By Westpac’s Elliot Clarke

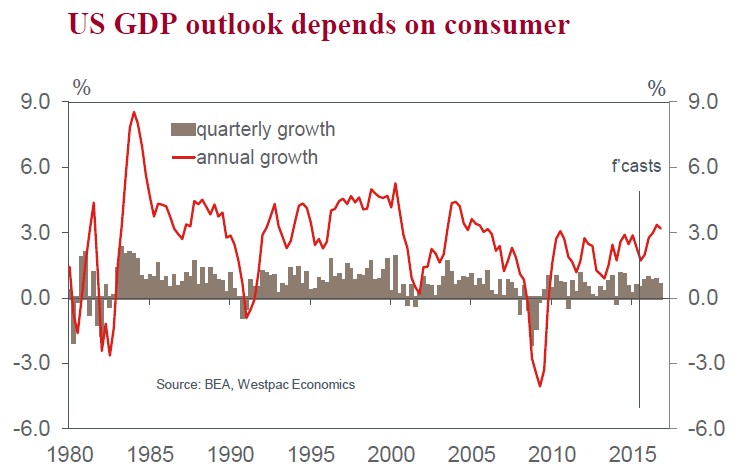

US GDP rose at a solid 2.3% annualised pace in Q2, much as expected. Household consumption drove the result, with momentum strengthening from Q1’s 1.7% annualised pace to 2.9% as durables and non-durables growth improved with the weather. Growth in services consumption was more modest at 2.1%, unchanged from Q1. While an improvement on Q1, it is worth highlighting that the Q2 growth pace for total consumption is still well down on the 3.9% average of the nine months to Q4 2014, largely due to the absence of stronger momentum in services.

Back revisions to recent quarters of residential investment brought it more into line with the momentum apparent in permits and starts; annual growth at Q1 is now reported as 8.4%, up from 5.5%. These gains continued into Q2, with annual growth robust at 7.5%yr.

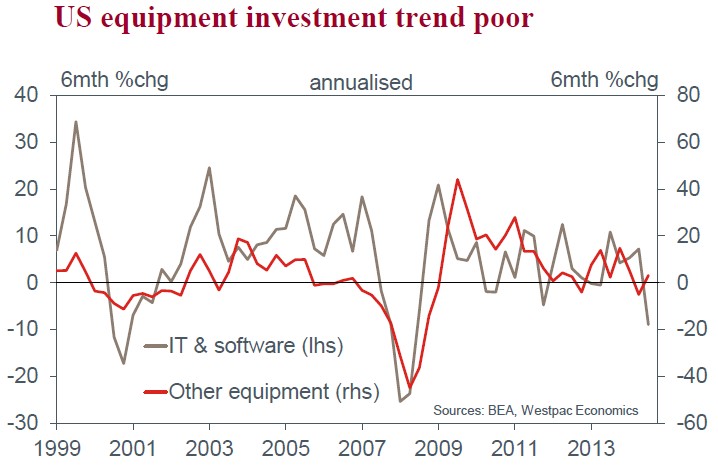

Q2 was a weak quarter for business investment: structures spending edged down to be –1.7%yr; of greater concern, equipment spending fell at a 4.1% annualised pace in Q2, leaving annual growth at just 2.1%. Contrasting this result to the recent 10.2%yr peak of Q3 2014 highlights how weak business investment currently is. Arguably, this is a function of the weaker oil price and stronger USD, but is also due to the continued preference of firms to manage their financial efficiency to boost profits rather than

expand capacity in search of greater revenue.

Public spending and the external sector provided next-to-no support for growth in Q2, and this will likely continue. But, of concern for headline growth in H2 2015, inventories grew at a rapid rate for a second consecutive quarter. Typically strong inventory builds give way to a draw down, dragging headline growth lower.

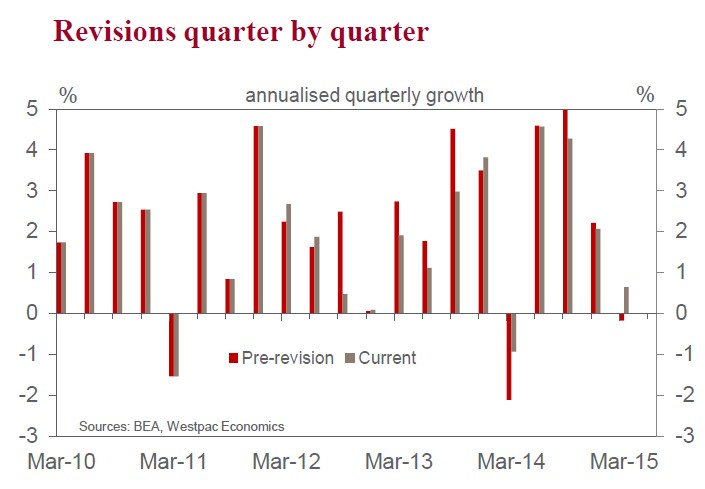

In our preview ahead of the Q2 release, we highlighted the substantial volatility apparent in recent estimates of GDP. Taking Q1 2015 as an example: while the first GDP estimate printed at +0.2% annualised, it was subsequently revised to –0.7% in the second estimate, then to –0.2% in the third. As part of the annual revision process, it has now been revised to +0.6%, leaving first-half annualised growth at 1.5%.

Changes to seasonal adjustment resulted in Q1 2014 also being heavily revised, from –2.1% annualised to –0.9%. However, because offsetting adjustments were made to surrounding quarters, the net impact of this change on the level of activity was negligible.

In contrast, the changes that came as a result of the inclusion of new source data were significant, with growth over the past three years revised. While year-average growth in 2012 edged higher to 2.3%, growth in 2013 was substantially revised down, from 2.2% to 1.5%. This outcome came as a result of downward revisions to state & local government spending (revised down in all three years); household consumption; and residential investment. Growth in 2014 was retained at 2.4%, but could well be revised later.

The prime consequence of the revisions to the previous three years is that, through that period, growth is now estimated to have risen at a 2.0% average pace, down from 2.3% previously. Hence, through a period of rapid employment growth; low interest rates; and wealth creation, the US economy was only able to grow at a pace consistent with the low-end of the FOMC’s current long-term (i.e. trend) expectation of 2.0–2.3%yr. While we anticipate growth will strengthen in late 2015 and into 2016, the past three years suggest the US economy is unlikely to sustain a growth pulse well in excess of trend for long, mitigating wage and inflation pressures, and limiting the need for policy makers to act.

This is not a topic on which the FOMC and Fed are uninformed. The FOMC’s long-term projections have been edged down in recent years towards 2.0% at the lower bound; also, as highlighted by the (well timed) accidental release of the Fed staff forecasts (distinct from FOMC members) from the June FOMC meeting, we know that their estimate of ‘potential’ is below 2.0% out to 2020. The absence of robust growth raises a clear question over whether the FOMC’s longer-term Fed Funds rate projection of 3.75% can be attained.

From our perspective, while we expect the FOMC will seek to get on the front foot and commence the normalisation process in September then follow up with but a short delay, our expectation for the peak in the Fed Funds rate is only 2.25–2.50% out in September 2017. Given the experience of the past three years, we would further argue that the risks to this forecast are to the downside, with the economy highly sensitive to rate increases.