From the Motley Fool:

Strategy

Rio Tinto’s strategy of increasing production at a time when prices are depressed is a sound move. Certainly, it has been argued that it has added a downward pressure on the price of iron ore and, while this may be true, Rio Tinto has correctly sought to strengthen its own position through increasing supply.

Not only has this allowed it to post profits that otherwise would have been lower, it has strengthened the company’s position versus a number of its peers who do not enjoy a cost base that is as low as that of Rio Tinto. As such, Rio Tinto appears to be ready to emerge from the current period of depressed iron ore prices in a much stronger position relative to its rivals.

Sustainability

As touched upon above, Rio Tinto has an exceptionally low cost base, which provides it with relatively healthy margins and means that it is among the most sustainable mining companies on the ASX. This low cost curve has been achieved through generating considerable efficiencies in recent years, as well as leveraging the company’s size and scale.

And, with Rio Tinto having a strong balance sheet (with a debt to equity ratio of just 46%) and excellent cash flow so as to be able to sufficiently invest in the long term capability of the business (net operating cash flow has averaged US$13bn per annum during the last three years), its future appears to be secure.

Value

Although Rio Tinto continues to trade at a premium to its net asset value, a price to book (P/B) ratio of 1.75 indicates good value for money. Certainly, it may be higher than the mining sector average of 0.65, but Rio Tinto offers a degree of stability and sustainability that few of its peers can match.

Furthermore, with the global economy continuing to move from strength to strength, it would be of little surprise for demand for iron ore to increase over the medium term. And, with Rio Tinto’s bottom line set to return to growth as early as next financial year, its valuation has scope to expand over the medium term.

MF has been all over the place on iron ore with regular buy and sell arguments and no clarity but this is the worst yet.

The three reasons to buy are ridiculous:

- RIO does not have a strategy of increasing supply when prices are depressed. Rather, it massively over-estimated Chinese demand growth and is now trapped between sunk costs and competitors that have made the same fateful mistake. To the extent that this is a plan at all it is a desperate rear guard action.

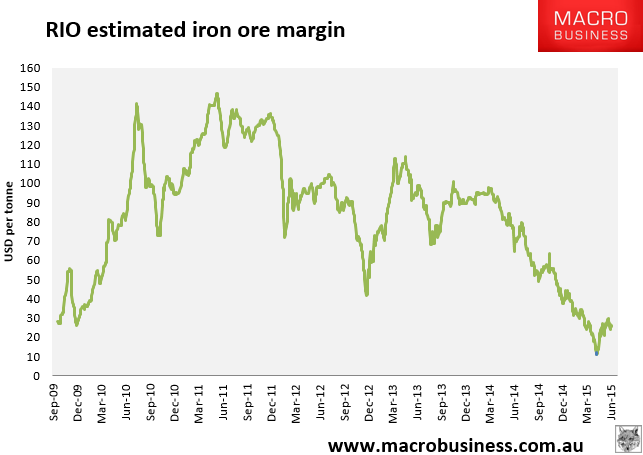

- Who cares how low RIO’s cost base is if the cost of its major product is collapsing. RIO’s margins are in a dreadful swan dive and my guess is they will turn negative before the shakeout ends:

- finally, how do you find value in a stock that is trading miles above the sectoral book value average and has giant exposure to the largest and longest commodity glut that the world faces?

The risks for any re-rating for RIO are tilted very much to the downside as the super cycle falls through its super bust.