As summarised earlier, the Australian Bureau of Statistics (ABS) today released the national accounts for the March quarter, which registered a 0.9% increase in real GDP over the quarter and a 2.2% rise over the year. The result beat market expectations of 0.7% growth over the quarter and 2.1% growth over the year.

On a per capita basis, real GDP rose by a solid 0.6% but was up by only 0.8% over the year. More importantly for living standards, real national disposable income per capita fell by 0.1% over the quarter and was down 1.6% over the year.

According to the ABS, seasonally adjusted growth for the quarter was driven by:

- a 0.5% contribution from net exports;

- a 0.3% contribution from household final consumption expenditure;

- a 0.1% contribution from government final consumption expenditure;

- a 0.3% contribution from changes in inventories; and

- a 0.2% contribution from total dwelling construction; partly offset by

- a 0.4% detraction from non-dwelling construction;

- a 0.1% detraction from Machinery and equipment; and

- a 0.1% detraction from Public gross fixed capital formation.

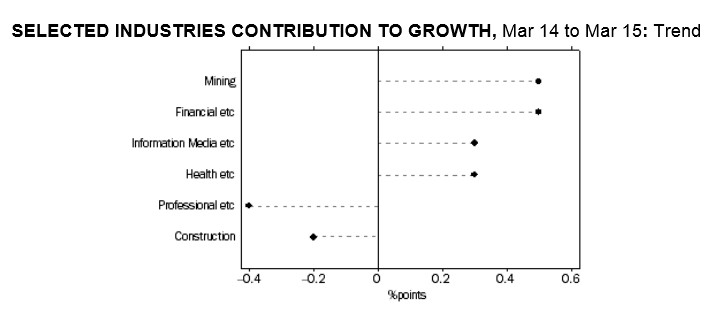

Reflecting Australia’s houses and holes economy, the main contributors to GDP growth over the year in trend terms were Mining (0.5%) and Finance & Insurance (0.5%), whereas the main detractors from growth were Professional, scientific and technical services (-0.4%) and Construction (-0.2%).

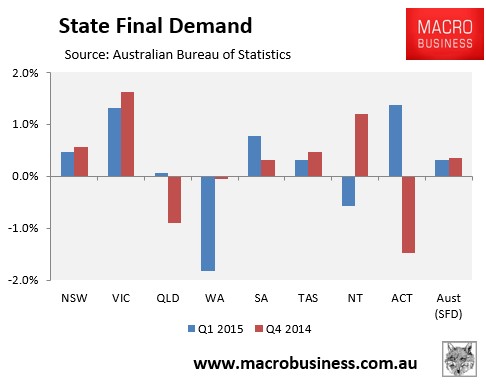

Results were mixed at the state and territory levels, with final demand weak in the mining jurisdictions (WA -1.8%; QLD +0.1%; NT -0.6%) but stronger elsewhere (VIC +1.3%; NSW +0.5%; SA +0.8%; TAS +0.3%; and ACT +1.4%). Final demand nationally also rose by only 0.3% over the quarter and was up just 0.8% over the year. [Note: state final demand does not include exports, so is markedly different to GDP]:

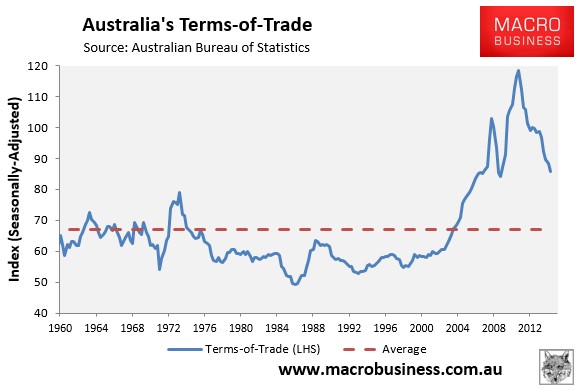

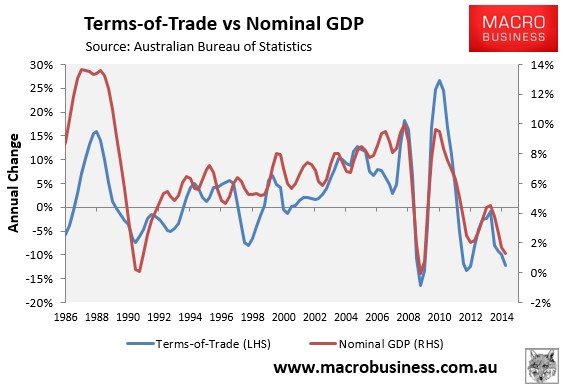

The terms-of-trade fell by a seasonally-adjusted 2.9% over the quarter and by 11.4% over the year, and now sits just above the GFC low, with much further still to fall:

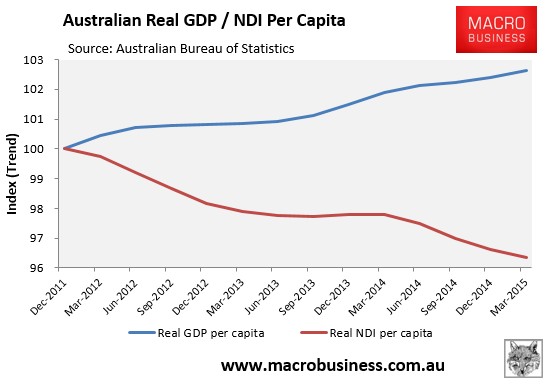

And as expected, the falling terms-of-trade dragged-down income growth, with real per capital national disposable income (NDI) up only 0.2% over the quarter but down 0.2% over the year.

However, because of population growth, per capita NDI fell a further 0.1% over the quarter and was down 1.6% over the year, and will continue to be weak as long as the terms-of-trade unwinds from its current still high level (see next chart).

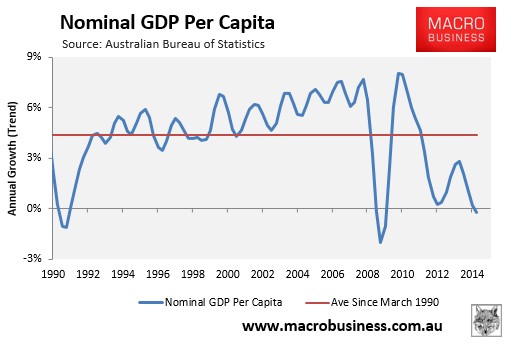

Indeed, the ongoing slump in per capita income – down 3.6% since December 2011 – is the real story of this release, not meaningless rises in GDP, which does nothing for living standards.

The fall in the terms-of-trade and national disposable income have also helped drag-down nominal GDP, which rose by only 0.4% over the quarter and by 1.2% over the year, which is generally a negative indicator for government finances:

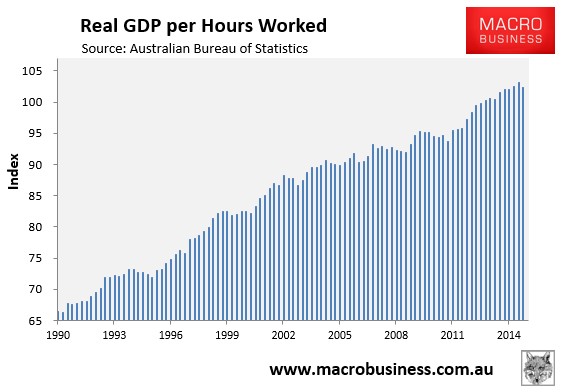

Another negative from this release is that real GDP per hour worked fell by 0.8% over the March quarter and was up just 0.2% over the year, suggesting labour productivity growth has stalled:

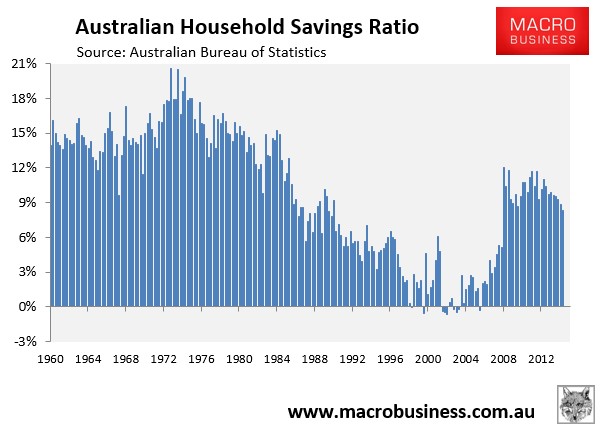

Finally, the household savings ratio continues to trend lower, falling to 8.3% from 8.8% in December 2014 and 9.6% at the same time last year, suggesting households are increasing their leverage:

Overall, this is another disappointing but unsurprising release, despite the better than expected jump in headline GDP.

National income per capita continues to slide backwards, labour productivity is low, and Australians are leveraging up once again into housing.

Sure, export volumes are good, but who cares when the price received for those goods is falling even faster?

The outlook is also poor, with ongoing falls in commodity prices (particularly iron ore) likely to continue dragging down per capita NDI over coming years – a trend that will persist as the terms-of-trade retraces back towards its long-run average.

The falling away in nominal growth is also a bad sign for Budget revenues, which are already set to take a hammering as capex falls faster than forecast.

The upcoming expected sharp falls in capital expenditures will, of course, also provide headwinds to GDP over coming years, and ultimately keep growth at an insufficient level to prevent unemployment from rising, despite rising net exports as increasing mining capacity comes online.

unconventionaleconomist@hotmail.com