So, it looks like Joe Hockey’s pledge on Monday night’s Q&A Program to dump the GST on women’s sanitary products, like tampons, has the support of the states, which means there’s a good chance that it will be implemented.

Viewed in isolation, the idea makes sense. Given that condoms have no GST applied on their sales, then why should women be penalised for purchasing what is an unavoidable and necessary expense?

However, my broader concern is that the whole argument about applying GST to tampons misses the point. Rather than removing GST on products on a case-by-case basis, Government’s should instead be looking to remove all exemptions from the GST, thereby broadening its base, and using the extra funds to undertake broad-based tax reform that improves both efficiency and equity.

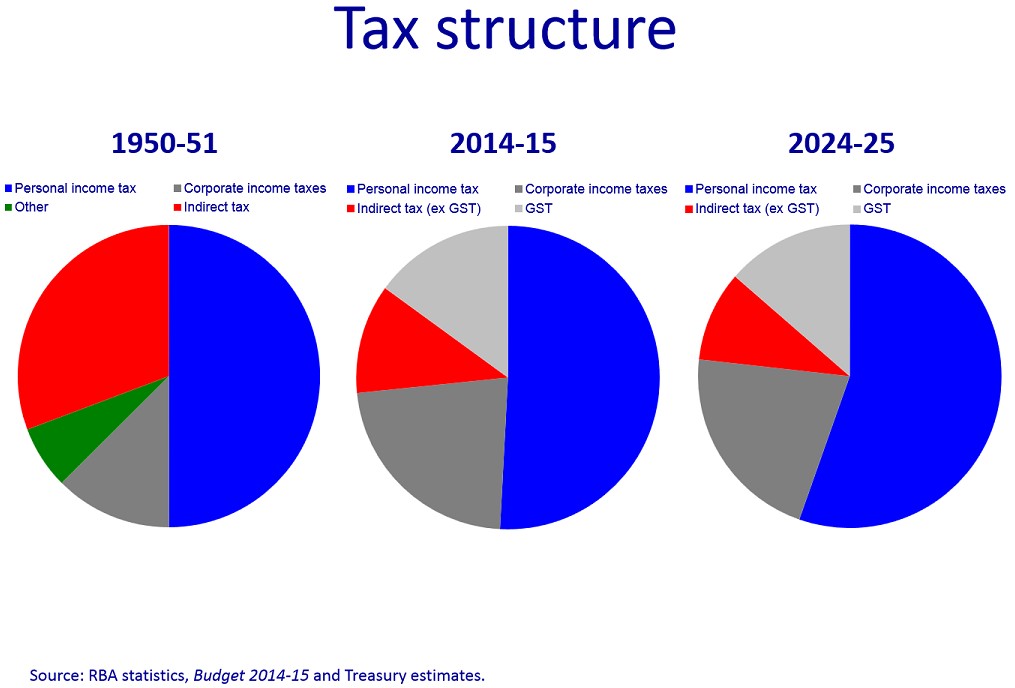

It is a fact that Australia’s existing tax structure is becoming increasingly narrow and unsustainable, and that personal income taxes will rise dramatically via bracket creep as the once-in-a-century commodity price and mining investment booms unwind and national income growth slows.

Advertisement

Former Treasury Secretary, Martin Parkinson, showed us last year that if left unchanged, personal income taxes will rise inexorably over the coming decade, making the tax system less efficient:

…under current policy settings our reliance on income taxes – both personal and corporate – will continue to increase.

As a result, without conscious change, the economic cost of raising tax from our current tax mix will also increase. Many studies, both in Australia and internationally, have suggested that reducing reliance on direct taxes would lead to higher incomes…

By contrast, indirect taxes – which are derived mostly from the GST – will shrink, as tax receipts grow by less than inflation due to the various exclusions on health products, education, and basic food (amongst other areas).

Advertisement

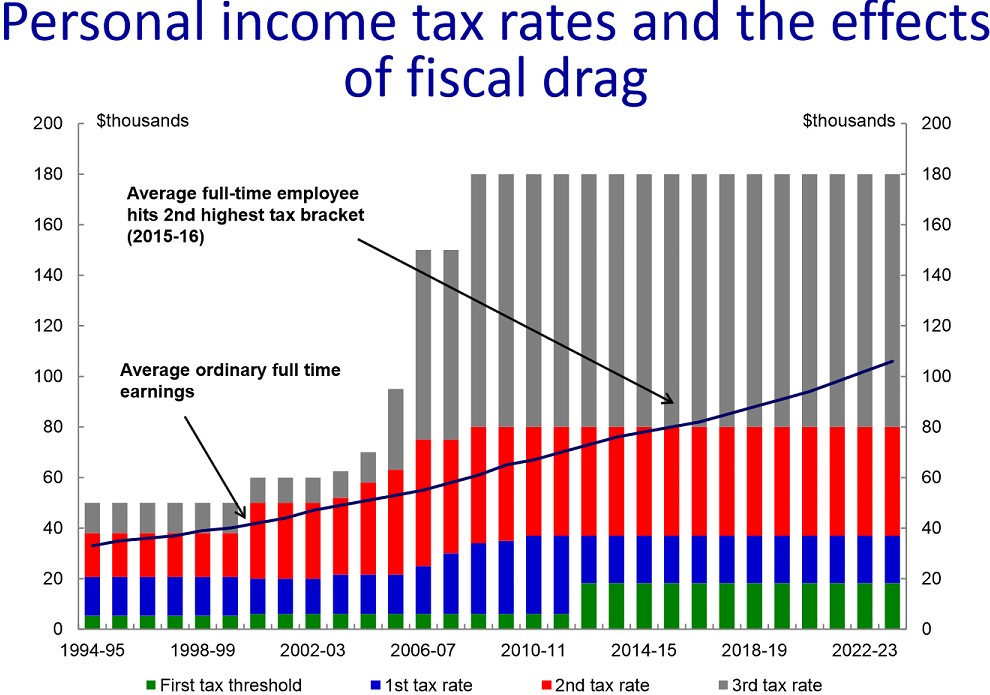

More worryingly, this inexorable rise in personal income taxes though bracket creep (aka “fiscal drag”) will punish lower paid workers the most, since it is they who will experience the biggest rises in average tax rates. Dr Parkinson explains:

…there are significant costs associated with inaction here since our personal tax thresholds are not indexed.

I have mentioned before that fiscal drag is expected to pull someone on average full time earnings into the third tax bracket, with a marginal rate of 37 per cent (or 39 per cent including the Medicare levy), from 2015-16.

And over the decade ahead, the average tax rate paid by that individual is expected to rise from 23 per cent to 28 per cent, an increase of over 20 per cent. Moreover, the increase in the average tax rate for lower income earners is generally greater than for higher income earners. One consequence of this is to make the personal income tax system less progressive…

A higher tax burden reduces the immediate reward for effort. At low levels of income, it can be a barrier to participation.

At higher levels of income, a rising personal tax burden increases the benefits from tax planning and tax minimisation. This is magnified even further if combined with a falling corporate tax rate…

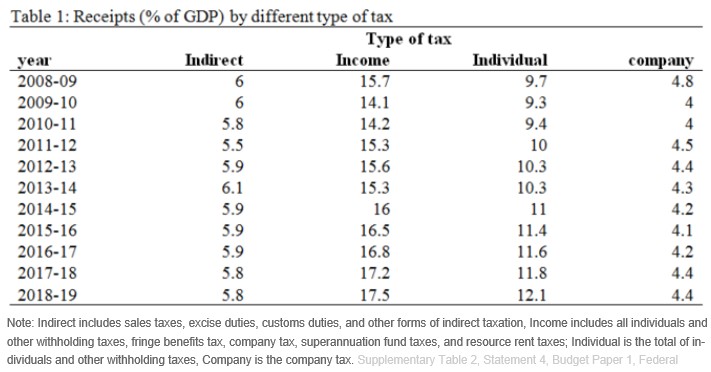

This month’s Budget confirmed these findings, and showed that the share of taxes derived from incomes is projected to rise from 16% of GDP in 2014-15 to 17.5% of GDP by 2018-19, an increase in the tax burden on workers of 9.4% (see next chart).

Advertisement

Another reason why the GST should be broadened is that it is far more efficient than personal income taxes, producing a “marginal excess burden” of just 8% versus 24% for personal income taxes, according to the Henry Tax Review:

Advertisement

With the population ageing, and the share of workers set to decline, broadening the GST would also share the tax burden with the growing share of people no longer in the workforce, so in this sense could help mitigate ageing’s effect on the Budget.

Ultimately, fundamental tax reform is required to ensure that the tax base is broadened and built around more efficient and equitable sources. Broadening the GST would help in this regard, as would raising a greater share of revenue via land taxes and resources rents.

Of course, the Government should also look to close Australia’s world-beating tax concessions (e.g.superannuation, negative gearing and capital gains discounts), which cost the Budget many billions of dollars in foregone revenue and are skewed towards the wealthy and high income earners.

Advertisement

This is where the whole tax reform debate should be centered, not on excluding individual product lines from the GST.

With Australia’s population ageing fast, and the proportion of workers to non-workers set to decline significantly in the decades ahead, the Government will ultimately be forced to scale back tax concessions as the tax base shrinks, and/or look for new, more efficient, ways to raise taxes.

There are many options, and it is better to start the reform process now rather than rejecting reform altogether, as the Abbott Government has done, and waiting until there is a Budget crisis.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.