Stephen Koukoulas (“the Kouk”) has posted an extract from his book that fails to debunk the “emotive codswallop being written and spoken about housing affordability”.

Let’s take a look.

Think of housing affordability in this way.

In the mid to late 1980s, a house cost, say, $75 000 and required a mortgage of $60 000 — that is, a loan-to-valuation ratio of 80 per cent. Household incomes at this time were around $25000 per annum and interest rates were around 13.5 per cent. In these circumstances, it took around 20 to 25 per cent of a household’s after-tax income to make the monthly mortgage repayment. The other 75 per cent of disposable income could be spent as the householder wanted.

Fast forward to now. A house is around $625 000 and, based on a loan-to-valuation ratio of 80 per cent, the mortgage would be around $500000. Household disposable income is around $125000 per annum and the interest rate is 5.25 per cent (although the increased competition now compared with the 1980s means that not many people pay this advertised rate). In these circumstances, it takes around 20 to 25 per cent of a household’s after-tax income to make the monthly repayments.

While house prices are up, so too are household incomes and, critically, interest rates are structurally down.

This shows, quite starkly, that it is no tougher financially for a first- home buyer today to service an average mortgage on an average house than it was 20 or 30 years ago. It is just that in the so-called good old days, the average home buyer’s mortgage pain came through interest rates and not the house price. Now, the pain comes through the house price and not interest rates and, I suspect, expectations being skewed to buying above-average houses.

Looking at it another way, monthly repayments are much the same on a $400 000 mortgage with an interest rate at 5.25 per cent as they are on a $300 000 mortgage with an interest rate of 8 per cent.

As a homeowner with a mortgage, what would you prefer? The joy of buying a house at a low price, with a relatively low mortgage, but having to pay a high interest rate, or taking out a large mortgage on an expensive house but having a low interest rate to service that loan?

Any prospective home buyer should be largely indifferent to these dynamics. Those wanting lower house prices, beware! It might come at the cost of higher interest rates, which would do little or nothing to help affordability.

Think of it this way. House prices could undoubtedly fall to make them more affordable, and a return to 8 per cent interest rates would no doubt help achieve that. Imagine paying a 13.5 per cent mortgage interest rate (as paid in the 1980s) right now. Obviously, if that were ever to occur again, a first-home buyer’s delight in getting a cheaper house and therefore borrowing less would, by definition, be neutralised by the pain of higher interest rates.

For those bemoaning high house prices now by stressing the lack of affordability, go to one of those very good mortgage calculators that are so common on the internet. Plug 10 per cent, 13.5 per cent or even the 1990s peak of 17 per cent into the ‘interest rate’ box and see how much you could afford to borrow today. The exercise should change those perceptions of poor housing affordability in recent years.

I am not sorry for going on about this — it is a vital point to make. It is a roundabout way of saying that it has never been easy to get into the housing market for the first time or to upgrade to a nicer house, but it is no harder now than it was in the past. It is just that the dynamics and the mix are different.

What has not changed is that sacrifices need to be made to get your foot in the door of the property market.

Make no mistake, this is one of the worst analysis of housing affordability that I have read.

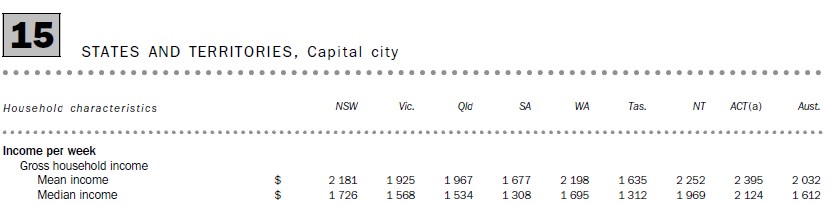

First, the Kouk has failed to account for the size of the deposit that must be saved. In the mid-to-late 1980s, the hypothetical home buyer had to save a deposit of $15,000 on an income of $25,000. That’s only 0.6 times gross income.

Today, using Kouk’s example, a home buyer would have to save a deposit of $125,000. Gross median household incomes are nowhere near the $125,000 claimed by the Kouk, but rather $90,000 across Australia’s capital cities (estimated using the below ABS data on median household income as at June 2012, adjusted up by wages growth). This means that today’s typical home buyer needs a deposit of 1.4 times gross household incomes. Add stamp duty into the mix, which is much higher today than it was in the 1980s, and the equation worsens.

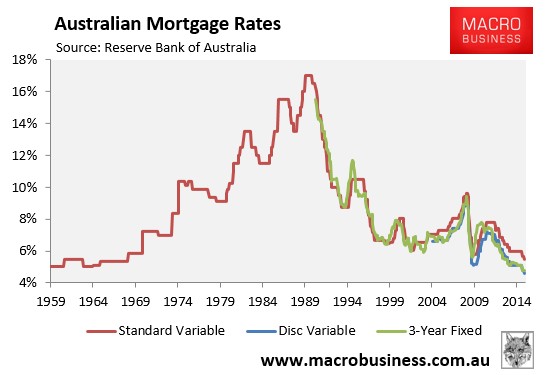

Second, the Kouk has conveniently drawn his conclusions by comparing repayments on mortgages taken-out today against repayments during the period when mortgage rates were amongst the highest in Australia’s history (see next chart).

This is misleading on a number of levels.

First, interest rates in the late 1980s did not stay high for long and a home buyer back then got to enjoy the benefit of a massive drop in mortgage rates over subsequent years and a corresponding massive rise in house prices.

Does anyone honestly believe that today’s first home buyer is likely to face similar conditions in the years ahead, whereby mortgage rates more than halve and values skyrocket?

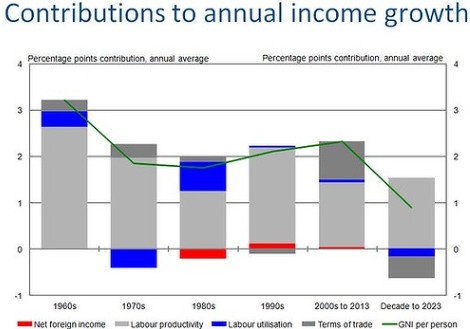

Second, as noted by the Australian Treasury last year, average income growth is expected to be the weakest in at least 60 years over the coming decade, which is going to make paying-off today’s mega mortgage far more difficult (see next chart).

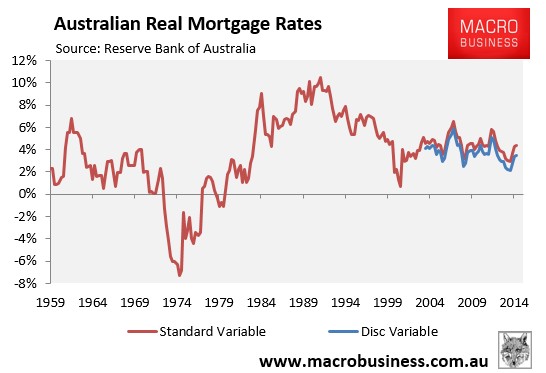

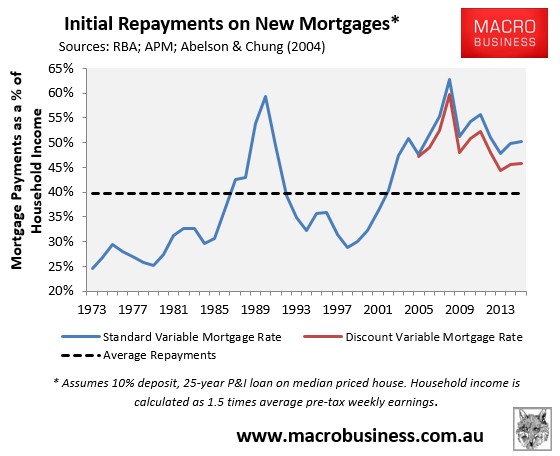

Third, when adjusted for inflation, real mortgage rates – 3.5% (discounted) as at March 2015 – are above levels that existed prior to the early-1980s – a time when many baby boomers purchased their homes (see next chart).

Fourth, while initial repayments on new mortgages are lower than the late-1980s and early-1990s, they remain well above the 40-year average (see next chart). Therefore, current housing conditions remain unfavourable, particularly given the coming shock to incomes.

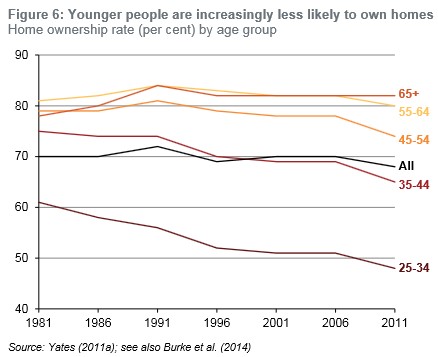

Finally, the Kouk fails to mention the sharp drop-off in home ownership rates amongst younger cohorts – bonafide evidence of falling housing affordability (see next chart).

What should also become clear from the above charts is that the 1970s was a dream time to purchase a home. Not only were homes highly affordable at roughly three times incomes, but a purchaser was in the fortunate position to have had their debts inflated away via high inflation and centrally indexed wage rises that outpaced the cost of credit.

Of course, it was also the early baby boomers who benefited the most from these favourable conditions before enjoying the rampant house price inflation that followed. If only today’s home buyers were so lucky!

unconventionaleconomist@hotmail.com