This AFR article also contained analysis from the Property Council of Australia (PCA), which claimed that Australia’s lower-paid workers are the primary beneficiaries of negative gearing, rather than it being the domain of the rich.

The latest available data from the Australian Taxation Office is indisputable and it shows that some of Australia’s most valued, but lower paid workers are the primary beneficiaries of negative gearing.

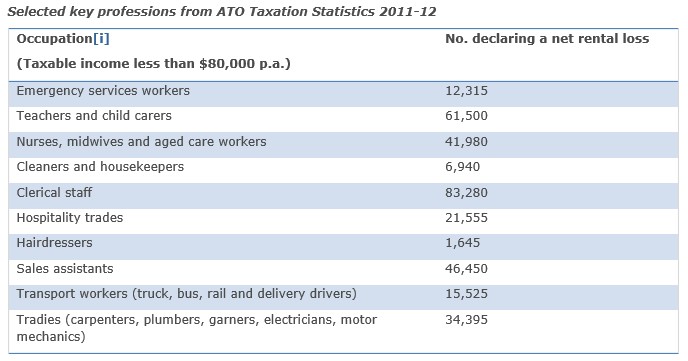

This includes the 42,000 nurses, midwives and aged care workers, 62,000 teachers and child carers, 12,300 emergency service workers and 83,000 clerical staff, who all earned around or under $80,000 p.a. and negatively geared a property in the 2012 Financial Year.

It is misleading to claim that these people only earn under $80,000 p.a. because they substantially reduce their gross taxable income.

A detailed analysis of the ATO Tax Statistics shows, for example, that 8,885 registered nurses, 3,120 primary school teachers, 2,880 secondary school teachers, 3,350 education aides, and 2,945 child care workers all declared a net rental loss and had a taxable income of between $6,001 and $37,000 p.a.

“The data clearly shows that negative gearing is something middle Australia uses to help build their household wealth, build for their future, and provide security for their families,” said Chief Executive Ken Morrison.

“Negative gearing provides an opportunity for average working Australians to save to get ahead.

“Demonising negative gearing, or disregarding its substantial benefits – in terms of household and retirement savings, stimulating housing supply and rental affordability – willfully disadvantages some of the hardest working, lowest paid people in the country…

“These people aren’t the rich and famous, nor are they property barons, but they do deserve a fair go and that’s why negative gearing must remain.”

It’s another excellent piece of propaganda run by the Property Industry, isn’t it? Because there are 325,585 ‘Aussie battlers’ with taxable incomes below 80,000 – i.e. incomes below $80,000 afterdeducting their negative gearing losses – negative gearing should not be touched, despite its significant cost to the Budget and its inflationary impact on house prices, which of course means that the battlers the PCA cares so much about must also pay more to put a roof over their head!

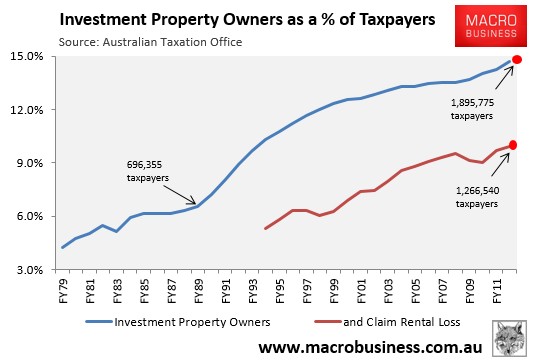

The problem for the PCA is that there were 1.26 million Australians that claimed rental losses in 2011-12 (see next chart), and any objective analysis shows that the lion’s share of these negatively geared investors were higher income earners.

Advertisement

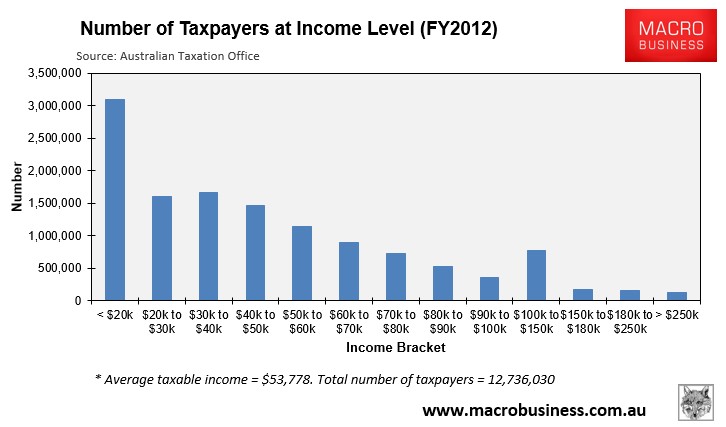

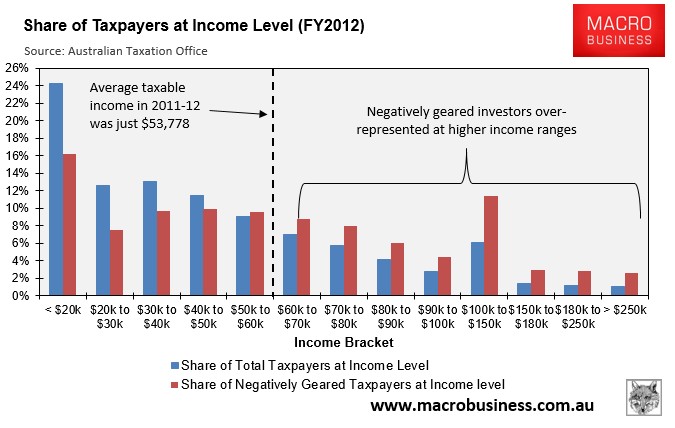

To illustrate, consider the next chart showing the breakdown of Australians that lodged tax returns in 2011-12 broken down by taxable income:

Advertisement

According to the ATO there were 12,736,030 individuals that lodged tax returns in 2011-12 with the average taxable income just $53,778 – well below the $80,000 threshold used by the PCA.

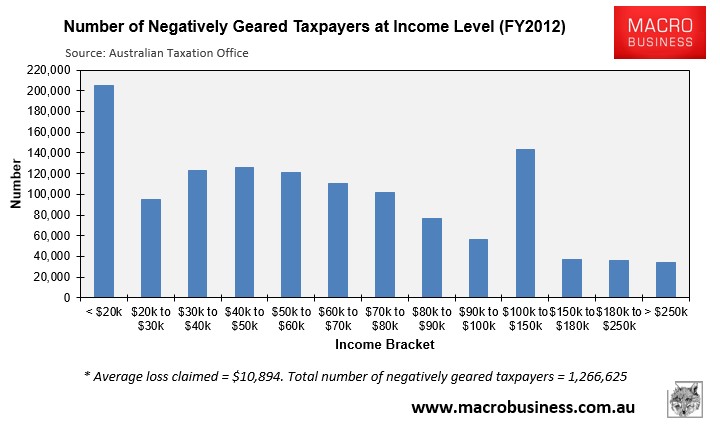

Now consider the next chart showing the distribution of negatively geared investors by taxable income range, whereby each negatively geared investor claiming an average loss of $10,894 in 2011-12, which of course reduced their taxable income:

Advertisement

Combining these two charts, and converting each series into their percentage share of the total gives the following distribution:

As you can see, negative gearing was significantly under-represented at the lower income levels and over-represented at the higher income levels in 2011-12.

Advertisement

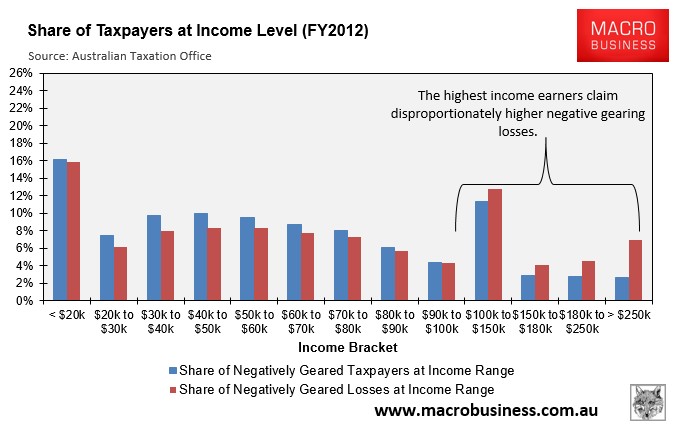

The picture gets even worse when one considers the share of total negative losses claimed at each taxable income level. As shown below, higher income earners – who are already over-represented in their negative gearing activities – claim an even higher share of the negative gearing losses:

All of which smashes the PCA’s claim that negative gearing is primarily the domain of the ‘Aussie battler’, which is clearly false. The number of negatively geared property investors increases with income, and the value of losses claimed even more so.

Advertisement

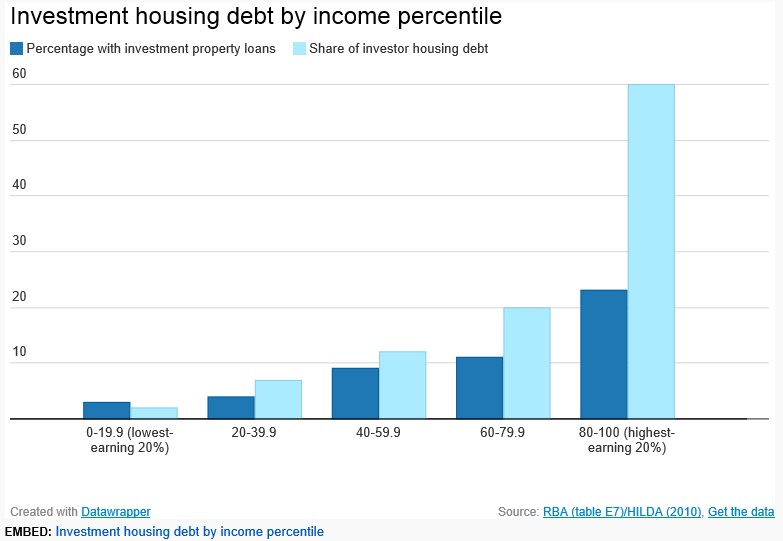

Of course, the ABC’s Michael Janda already debunked the PCA’s claims last year when he used Household Income and Labour Dynamics in Australia (HILDA) data to show that a whopping 60% of investment housing debt is held by the top fifth of income earners and that investment housing loans are more than twice as common amongst the top 20% of income-earning households than any other income group:

Make no mistake, negative gearing is used disproportionately by higher-income Australia’s to avoid paying tax by speculating on housing.

Advertisement

It is a wasteful use of scarce taxpayer funds that has forced-up the cost of housing in Australia to the detriment of middle and lower income families.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.