Another dubious report out today from an economic consultancy engaged in a rent-seeker’s fight. This time it’s Port Phillip Partners and the customer is RIO and the Minerals Council:

The Australian iron ore industry has capitalised on a decade of unprecedented volume and price growth to create a market position stronger after the commodities boom than it was before. Australia now has a 50 per cent share of the seaborne market, a share built on vastly expanded production volumes which now exceed 650 million tonnes per year. This compares with 170 million tonnes in 2000.

This will enable the industry to add more value to the Australian economy over the next decade than over the previous 10 years. The iron ore industry is likely to contribute more than A$600 billion to the Australian economy over the next decade. With continued attention to competitiveness and productivity, iron ore represents a robust wealth generation machine for the nation, even at long-term average prices or below.

Three major points need to be considered: a) The actions of the Australian iron ore sector are not the only, and not even the major, drivers of iron ore prices. Iron ore trades in a global commodity market which behaves as global commodity markets always do – a sharp increase in demand followed by a rapid increase in commodity prices, an investment-driven supply response, and finally price declines as demand slows and costs are taken out across the board. This has been repeated across other commodities – copper and coal, for example, but also in agricultural commodities – and for the same reasons.

b) The actions of the Australian iron ore industry over the past decade have been exactly right from a national interest point of view. Expansion has lifted Australia’s seaborne market share to 50 per cent, at a time when competitor nations have eroded Australia’s share in other commodity markets. The core of Australia’s iron ore sector is robust. Despite industry-wide cost reductions, more than 80 per cent of Australian capacity is in the bottom half of the global cost curve and will continue to generate strong operating cash flows. Even if growth continues to slow, Australian iron ore will remain a powerful wealth generator for Australia. The annual level of activity in the iron ore sector from ongoing operations alone is now much greater than even investment-driven activity over previous years.

In addition, iron ore employment contributed A$45 billion to the economy over the past 10 years, and will contribute A$78 billion over the next 10 years. This is based on a very conservative analysis that includes modest consensus price forecasts and an assumption of no future growth.

c) History shows market intervention through government policy action is likely to be ineffective at best and counter-productive at worst. History suggests that the burden of proof is very high for market intervention as a policy lever to control price. In other industries, Australia has unwound virtually all previous attempts at controlling price through centralised marketing. Controlling production of iron ore has failed in the past – export controls introduced by Australia in the 1970s led Japan to support Brazilian iron ore investment instead of Australian.

A superior approach is to focus on policies that allow all operators to compete successfully in the global market, and to make their businesses sustainable against a wide range of potential prices, not only those at historic highs. These policies are focussed on free and open markets for trade internationally, competitive markets for goods and services supplied in Australia, workplace cultures that support productivity, wise investments in people and infrastructure and stable and competitive tax and royalty arrangements. Australia’s iron ore resources are globally significant assets. An ongoing focus on these policies will ensure a strong contribution from the industry in the decade to come.

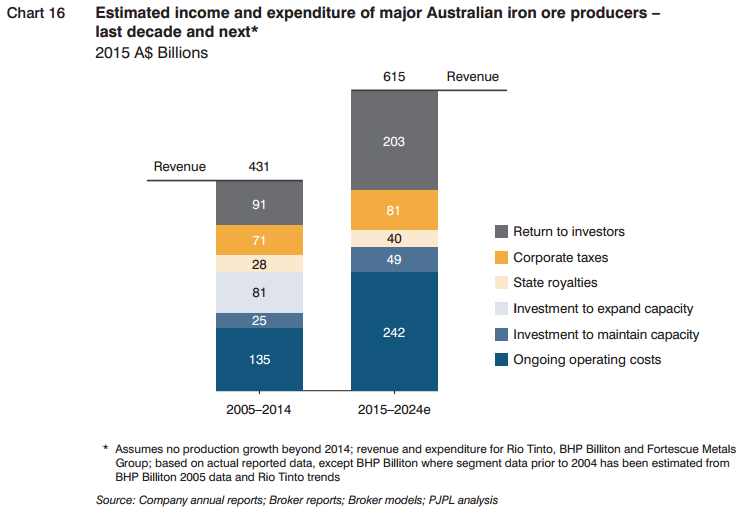

The conclusions are basically right but the outlook is drivel. This chart of hilarious:

The assumption for this glowing outcome is a $72 iron ore price and a 0.78 Australian dollar. The reality is going to be more like half that price with a currency that is materially lower but nowhere near enough. If we plug in $36 and a 60 cent dollar we get roughly $380 billion for 2015-2014 aggregate revenue and every sub-component collapses.

As I say it doesn’t impact the outcome of the arguments. You’re still better off letting high cost production go out of business. But the report makes RIO look an awful lot more competent and magnanimous than is the reality. Full report.