PIMCO, the world’s biggest bond manager, has released a new report looking at Australian household debt, which raises the alarm bells and joins the chorus of commentators calling for stronger macro-prudential controls on mortgage lending:

…common metrics of household leverage and house price valuations remain elevated in Australia, particularly compared with those in other developed markets…

This complicates the RBA’s reaction function when setting policy by introducing financial stability risk…

Households often decide to incur debt to finance assets that will provide a future expected payoff and maximize their net worth…

The problem is that expected future capital price gains may become unrealistic when extrapolated from recent history (“irrational exuberance”), leading to excess borrowing, which, when unwound, can lead to large negative externalities…

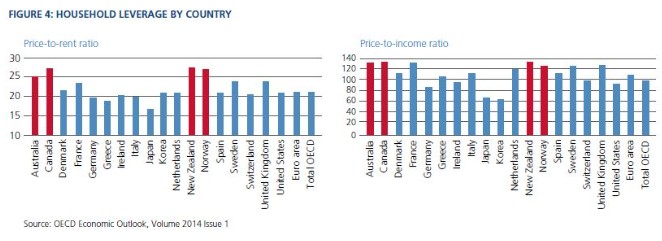

Based on data from the OECD (2014), two commonly used valuation metrics place Australian house prices at the higher end of international comparisons, as seen in Figure 4. With this starting point, it seems questionable to embed expectations of continued high price growth…

[Our] modelling results reveal that asset prices and mortgage rates largely explain the change in household leverage. These two factors appear to dominate all other variables regardless of how significant they are individually.

From this we infer several probable outcomes in Australia:

• Households’ decision to incur debt is dominated by the cost of debt (the mortgage rate) and recent asset price appreciation, which may not be sustainable or linked to the productivity of the asset.

• Of concern, households are exhibiting irrational exuberance because they are placing little weight on broader fundamentals like unemployment that may be more representative of future incomes or asset price returns, increasing the likelihood of asset price bubbles.

• Australian households appear to respond rather quickly, needing only two quarters of favourable changes in asset prices and mortgage rates to increase leverage.

• Australian households will react faster and more vigorously to a shock in asset prices or mortgage rates. This could result in a feedback loop where falling asset values induce further deleveraging.

Based on our model for household leverage alone, if an exogenous shock sparked a deleveraging cycle in Australia, it would be expected to be quite severe given the larger co-efficient for asset prices and the quicker household response…

We believe macro-prudential measures should be strengthened to address financial stability risk and give the RBA maximum flexibility when setting policy for the aggregate economy.

That’s a stern warning if ever I have read one, and I couldn’t agree more.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.