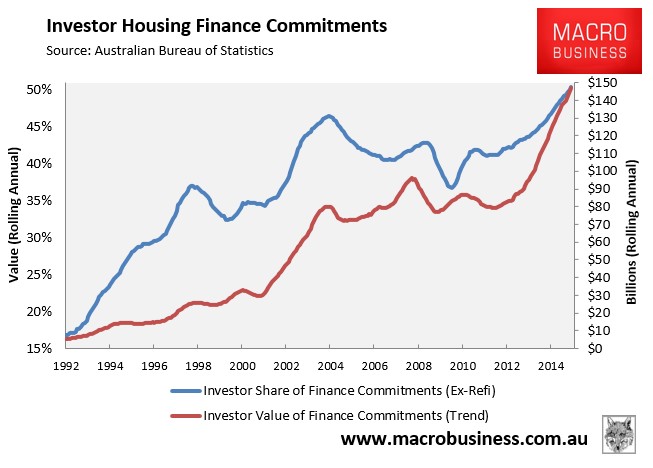

The vice is tightening around Australia’s property investors.

First it was Westpac Bank, which announced that investors would need a minimum 20% deposit in order to secure a new investor mortgage.

Then, as reported yesterday, ANZ Bank lifted its home loan rates on all variable investor mortgages by 0.27% and by 0.30% on new fixed investor mortgages in response to APRA’s 10% speed limit on investor credit growth.

And following in ANZ’s footsteps, the nation’s biggest mortgage lender, Commonwealth Bank, quietly announced yesterday that it would do the same.

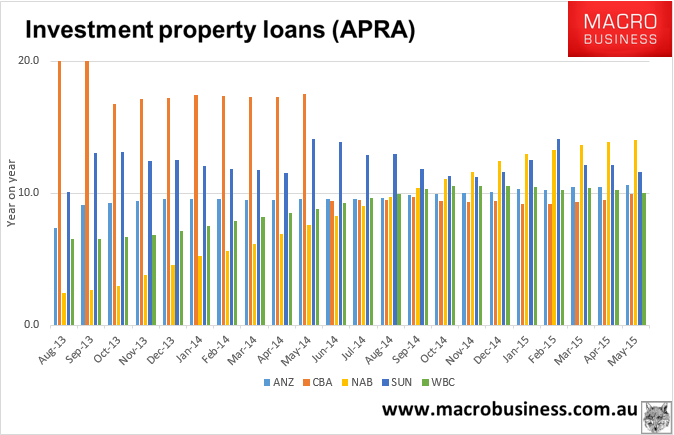

So that’s three of the big four lenders introducing new measures to clamp down on investor mortgage lending in response to APRA’s guidance and threat of regulatory action.

According to ANZ Australia chief executive, Mark Whelan:

“[The policy shift] certainly related to some concerns I think in the marketplace by APRA, and I think a lot of the market participants of the growth in investor lending but that’s not the primary reason we moved.

We made this decision based on looking at the mix of our investor lending and our owner-occupied lending in our books so we want to get more of the owner-occupied lending and slow down a bit of the investor lending”.

Nerida Cole, managing director of Dixon Advisory’s financial advice arm, also believes that the banks have tightened their lending criteria recently in a range of ways, which could act to further slow the rate of investor mortgage growth. From The AFR:

“People who are more restricted with cash flow might find that the income that was previously considered [adequate] for obtaining investment loans is now heavily discounted,” Cole says. “This means it will hold less weight in the bank’s assessment of your risk potential”…

CBA and Westpac, for example, have reduced the weight rental income has on its loan calculations by 40 per cent, Cole says, while ANZ no longer counts negative gearing towards lenders’ ability to repay their loans…

Dixon Advisory’s modelling shows the amount of additional cash an investor could expect to be asked to hold to cover a $500,000 loan might be between $10,000 and $12,000…

Previously a borrower with a $500,000 loan and 20 per cent deposit would have reasonably been expected to prove cash flow of about $8600 a year before loan approval, after factors like rental income and negative gearing were accounted for. Dixon’s modelling shows that sum jumps to almost $21,000.

For a $1 million loan, the expected additional cash flow could be as high as $22,000 under the new standards, a leap from $14,700 to $36,870.

What is interesting here is that both CBA and Westpac are already behind APRA’s 10% investor loan growth line in the sand:

It appears APRA is suddenly being taken quite seriously, perhaps even more than the headline 10% line suggests.

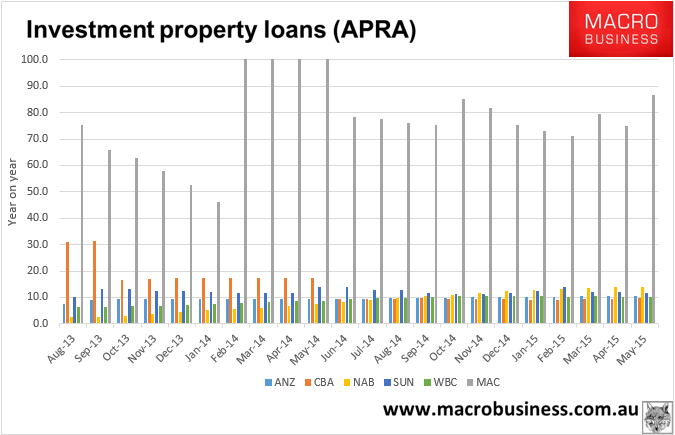

Except, of course, at Macquarie Bank which operates with no rules at all:

As I noted yesterday, we are possibly witnessing the beginning of the end for the great investor bubble: