As the iron ore rally persists in conjunction with Twiggy Forrest’s outrageous bluster, the feeble-minded might be duped into believing that the iron ore market balance is improving when, in fact, it is getting worse.

I recent days we have seen BHP and Vale cut expansion forecasts by 50 million tonnes. These cuts are distant but have had the effect of squeezing a steel mill restock as Chinese stimulus gets progressively more intense.

However, in the recent past we have also seen several other developments. The first is that the African Tonkolili mine is to be reopened and expanded by Chinese interests. That will add 25mt long before BHP or Vale get to their cuts. We’ve also seen India cut its ad valorum taxes on iron ore, allowing Goan exports resume post monsoon, adding another 15mt this year. Atlas iron will sustaining production at 10mt at a breakeven below $50 per tonne. Today there re rumours that Roy Hill will be pushing back its launch by two quarters though the company denies it and even so that is not a material shift.

So, supply expansions and curtailments have basically cancelled one another out.

Advertisement

But that is not the big news. That dubious privilege belongs to the IMF’s new Chinese property forecasts which paint an extraordinarily bearish demand outlook over the next three years.

MB iron ore price modelling has used a fall of 2.5% per annum in Chinese steel output over the next three years. That makes MB the most bearish in the market and cancels out falls in Chinese iron ore production and then some, meaning that all of the current and future oversupply in the iron ore market will have to come through shut-ins in the seaborne market.

But, if the IMF is right, then MB has been far too conservative. Here’s the money chart from yesterday:

Advertisement

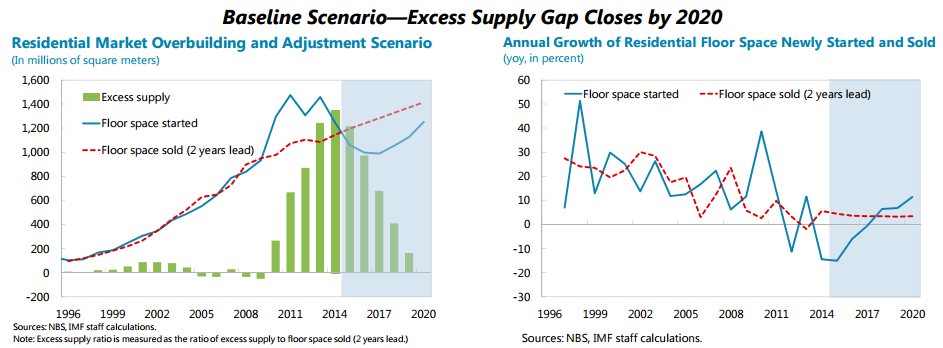

Baseline scenario. This scenario assumes that the excess supply gap will close gradually by 2020, broadly in a linear fashion. Excess supply will be absorbed through both a moderate contraction in floor space starts and a recovery of projected real estate demand in the medium term. The adjustment scenario yields the path of the year-over-year growth rate of floor space starts and floor space sold, providing an indication of real estate investment in the medium term, as considered below. We can also trace the effects on the inventory ratio of closing the excess supply gap considered in section II (based on FangGuanJu data): it would fall from 2.2 in 2013 to about 1 (a normal historical level) by 2020.

Let’s face it, the IMF is not renowned for its bearish calls so we ought to take this seriously. In it, Chinese residential floor starts must fall by one third from 2014 to 2017 to clear the market of oversupply. Real estate represents half of Chinese steel consumption so this is a 15% peak to 2017 trough fall over the next three years. All things equal that is a reduction of 124 million tonnes (mt) of steel from 2014 levels. Converting that to iron ore gives you a demand hit of 200mt versus 2014 levels.

In effect, MB has been modeling half of that amount.

Advertisement

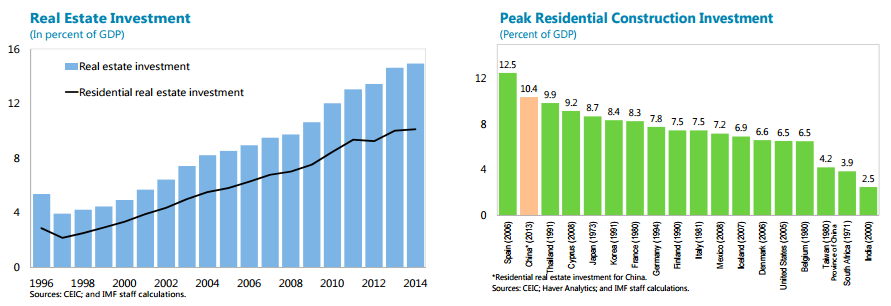

However, a second IMF chart shows that this magnitude of fall is not likely to actually transpire:

Real estate investment is a huge proportion of GDP so you can expect a big move towards expanded infrastructure development to partially offset the downdraft. With some added exports and to be conservative, let’s cut the fall in China’s steel production implied by the IMF numbers in half.

Advertisement

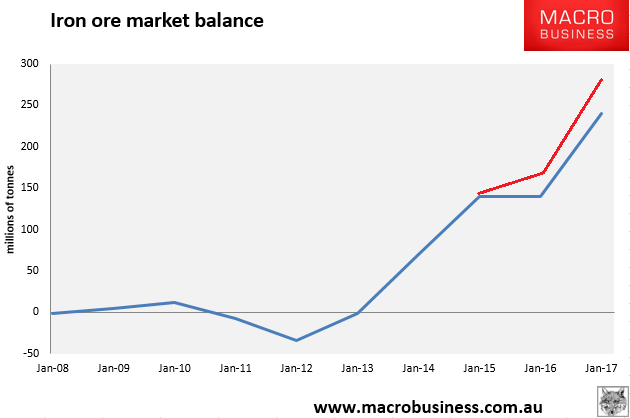

That still cuts another 50mt of Chinese iron ore demand out of the market versus MB’s old modeling. So, adding all of that together we get this:

Blue is the old surplus forecast and red is the new one. Yes, that’s right, despite all of the panic, hyperbole and hope the modeled looming glut has gotten worse not better.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.