By Chris Becker

Second quarter GDP for the US came in weak at 2.3% (vs 2.5% expected) with the first quarter revised higher, just enough for the Fed to see the US economy is “back on track”, but US stocks were flat as the USD rose in response. In Europe, the only important releases for the ECB – German CPI and German unemployment – came in flat, which gave European stocks a lift and bonds were bid snapping their losing streak. The commodity deflation train continued to roll on…

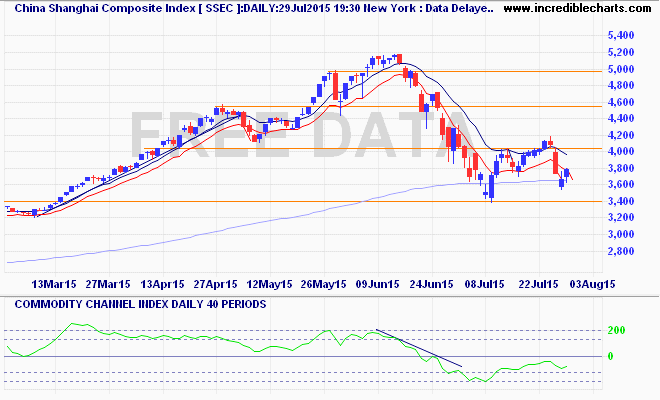

Volatility continues to confound the Shanghai Composite with a 2% loss after the previous 4% gain. Now just above 3700 points, and right on the 200 day moving average, this is still well below the critical 4000 point resistance level as a broad trading range is starting to develop here. Those who want to be brave and go long need to watch that 4000 level, shorts the 3500 long term support: