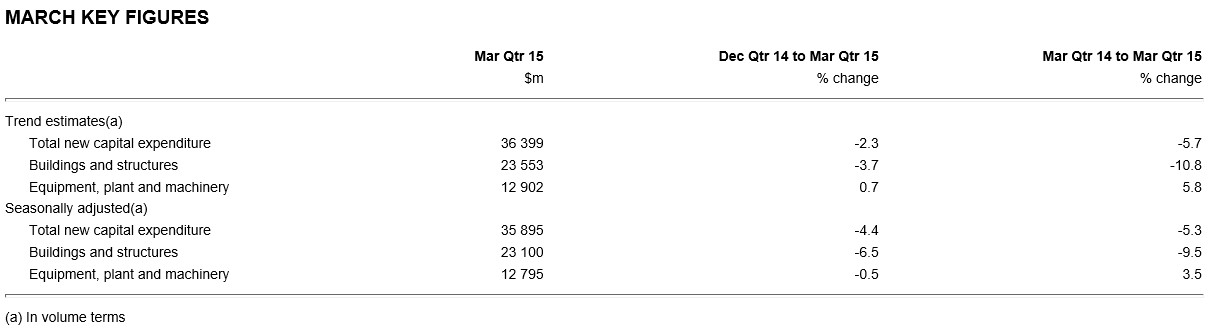

The Australian Bureau of Statistics (ABS) today released data on capital expenditures (capex) for the March quarter of 2014, which registered a 4.4% seasonally adjusted fall in capex over the quarter and a 5.3% decrease over the year. The result badly disappointment analyst’s expectations of a 2.2% fall over the quarter (see below table).

While Houses and Holes has covered the forward-looking capex plans over the coming years, below are some backward looking charts showing actual capex up to the March quarter of 2015.

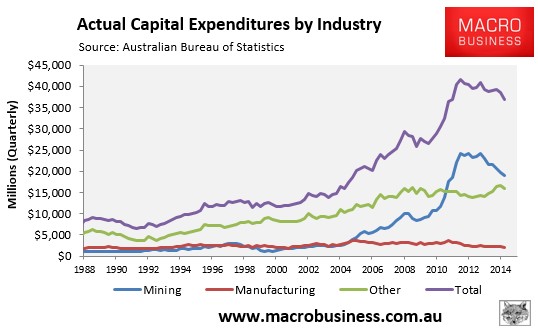

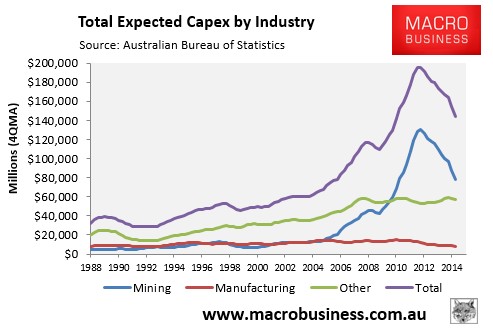

The first chart below shows actual capex by industry in dollar terms (rather than volume terms as shown above). As you can see, the fall in total capex (-4.0%) was broad-based, with mining capex (-4.1%), manufacturing capex (-8.5%) and “other” capex (-3.4%) all registering significant falls:

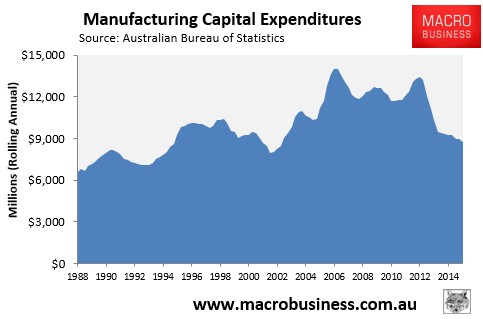

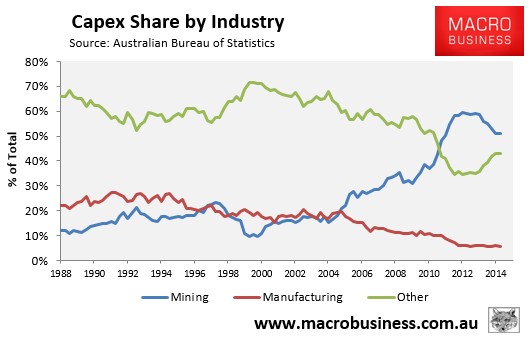

Manufacturing capex remains well and truly in the doldrums, with its share of total capex at just 5.7% in the March 2015 quarter (see below charts).

As you can see, annual manufacturing capex – $8,761 million in the year to March – was the lowest since June 2002 in nominal terms. In real inflation-adjusted terms, the result would obviously be much worse.

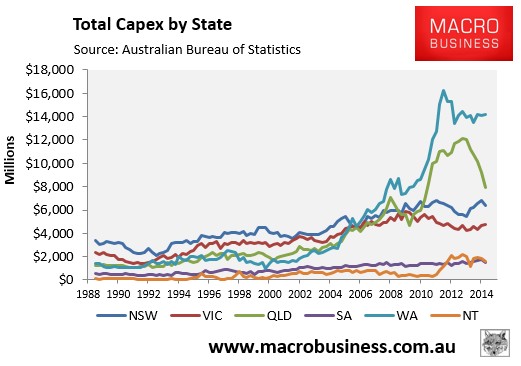

The fall in capex nationally was drive by Queensland, where capex fell by $1,310 million (-14.2%) over the quarter, most likely due to the ramping down of construction on the three Gladstone LNG plants. By contrast, capex rose slightly in Western Australia – most likely held up by Gina’s Roy Hill iron ore mine – rising by $146 million (+1.0%) in the March quarter (see below chart).

Looking ahead, the capex pipeline continues to shrink, due to falling planned mining investment (see next chart).

The longer-term outlook remains very poor. Mining capex faces a prolonged period of sharp falls that will accelerate through to 2017, and manufacturing capex remains terminally sick. Meanwhile, “other” (services) capex is ill-equipped to fill the void.