FMG is now guiding to a C1 cash cost of US$18/t in FY16 – which is lower than BHP and RIO’s last reported halves. However, BHP and RIO will probably also surprise, and deliver cash costs below US$15/t this year. Lower costs may not help margins – it may just result in a lower long-term iron ore price.

…We have increased earnings in-line with FMG’s new cost guidance, but have assumed the low costs are not sustainable long term. Our valuation increases from A$1.00ps to A$1.60ps.

Today it’s Morgans which was hopelessly bullish on iron ore all the way down and has now upgraded FMG to “hold”. And Bell Potter which has famously backed FMG through enormous equity losses and only just downgraded the failing miner two weeks ago.

Finally today, Morgan Stanley joins the stampede:

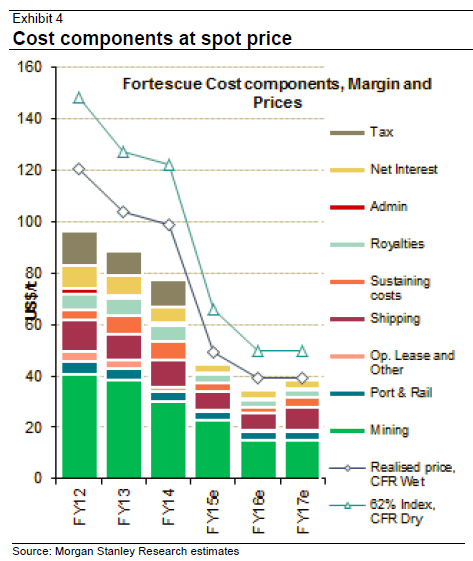

Magnitude of the cost-out a shock, but accepted:

The 28% reduction in C1 costs to US$18/t (vs. prior JH guidance) exceeded the estimates we had considered.

…If peers match FMG, lower iron prices could occur: If not, FMG should survive the cycle; otherwise the cost curve shifts lower, pressuring the commodity price, and, in turn, FMG’s FCF. This concern keeps us from becoming more positive on the equity at this time.

Large moves in the EPS on the new cost base:

Applying the lower costs pushed our EPS forecasts up 6-23cps, and our PT is up 30% to A$2.14/sh. We are once more above consensus.

FMG has always executed brilliantly but that is not the issue. No matter how it tries, it is very unlikely to be able to displace any iron ore from RIO, BHP, Vale, Roy Hill, or Sino. Anglo is almost as questionable.

Advertisement

That means it is the only miner large enough to have a material impact on the supply imbalance so until it dies the price will just keep falling as all of its cost out efforts drive everyone else to do the same.

FMG must die so that the iron ore price can live. It’s written in stone.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.