Commodity prices may have hit bottom – but don’t expect a sharp recovery.

So says Mihir Worah, chief investment officer for real return and asset allocation at global bond fund manager PIMCO, who says a supply shake-out forced by sharp price declines over the last year has put supply and demand closer to equilibrium.

“The commodities super cycle is done,” he said.

“The correction is over.”

The AFR has a piece today on Aquila’s Tony Poli:

Tony Poli must be the luckiest man in iron ore. He may not have felt like it 10 months ago, but he surely does now.

Poli netted about $400 million of the $1.34 billion Baosteel and Aurizon paid for the Perth-based iron ore and coal junior he co-founded – Aquila Resources – just as the iron ore price began to fall off the edge of a cliff.

But insiders close to the deal have said while it might have seemed a no-brainer for executive chairman Poli and the rest of the board to accept the bid, it was far from it. At the time, the widely held expectation was that iron ore prices were going to rebound, and that $US100 would be a floor.

Poli, who sold his 29 per cent stake in Aquila into the deal, recognises the fortuitous timing but has shied away from discussing the deal because of the difficulty many of his peers in the industry now find themselves in. He declined to comment for this article.

This deal was always a steal and good luck to Poli. I don’t know why the one junior who did escape with his shirt on needs to be put down. It’s a lesson that some young bloke at Dad’s Army could learn today as he calls an iron ore bottom:

The most obvious clue was analysts clamouring to deliver the grimmest forecast throughout April. It ‘may never reach $US50 a tonne again’, Goldman Sachs screamed, while Citi, Deutsche and even our Treasurer all spruiked a fall into the mid-$US30s as ratings agencies placed a watch on the sector.

There’s something about a mass warning of the ‘end of days’ that suggests the worst is either within sight or already behind us.

Advertisement

The entire piece runs without a any reference to the particulars of tonnages for steel or iron ore.

Back at the AFR, the commodities bust is over according to PIMCO:

Advertisement

“Supply has caught up with demand, and we don’t believe commodity prices will go down from here,” he said.

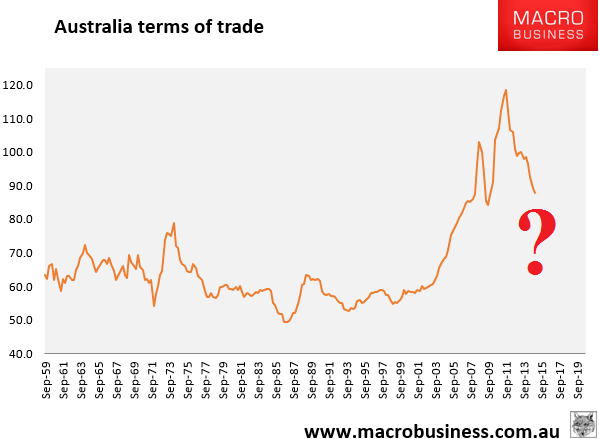

Crikey, is that right? Let’s check in on the super cycle and see if it’s over:

We’re about halfway. The reasons why are still available here.