Another day, another spurious defence of negative gearing and the 50% CGT discount. This time from The Australian’s Henry Ergas, who has written a vitriolic piece attacking the Grattan Institute’s John Daley and Daniel Wood. Let’s take a look at his key points.

First, tax efficiency:

To repeat, for the benefit of the children: if owner-occupied housing is tax advantaged, then rental housing should be too, or investment decisions will be distorted, as will the choice between renting and buying. And the taxation of capital gains is no exception to that rule.

To say that is not to deny that optimal capital gains taxation can be complex. But in this case, the economics are straightforward. If the capital gains tax on owner-occupied housing is set at zero, then “production efficiency” — the situation in which society’s resources are put to their best uses — requires that capital gains on rental properties also be taxed at a low, if not zero, rate.

Funny how Ergas mentions the difference in how capital gains are treated under owner-occupied housing and investor housing, but fails to also mention that investor loans are tax deductible (and would remain so if negative gearing was quarantined), whereas owner-occupied loans are not.

Is Ergas suggesting that owner-occupiers should be able to deduct mortgage interest in the same way that investors can? If not, his arguments about tax neutrality make no sense.

Further, if Ergas is really interested in ensuring that “the choice between renting and buying” is not “distorted”, shouldn’t he be advocating for the actual renters to receive the tax benefits, rather than the owners of the rental stock?

Next, Ergas tries to make the point that negative gearing and the CGT discount boosts housing supply:

On this too, our authors express themselves in fine Jabberwockian form; but the essence of their claim is that all negative gearing does is reshuffle the ownership of the housing stock, increasing the price of existing housing in the process.

That can only be true, however, if the supply of housing does not eventually respond to price rises: otherwise, the greater demand caused by negative gearing will induce an at least partially offsetting expansion in the housing on offer…

Rather, as Daley and Woods agree, the supply of new housing, particularly in Sydney, has been constrained severely by zoning laws and by restrictions on land release. But it is absurd to suggest, as Daley and Woods do, that one should respond to those constraints by repealing negative gearing: that would do nothing to make the Sydney housing market more efficient, while making housing markets less efficient, and increasing rents, everywhere else.

Indeed, that has been the experience in the US, which largely abolished negative gearing in 1986 and has faced a rental crisis since…

Righto, so under Australia’s sluggish planning system, negative gearing raises investor demand and pushes up prices. But this is okay, because the rise in prices will illicit some moderate supply response?

Seriously Henry, I wholeheartedly agree with your view that the supply-side of the housing market needs to be liberalised. But until this is done – which let’s face it is highly unlikely – it makes absolutely no sense to continue stoking demand and forcing-up prices. You seem to believe that only the supply-side sets price. When the truth of the matter is that it is the inter-play between both demand and supply that does so.

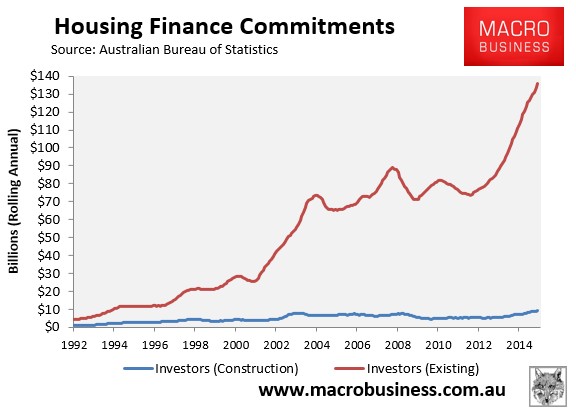

Moreover, you claim that removing negative gearing would somehow make the housing market less efficient and push up rents, even though it has been proven time and time again that more than 90% of investors buy established homes, thus they are not actually boosting rental availability and affordability:

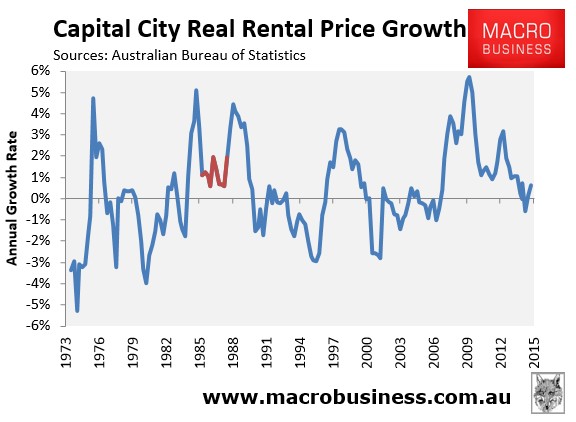

It has also been proven that there was no adverse rental impacts when negative gearing was temporarily quarantined between 1985 and 1987, with higher rental growth experienced both before and afterwards:

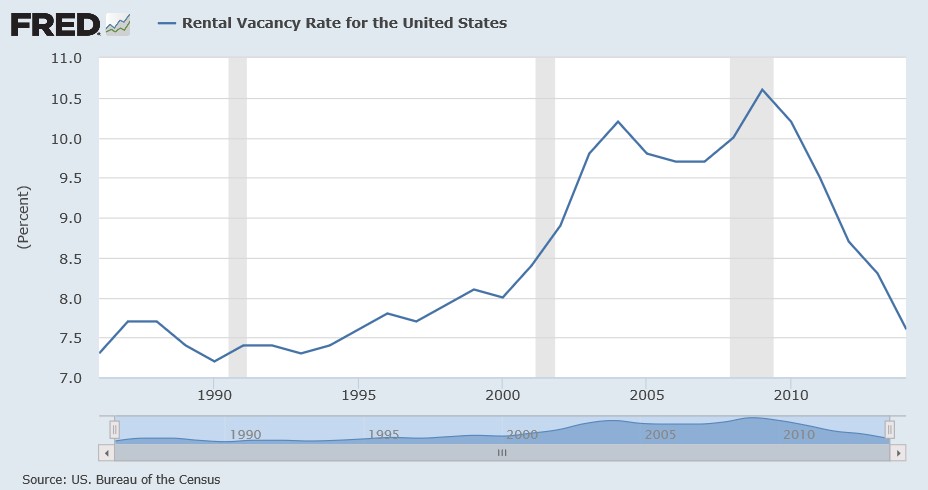

Finally, your argument that the US has “faced a rental crises ever since” it “largely abolished negative gearing in 1986” also doesn’t pass the laugh test given the US’ rental vacancy rate has remained above 7% throughout this entire period (see next chart) and is more than three times higher than Australia’s, which of course has negative gearing. The US rental vacancy rate is also higher today than it was in 1986, despite the Great Recession smashing new home construction.

QED.