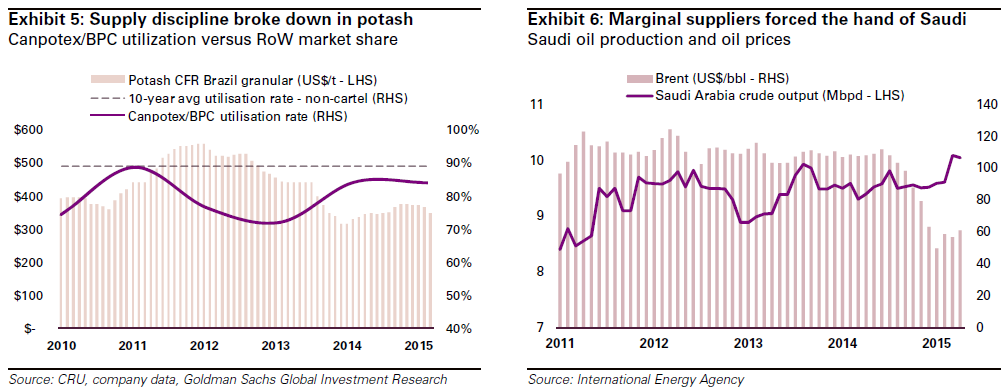

Voluntary production cuts are appealing in theory…

The role that low cost expansions in Australia and Brazil are playing in driving iron ore prices lower has come into focus among investors, corporates and even policy-makers. With government receipts under pressure and the commercial viability of smaller producers at risk, many voices have asked for a change of strategy at the 3 largest producers that in aggregate account for 2/3 of current seaborne supply. According to this alternative view, dominant producers should maximize profits for the broader industry by refraining from further expansions. In principle, a steep cost curve where marginal producers are allowed to set the iron ore price without the risk of displacement by more competitive supply could result in a better outcome for all miners.

… but Tier 1 miners will not stand in the way of falling prices

However, we believe this view is misguided. First, production cuts would go against the prevailing trend of improving efficiency – our analysis indicates that mining productivity in the Australian iron ore industry is increasing by 4% p.a., resulting in higher output and lower unit costs. Second, the required coordination among dominant producers with different incentives would be more difficult to achieve among three companies; successful cartels in oil and potash have featured only one or two dominant producers. Third, seaborne demand is likely to peak in 2016 and the iron ore market is becoming a zero-sum game. Tier 2 producers have up to 100Mtpa of new capacity to commission in the next couple of years, so dominant producers would have to stomach further production cuts in order to support prices over the medium term.

In summary, efforts to support prices via voluntary production cuts would be counter-productive. In our view, competition in the iron ore market can only intensify; we expect the war of attrition will continue while prices gradually decline towards our US$40/t CFR China forecast by 2017. We believe the alternative scenario, where dominant iron ore producers collude to secure abnormal profits, is as implausible as a chimera, the firebreathing mythological creature that was part lion, part goat and part snake.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.