By Gavin Putland, cross-posted from the Land Values Research Group:

The McKell Institute’s report on negative gearing (Richard Holden, Switching Gears, June 2015) concluded that negative gearing for future investors should be allowed only for new homes. I have been pushing that idea since 2003. But the McKell report, in its account of the Hawke-Keating government’s brief quarantining of negative gearing (based on contemporary reports in the Sydney Morning Herald and the Sun-Herald), reveals that the idea dates back at least as far as 1987. I quote from pp.21–22:

Treasurer Paul Keating insisted at the time that the overwhelming factor deterring potential investors was high interest rates, needed to counter high inflation. By December 1986, the interest rate on loans to building societies had reached 15.5%, with NSW particularly hard hit, as new dwelling commencements decline [sic] by some 28% on the previous year.

By February 1987, the Real Estate Institute (REI) of NSW joined the HIA in blaming [disallowance of] negative gearing for contributing to a “rental crisis” in Sydney. …

In March, the Master Builders Federation of Australia released figures showing that Sydney rental prices had skyrocketed by 25% in the previous 12 months. …

By April, BIS Shrapnel released data showing that the level of new dwelling constructions had plummeted to a 10 year low….

By June 1987, the Liberal Party announced that if elected, it would replace Labor’s prohibition of negative gearing on rental properties with a system allowing deductions from taxable income on interest incurred on borrowings up to 80 per cent of the value of the rental property.

This received immediate support from the Confederation of Australian Industry (CAI) and the NSW REI, but was sternly criticized by the Tenants Union (TU) of NSW.

TU spokesman Tracy Goulding… argued that “These taxes aren’t directly responsible for the housing crisis. The rental crisis is an ongoing thing…”

Nevertheless, the Coalition began to ramp up its attacks on negative gearing as contributing to higher rental prices and longer public housing waiting lists. …

In August, the NSW REI released new figures which showed that Sydney rental prices had increased by 66% in the previous 12 months…

That apocalyptic claim is not supported by ABS figures. Nor is it clear how the Liberal Party’s proposal would have alleviated the construction slump when the tax deduction was not tied to construction. A clearer solution came from elsewhere (pp.22–23, my emphasis):

At this point, the West Australian Government began lobbying the Prime Minister to reform negative gearing so as to reintroduce it but for new housing only. … The acting WA Premier, Mr Mal Bryce, said that the shortage of private rental accommodation was a major concern in the community, but also urged the government to not reintroduce the incentive for existing houses on the basis that it would drive up prices….

Under growing pressure from his political base in NSW, the Treasurer began to consider several options for reform, including:

- Allowing investors to claim interest expenses against gross rental income before deduction of operating expenses, which would allow more interest to be claimed as a tax deduction and increase returns to investors;

- Allowing interest costs on up to a set percentage of borrowings, effectively setting an equity limit below which the negative gearing rules would not apply;

- Setting a borrowing limit on interest deductibility; and,

- The West Australian Premier’s proposal to restrict negative gearing to new supply.

In September, Treasurer Paul Keating took to cabinet a proposal that would allow investors to claim interest expenses as a tax deduction against gross rental income… but cabinet was split and no decision was made.

Note that Keating’s proposal, like the Liberal Party’s proposal, was not tied to construction! The rest is history (p.23):

Eventually, the Treasurer’s preferred approach was rejected, and the Government revealed that it would reinstate negative gearing in its entirety.

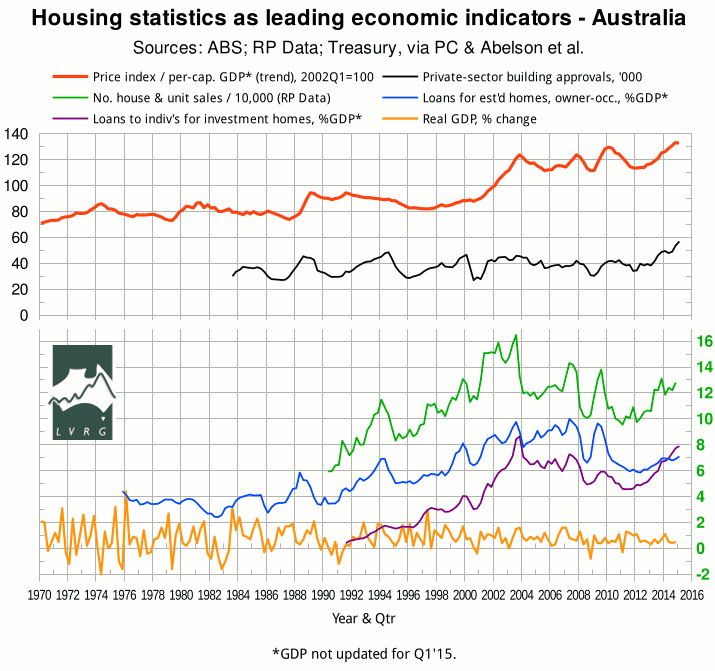

The reinstatement of full negative gearing coincided with the minimum in the house price index (red curve) in the following graph. Next month, the stock market crashed. In the new year, house prices entered bubble territory.

And in 1989 the bubble burst, together with its companion in commercial property — giving us the recession we had to have, turning Keating’s surpluses into deficits, and trashing his place in history.