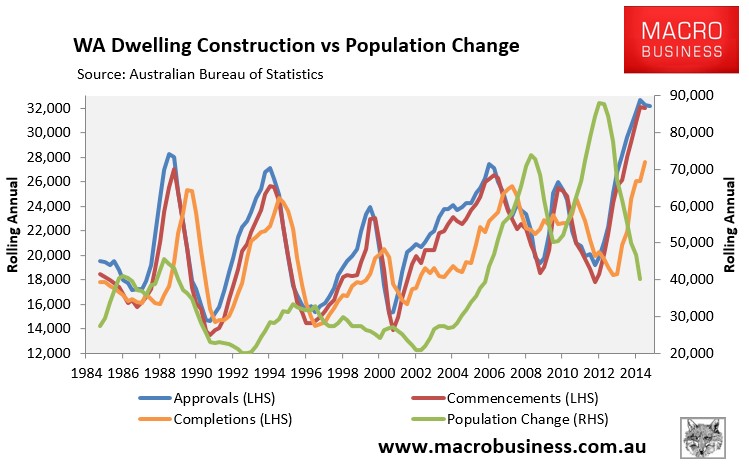

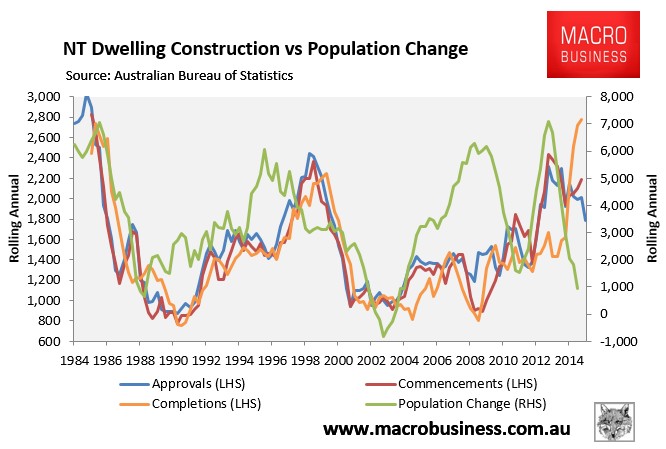

And supply first escalates before dwelling construction slumps as population growth falls:

Advertisement

Ms Owen also claims that there is little evidence of foreign buyers and negative gearing pushing up home prices:

…the Foreign Investment Review Board (FIRB) monitors foreign investment in housing. In November last year, the government reported an inquiry into the FIRB to see how foreign investment impacted property values. The findings revealed that the FIRB had not kept record of the citizenship status of property purchasers, or taken court action against foreign investors since 2006. Without detailed information on who is buying property and how they are doing it, we cannot confidently or academically attribute foreign investment to increased property values…

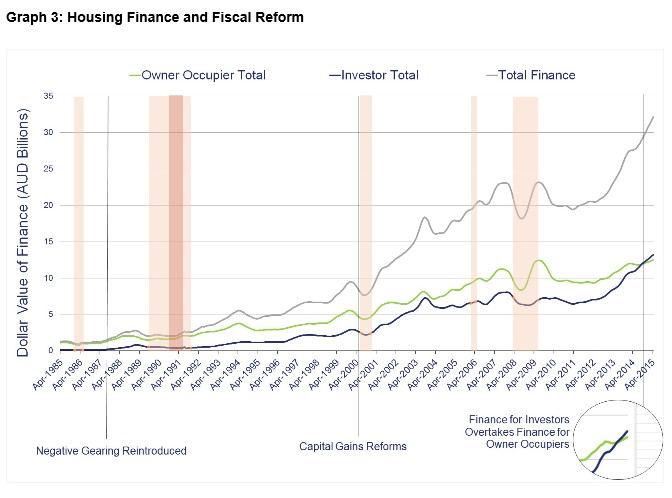

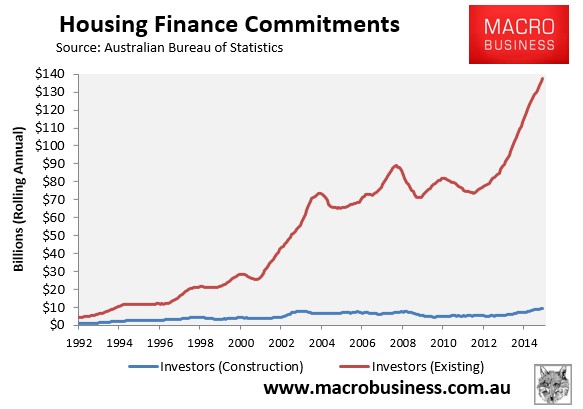

An increase in investors in the housing market suggests that a higher quantity of properties are being traded for investment, because more money is being lent to investors than people buying property to live in…

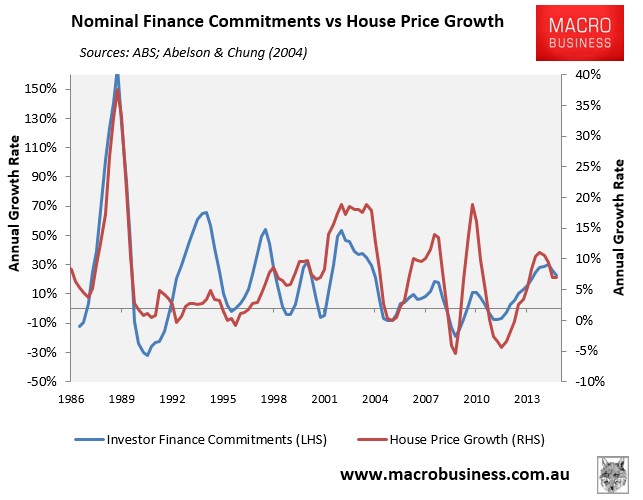

Negative gearing, which allows investors to claim asset losses on their taxable income, was reintroduced by the Hawke-Keating government in 1987. The capital gains concession, which halves the amount of tax to be paid on profit from the sale of assets, was introduced in 1999. By highlighting where these policy changes exist in the time series, it can be seen that they do not seem to have a direct impact on the convergence of investor and owner occupier buying activity.

Also overlayed on Graph 3 are times of economic recession (red) and economic downturn (orange). One could argue that the increase in investment is aided by the tax concessions introduced by the Hawke-Keating government, but that it also has to do with economic performance. Furthermore, the convergence between 2011-2015 between investment and owner-occupation could be attributed to increased overseas investment, or the relaxation of rules pertaining to borrowing from self-managed super funds, which occurred around 2010. It is worth remembering that there is a lag between fiscal reforms and their impact on the market.

Advertisement

Lack of oversight from FIRB and a lack of data on foreign investment is no excuse, and certainly does not mean that we “cannot confidently or academically attribute foreign investment to increased property values”.

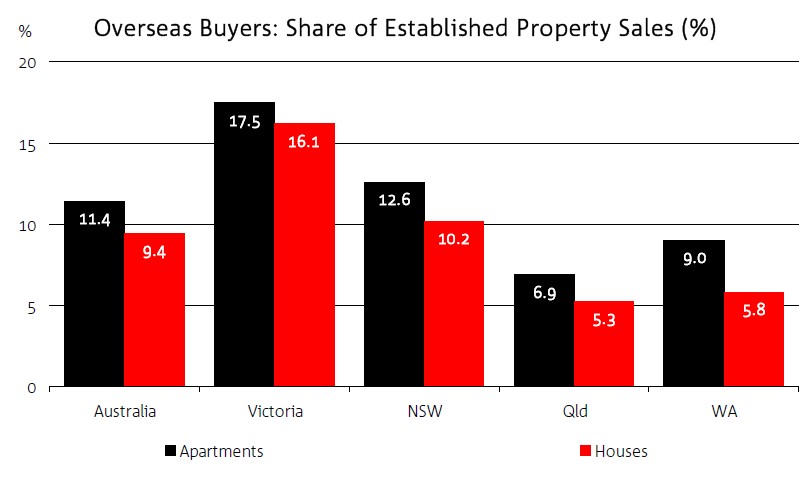

The latest NAB Australian Residential Property Survey showed that overseas buyers are responsible for a significant share of established property sales, particularly in Sydney and Melbourne:

Advertisement

Hence, this added demand is obviously helping to push-up property values and price first home buyers out.

The same can be said for Australia’s negative gearing and capital gains tax rules, which have added extra demand without a commensurate boost in supply:

Advertisement

The correlation between increased investor demand and rising house prices is also clear as day, particularly after negative gearing was reintroduced in the late-1980s, after the CGT discount was introduced in 1999, and currently:

The question that Ms Owen should be answering is this: would domestic and foreign investment (demand) into established dwellings likely be lower if:

Advertisement

Negative gearing losses were quarantined and only allowed to be offset against investment earnings;

The 50% CGT discount was never introduced; and

Australia’s foreign ownership rules were rigorously enforced?

If the answer to these questions is yes, then it is true that foreign investment and Australia’s tax rules have helped to push up Australian property values.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.