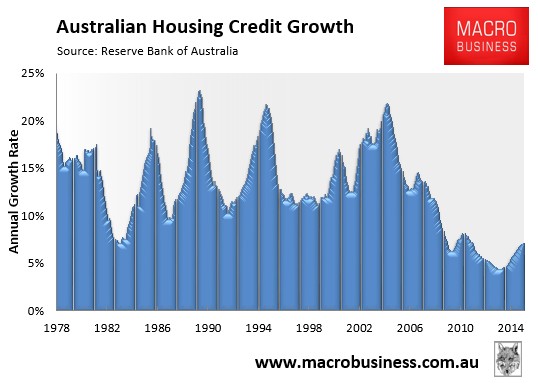

Yesterday’s private sector credit aggregates data, released by the RBA, revealed a strengthening of mortgage growth to 7.3% in the year to March 2015 (see next chart).

Often when reading commentary from the RBA on the Australian housing market, we hear that mortgage credit growth is well below the early-2000s experience, therefore, risks are contained. Certainly, a superficial glance at the above chart confirms this view.

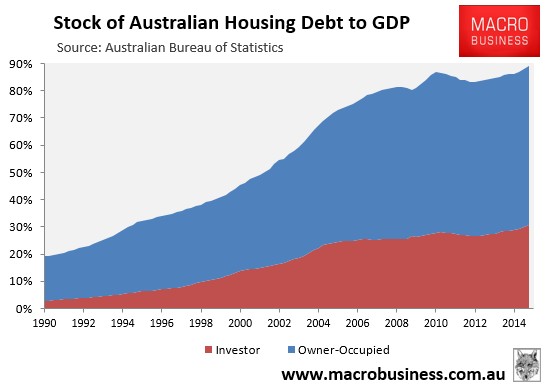

However, the primary reason why the percentage growth in Australian mortgage debt is relatively low is not because the stock of outstanding loans is growing slowly, but because the outstanding stock of mortgages is ginormous, as confirmed by the record ratio of mortgage debt to GDP (see next chart).

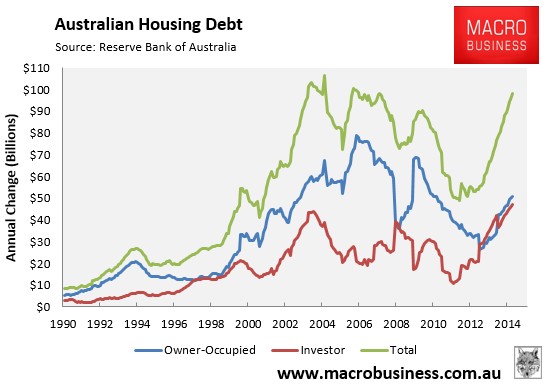

Indeed, when one looks at the annual change in the value of mortgage debt, we see that mortgage growth is in fact quickly approaching its pre-GFC peak, driven by record investor mortgage growth (see next chart).

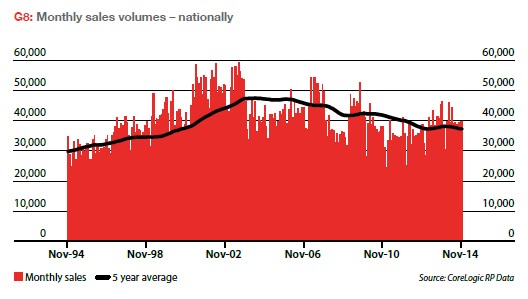

One of the reasons why mortgage growth has not already exceeded the pre-GFC experience is because the volume of housing transactions has fallen over the past decade (see next chart).

In effect, fewer sales have taken place but at much higher prices.

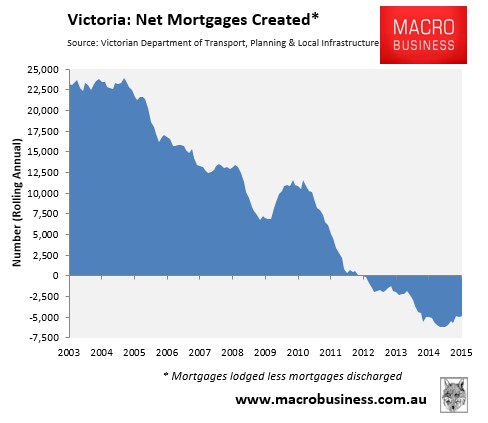

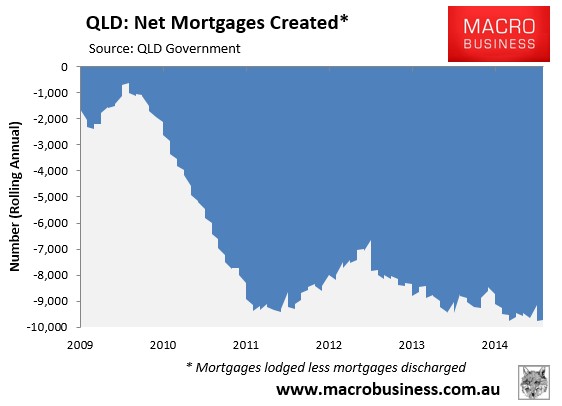

Another reason is because those with older existing mortgages have taken advantage of lower interest rates and been paying-off their loans faster, which has helped offset the new mortgage generation. For example, we have seen this phenomenon both in Victoria and Queensland, where the state based data has shown that the number of mortgages outstanding has been shrinking (see below charts).

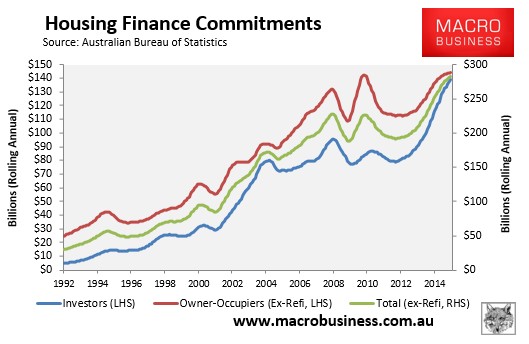

It is also worth noting that the value of new housing finance commitments is easily at an all-time high, driven again by unprecedented investor participation (see next chart).

So, far from mortgage growth being under control and well below early-2000 levels, there is an unsustainable investor bubble that severely risks destabilising Australia’s financial system and economy.