More Liberal Party bubble supporters are on the hustings today:

Federal Liberal MP Craig Laundy has backed Treasurer Joe Hockey, saying he believes Sydney’s housing market is pricey but affordable.

Mr Hockey’s political opponents have labelled him “out of touch” after he dismissed suggestions that Sydney property was unaffordable and advised those looking to buy their first home to “get a good job”.

“The starting point for a first home buyer is to get a good job that pays good money,” he said.

“Then you can go to the bank and you can borrow money.”

Mr Laundy, whose electorate covers part of western Sydney, has defended Mr Hockey’s comments, saying it is technically a good time for people to buy.

“When you look at what he said in its entirety, he was saying when you have a job that is secure and that job is well paid, a bank will lend you money and interest rates are as low historically as they have been,” he said.

It’s not surprising. The bubble has been preened by both political parties at times, but it was the Howard Government that made the structural changes that birthed it. Yesterday, Fairfax’s Peter Martin expertly mapped-out how the Howard Government’s halving of the rate of capital gains tax (CGT) in 1999 ignited the investor orgy that is now helping to price young Australians out of home ownership:

It used to be said that house prices couldn’t climb to the level where owner-occupiers couldn’t afford to buy them. But it’s no longer true. John Howard severed the link in September 1999. A simple change to the Tax Act created a whole new class of buyers for whom occupying the house wasn’t the point. They could make big money by using houses as investments, getting someone else to live in them, and selling them later at a profit. From September 1999 only half of any profit they made was subject to tax.

This meant they could afford to pay more than the properties were worth, more than people could comfortably pay to live in them. If their interest payments exceeded their income from rent and they had to record a loss, so much the better. They could use the loss to write down other income and cut their tax. They would make it up later when they sold for a (largely untaxed) profit.

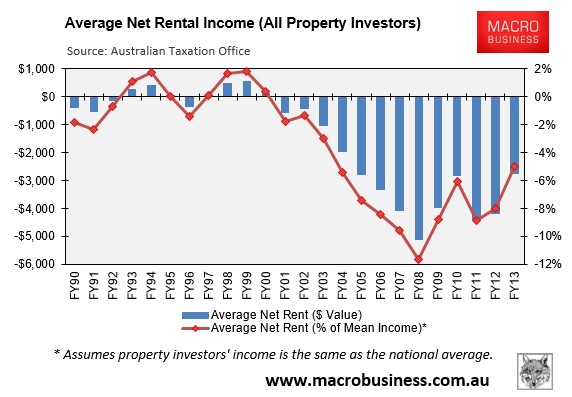

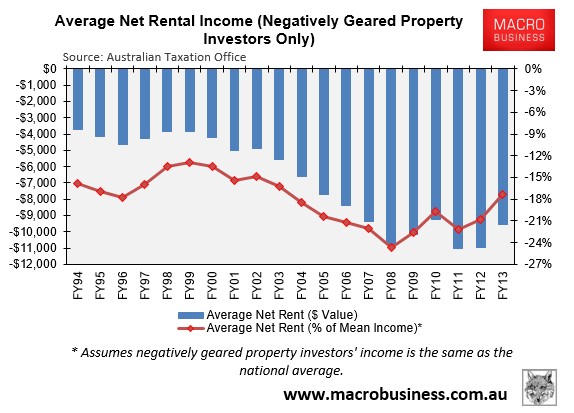

Before the change negative gearing wasn’t that common. In 1999 only 650,000 landlords recorded losses. Within five years the number had passed 1 million. It’s now 1.3 million, accounting for 1 in every 10 taxpayers. And their losses are no longer small. The average loss has jumped from $4000 to almost $10,000.

The flood of negative gearers has pushed prices to levels that once wouldn’t have lacked support. In the decade before 1999 Melbourne prices rose by an average of 4.8 per cent per year. In the 15 years after they’ve climbed 7.6 per cent per year. They’ll keep climbing for as long as negative gearers (who don’t much care about prices) outbid owner-occupiers.

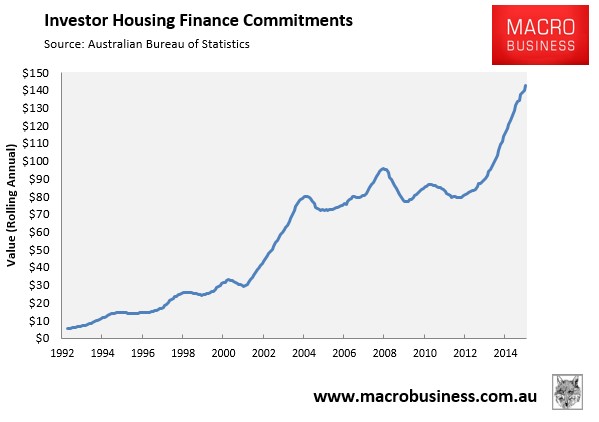

It is worth pointing-out to readers that shortly after CGT was halved, loans to investors surged, growing almost exponentially over the following four years (see next chart).

As pointed out by Martin, this growth was driven by a massive increase in the number of negatively geared investors, whose numbers have roughly doubled since 1999 at the same time as the number of positively geared investors has remained roughly stable (see next chart).

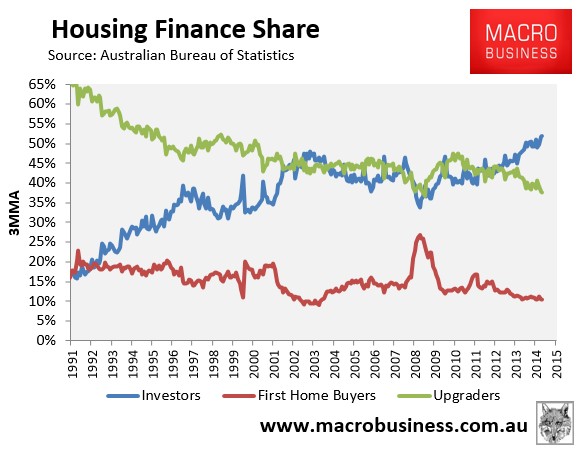

While the early 2000s explosion of property investment was indeed massive, it is nothing compared to the current episode. Yesterday’s housing finance data for April revealed that the share of mortgages (excluding refinancings) going to investors hit an all-time high 52.0% in April (see next chart).

While it is true that loans to investors has been growing ever since negative gearing was re-introduced in 1987 by the Hawke Government, the slashing of CGT made negative gearing a much more effective tax shelter – for reasons explained in the Hawke Government’s 1987 Cabinet Submission to re-instate negative gearing (viewable via searching here):

The negative gearing measure was introduced [in 1985] to partially close-off a generally recognised tax shelter, a rationale which remains broadly valid…

The three basic features of a typical tax shelter are the absence of a full nominal capital gains tax, the deductibility of full nominal interest expenses, and the mis-match in the timing of the deductions and the recognition of taxable income (for example, because capital tax is payable on a realisations rather than accrual basis).

Rental property investment clearly exhibits each of these features, as do some other activities, and so effectively obtains tax benefits under the current tax system.

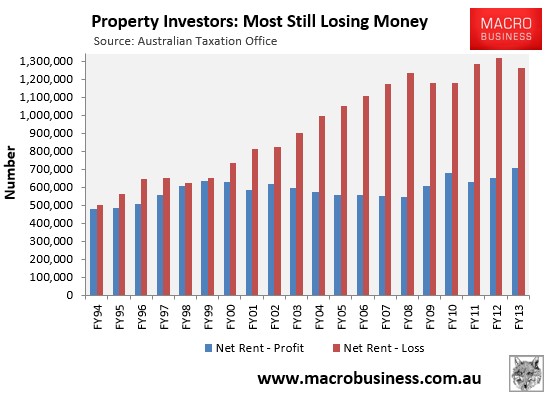

Howard’s CGT discount made the existing tax shelter under negative gearing even more pronounced. It is also a key reason why the value of rental losses exploded after the CGT discount’s introduction (see below charts).

Of course, there are other things the Howard Government did to expand the property bubble, including allowing self-managed superannuation funds to leverage into property, ramping-up immigration, and implementing a raft of first home buyer subsidies. There are obviously also other contributing factors, including financial deregulation, falling interest rates, foreign investors, and the states’ increasingly restrictive land-use policies.

Nevertheless, it is the Howard Government’s halving of CGT that first put a rocket under negatively geared investment which continues to plague the housing market today, to the detriment of first home buyers.