From Westpac’s Elliot Clarke:

As the pivotal September FOMC meeting draws ever closer, the magnitude and quality of job gains becomes all the more important. Key from the June post FOMC meeting press conference of Chair Yellen was: (1) her strong belief that labour market conditions had improved markedly in recent years; (2) equally that there was a need to see further improvement in conditions before the process of interest rate normalisation commenced.

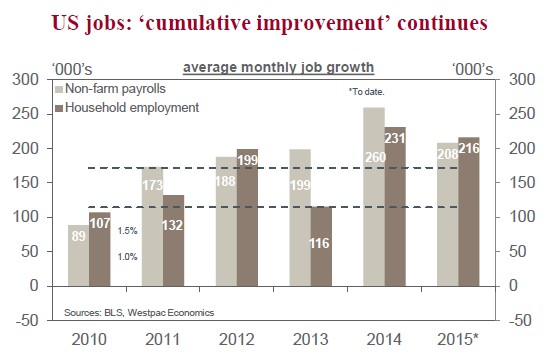

In the June employment report, we find evidence broadly in favour of ongoing cumulative improvement, albeit (continuing the 2015 trend) at a slower pace than was seen during 2014.

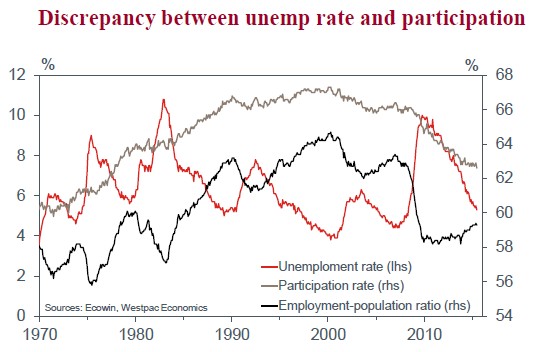

The June nonfarm payrolls result was healthy, coming in at 223k – a touch below market and our own expectations. And the unemployment rate fell to just 5.3%, as the participation rate reversed its May rise – falling 0.3ppts in the month. More important than these spot outcomes is the multi-month trend in job creation and the degree of perceived labour market slack.

Despite the 60k downward revision to April and May, the average monthly nonfarm payrolls job gain for 2015 still stands at 208k. While lower than 2014’s 260k average, it equates to an annualised job gain of 1.8%, well and truly eclipsing population growth over the same period of 1.3%.

With respect to labour market slack, the key benchmark for FOMC deliberation remains the unemployment rate. As noted above, had it not been for the pull-back in the participation rate, the unemployment rate would not have fallen in June. Yet this decline in participation only reversed May’s rise. Indeed, participation is broadly unchanged over the past 18 months. This implies the decline in unemployment over this period was due to job creation, as opposed to the loss of labour force participants.

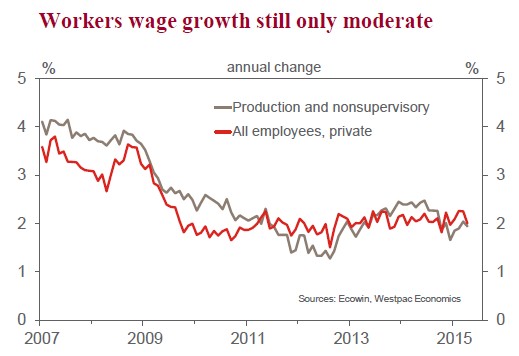

Further, at 5.3%, the unemployment rate is just 0.1ppts above the FOMC’s ‘longer-run’ forecast – effectively the unemployment rate they belief is consistent with ‘full employment’. Together with ongoing robust gains for employment in excess of population growth, this lack of immediate slack gives rise to concerns over the potential for wage and inflation pressures to build, even though both clearly remain absent at present – note that average hourly earnings were unchanged in June, and up a moderate 2.0%yr.

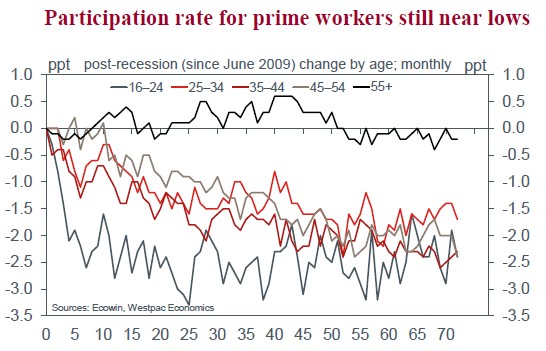

The apparent tension between seemingly full employment and relatively soft nominal wage gains is resolved when one considers the other major measure of slack: the employment-to-population ratio. Having been brought to historic lows not only by the job losses of the post-GFC recession but also by the sharp decline in participation to end-2013, it has only edged higher since. This result implies there remains a large pool of marginally-attached workers which could be brought back into the labour market, if conditions were favourable. That many of these could-be workers are in primeworking age groups highlights both their availability and potential productive use by the economy.

For the FOMC, the challenge is to continue to foster healthy job gains without causing the returns that firms receive from employing to be depleted by wage pressures. Consequently, having seen the unemployment rate fall to 5.3% and given job gains are continuing, conditions are conducive to begin interest rate normalisation.

Through this data-dependent (likely very slow process), committee members aim to foster further sustainable growth in activity and jobs, incentivising participation and productivity. A September commencement and cautious normalisation remains most likely.