As the day wears on the RIO share price wears with it, now down the better part of 3%, matching London.

I put it to you that this is just the beginning. RIO may be the cheapest iron ore producer in the world but iron ore is about to spend several years being given away for free, more or less, so that’s going to be much comfort.

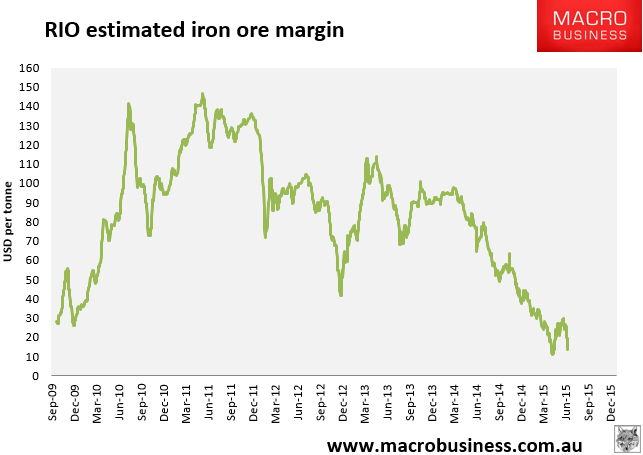

RIO’s all-in break even price for iron ore is $35-40. Cash cost is much lower and as such RIO will be the last to be shutting in volumes which is some comfort. I’m using $36 in my charts today so its margin looks like this:

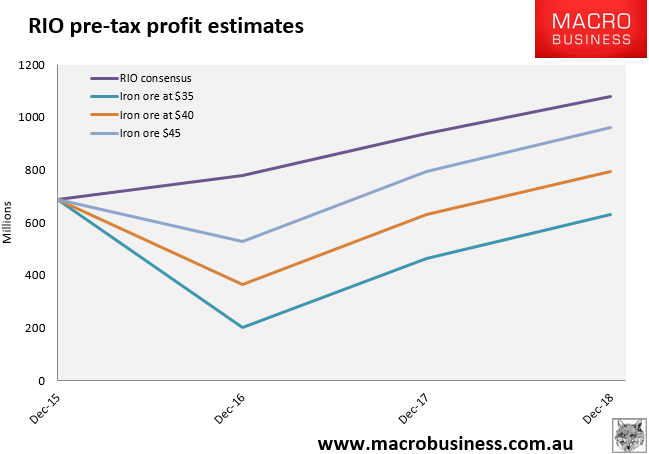

Not a very pretty trend and about to get worse. Here’s are some iron roe scenarios for RIO profits:

The forward years assume a $5 per tonne cost reduction and the assumptions for RIO’s other divisions are also pretty generous. This does not include any write downs which are surely going to have to come given the massive capital mis-allocation into over-capacity that has occurred. Consensus is pricing RIO off an assumed iron ore price of roughly $55.

With a P/E around 10 and change and a dividend around 5% (more grossed up) it may seem appealing but you have to recall that this is a highly cyclical stock and its capital value is going to continue to compress as the commodity super cycle unwinds. Dividend mining in miners is a very stupid idea. Look to a utility.

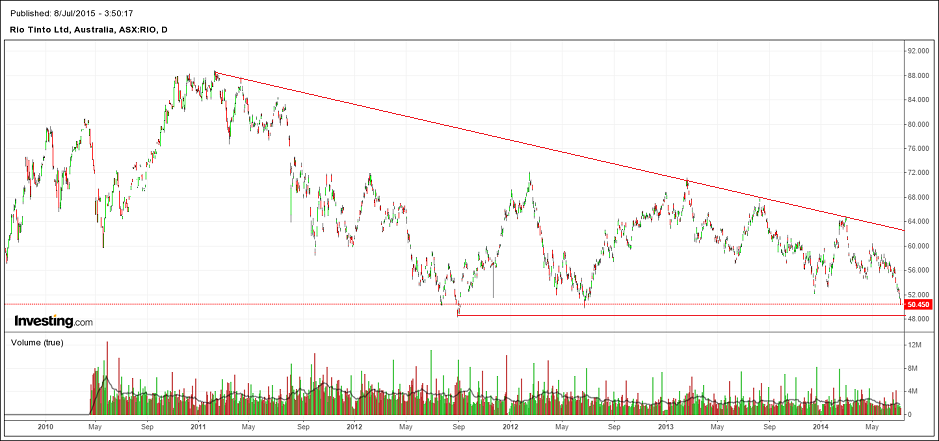

Technicals too are not encouraging. The daily chart has just one support between it and free fall and that really is one the most impressive bearish descending triangles that I can recall:

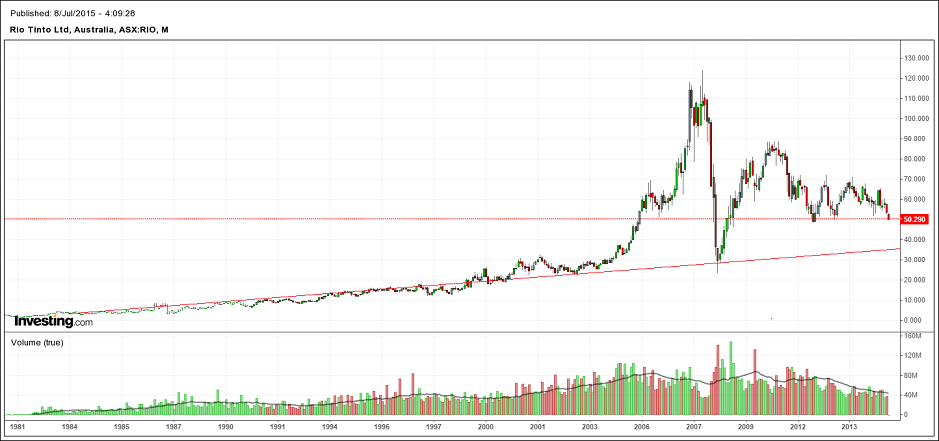

Terminal support is in the mid to low $48s. To give us a downside target let’s turn to the monthly chart:

The really long term trend comes in around the mid $35s. That seems a good target a few years down the track after we’ve overshot to the GFC low in the bottom half of the $20s for a while.