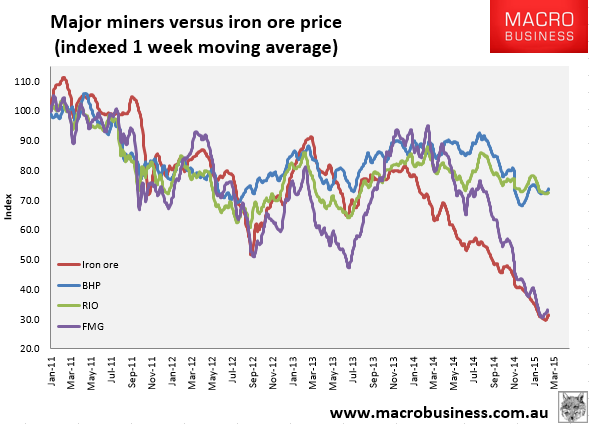

Big iron has hit a wall today. BHP is flat and RIO down 1% though FMG has managed a 1.5% gain. To the indexes:

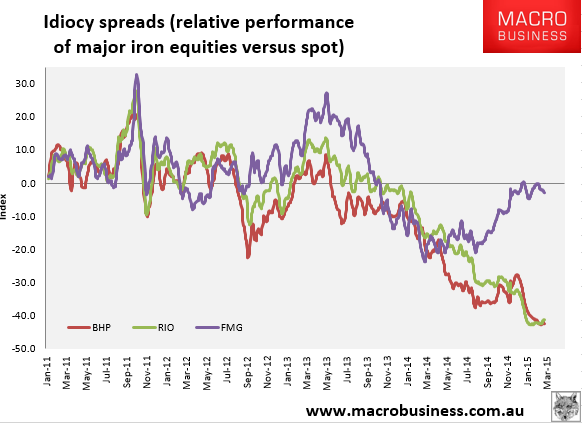

The idiocy spreads are roughly flat with the exception of FMG which is widening:

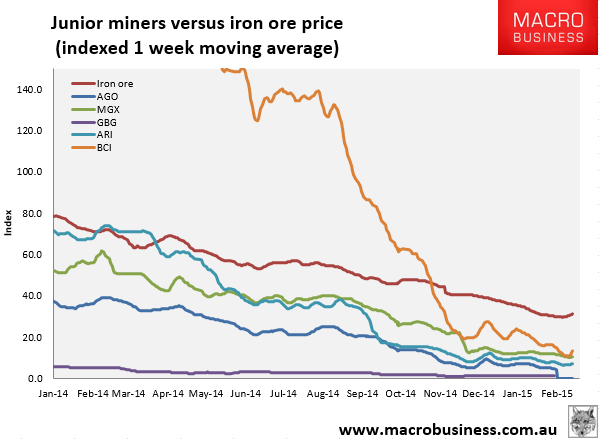

Juniors are becalmed but not before BCI doubled from 26 cents to 52 cents for no reason at all:

Dalian is still up 5 points at 433 from yesterday’s close suggesting another move towards $60 in tomorrow’s price.

So, time to short already? BCI looks like a sitting duck.

I see one possible spur for the bear market rally to get another leg up. The PBOC is clearly getting set to launch new policies that enable it to buy local government bonds. This is already being couched in the media as Chinese QE even if it really isn’t anything new.

China has effectively been doing QE for years via its currency peg which requires the central bank to buy US dollars from banks thus liquefying them with an excess of yuan. As that QE eases down owing to capital flight it is inevitable that it will need to be replaced elsewhere in the economy to control the growth glide slope and it looks like it’ll be via monetisation of local government bonds. Regardless of its ultimate relevance, in the current excited environment that announcement, should it come, will kick the bear market rally along.

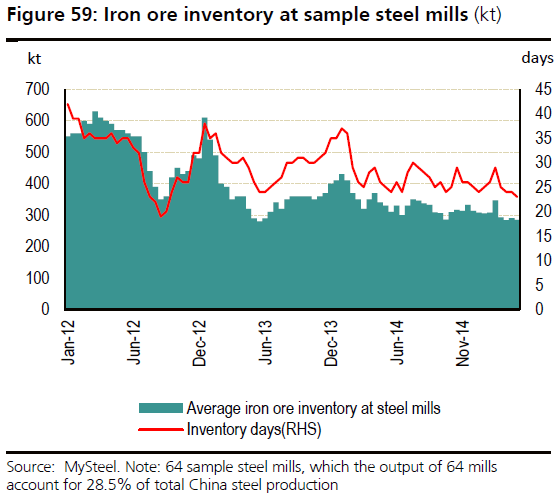

The other consideration is how long will steel mills take to restock? The following UBS chart shows that inventories had fallen quite low before the short squeeze:

Mills will now restock to 27-28 days of iron ore inventory from 22 days. That will take a few more weeks.

The base case then is that the rally has another couple of weeks to run. After that I’d expect price erosion as RIO’s next supply deluge arrives and then another price cliff in Q3 as Roy Hill joins just as the ongoing fade in Chinese property hits the seasonal steel production slowdown.