LF Economics, a new Australian analytical and research firm, has produced another interesting report examining the claim that housing supply shortages are the cause of Australia’s unaffordable housing:

Today, there are few, if any, examples in modern history to suggest that the cost per square metre of land in such a sparsely populated nation has ever reached so high. It is significantly cheaper to acquire land (per square metre) on the hills of Malibu, California, with a view of the Pacific Ocean, than it is to acquire land in the remote Australian desert town of Alice Springs. Malibu is an affluent suburb in Los Angeles and globally recognized, while Alice Springs is a small, dusty town surrounded by desert with little economic activity or global recognition.

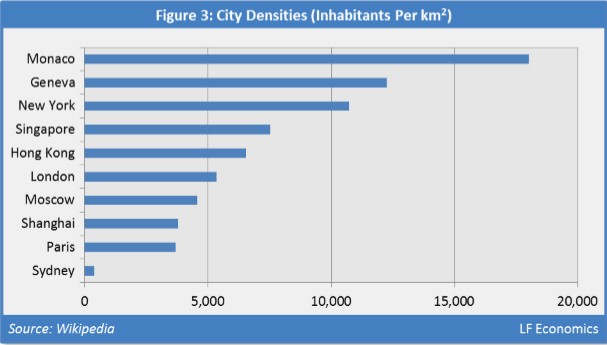

Australia’s largest capital city, Sydney, has one of the most expensive real estate markets in the world but does not share common density or economic characteristics of other cities that are globally recognized for having expensive real estate markets. These include cities such as London, New York, Paris, Monaco and Hong Kong. If Sydney were as densely populated as London, the city would have a population of close to 64 million inhabitants.

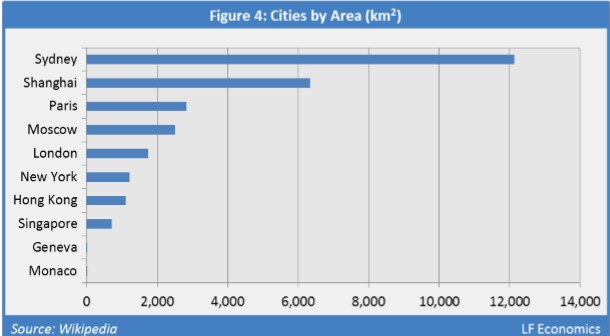

The two following tables illustrates that Sydney shares no physical characteristics in terms of city density and area relative to other expensive real estate markets. The first table illustrates the density (inhabitants per km2) of global capital cities.

Second, by area, Sydney is located on an incredibly large landmass…

The shortage argument, however, is not new. Every country that has suffered through a housing cycle in recent years had so-called experts claiming capital prices were based upon fundamental factors of supply and demand. Unfortunately, economists considered these housing price booms to be efficiently based, so there was no need to actually test for a shortage – they are considered to exist by definition…

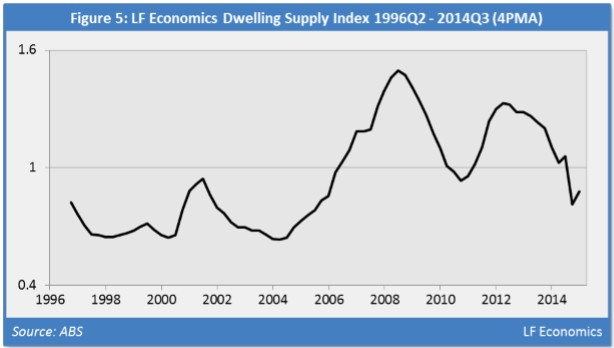

The best method to determine whether a surplus or deficit exists is to compare the flow of new net dwellings to new net households, once appropriate adjustments have been made… we have chosen the baseline for our analysis as 1996Q2, when real housing prices began to rise. The latest data point available is 2014Q3…

Between 1996 and 2014, Australia was required to build a new dwelling for every 2.6 new residents to sufficiently accommodate its growing population. So has Australia built enough housing?…

The LF Economics Dwelling Supply Index is interpreted as following: a value of 1 indicates a balanced market, a value less than one indicates a surplus, while a value greater than one indicates a shortage. A 4-period moving average has been used to smooth the volatility of the data series.

It shows, for the majority of the housing price boom, the national housing market was in surplus. Between 1996 and 2014, Australian housing prices, adjusted for inflation and quality, surged by 121 percent. Yet, 86 percent, or almost three-quarters, of that boom occurred over a ten-year period between 1996 and 2006 when the housing market was in persistent surplus…

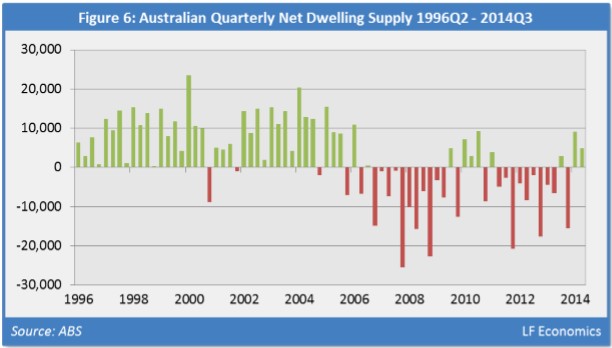

Figure 6 transposes the results from Figure 5 to illustrate the trend in net supply on a quarterly basis. As the LF Economics Dwelling Supply Index demonstrated a persistent value of <1 between 1996 and 2006, the results shows the surplus in absolute values (green). After 2006, the housing market has experienced mostly deficits (red)…

Of particular concern is Victoria, which has experienced the biggest housing price boom of all the states and territories, but yet has the largest cumulative oversupply of dwellings at 123,000. This is equivalent to approximately three years’ worth of extra supply…

There is clearly little evidence to suggest there is a profound connection between the supply of dwellings and the rampant housing price inflation Australia has experienced since 1996. In future reports, LF Economics shall demonstrate there is a significantly stronger connection between housing price growth and the availability of household credit, economic conditions and interest rates in contrast to the overall supply of dwellings…

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.