The Secretary of the Australian Treasury, John Fraser, has given a scathing assessment of Australia’s retirement system, arguing that the interaction between superannuation, the Aged Pension, and housing tax breaks have created a labyrinth of middle-class welfare. From Fleur Anderson at The AFR:

“It’s difficult not to speak about so-called middle-class welfare and the questions around retirement incomes, and the array of concessions and incentives around the age pension, superannuation and housing”…

“I was there in the major reforms of the late ’80s and early ’90s, and a lot of the planning we did at the time hasn’t proved to be correct – a lot has proved correct – but there are unintended or not forecast outcomes”…the time has come 25 years or so after those big reforms to have a more fundamental rethink about the interaction between superannuation and tax and the whole welfare system.”

That’s about as damning an assessment as you are likely to get from a senior public official. What Mr Fraser is really saying is that the whole superannuation, Aged Pension and housing system is inequitable as it provides disproportionate benefits to high income earners and the wealthy, who should be able to look after themselves in retirement.

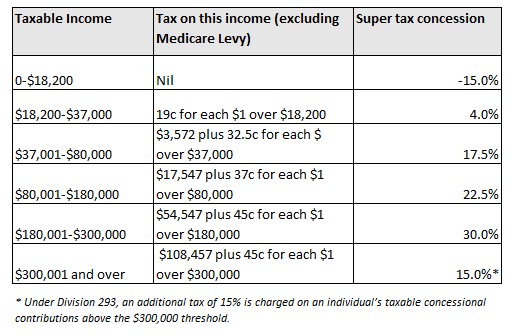

The problems are multi-faceted. First there is the ridiculous flat 15% tax on superannuation contributions, which provides the greatest benefits to higher income earners (see below table).

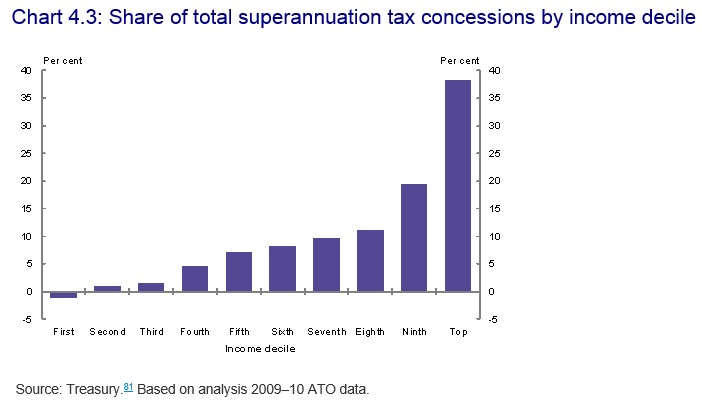

When combined with the tax-free status of superannuation earnings for those over the age of 60, we have the ridiculous situation whereby the overwhelming majority of superannuation concessions are flowing to wealthy (see next chart).

Obviously, by providing massive taxation concessions to those on the highest incomes, the Budget is losing many billions of dollars of forgone revenue each and every year. Meanwhile, super is failing to relieve pressure on the Aged Pension, since those that are most likely to need it – lower and middle income earners – receive minimal concessions (or get penalised), which both hinders their ability to build-up a retirement nest egg and discourages them from making additional contributions.

Then there is the ridiculously generous assets test around the Aged Pension, which not only excludes one’s principal place of residence, but also is so lax that a couple that owns their own home and has almost $1.2 million in financial assets still receives welfare, along with a lucrative Commonwealth seniors’ card.

The latest Inter-Generational report highlighted this craziness of the situation in all of its ugly glory:

A pensioner can continue to receive some payment and the Pensioner Concession Card with assets (excluding their primary residence) up to $771,750 for single homeowners and $1,145,500 combined for couple homeowners. A single person who does not own a home can have assets up to $918,250 and a couple up to $1,292,000 combined and still receive a part pension. A single pensioner can also earn up to $1,868.60 per fortnight (approximately $48,580 per annum) in income and continue to receive a part pension, while a couple can earn up to $2,860 per fortnight combined (approximately $74,360 per annum).

For example:

• Kathleen and Steve are 68, own their home and have $1.1 million in superannuation, shares and bank accounts. They have no other income. They will receive a part-rate pension.

• Liam is 75 is single and has superannuation, an investment property and shares valued at $910,000. He does not own a home and has no other income. He also receives a part-rate pension.

• Lillian is 85, single and lives in her own home worth $1.5 million. She has bank accounts valued at $50,000 but has no other income. Lillian receives a full-rate pension.

Again, it is hard to deny that the Aged Pension is very poorly targeted, providing far too much assistance to those with significant assets – both financial and non-financial (e.g. owner-occupied housing).

As I keep arguing, the Aged Pension is the biggest and fastest growing area of welfare expenditure, with superannuation concessions not far behind. Given the proportion of workers supporting retirees is projected to shrink, it is imperative that the means test for the Aged Pension is tightened to ensure that only those in genuine need receive it, whilst also ensuring superannuation concessions (particularly for the wealthy) are also reined in.

Otherwise, richer older Australians will continue to receive a free taxpayer ride, while poorer segments of society (and the young, in particular) are required to shoulder the burden of Budget cuts.