From Moody’s:

Moody‘s Investors Service has lowered its price sensitivities for iron ore and metallurgical (met) coal, the rating

agency says in a new report. The changes come in response to slowing steel production in China and rampant oversupply, particularly of iron ore, which will keep prices low through at least next year.Moody‘s downside price sensitivities for iron ore are now $40 per metric ton for both 2015 and 2016, and for met coal $100 per metric ton in 2015 and $110 per metric ton in 2016.

“Companies’ earnings will be materially affected by the lower prices for met coal and iron ore,” says Senior Vice President, Carol Cowan. “But the price sensitivity changes alone won’t result in wholesale rating changes, though the likelihood of outlook or rating changes is increased.”

Moody‘s-rated companies will be evaluated on a number of factors, including their ability to reduce capital expenditures or other cash outflows to achieve at least a breakeven free cash flow position, their liquidity position, and their debt maturity profile, Cowan says in “Iron Ore, Met Coal Drowning in Oversupply With More on the Way.”

“Slower global economic expansion, particularly in China, which accounts for approximately 50% of global steel production, will continue to limit growth in steel demand, while at the same time iron ore and met coal, two key raw material inputs, are in oversupply.”

Production of iron ore continues to increase particularly in Australia and Brazil, with the reasons for this including a desire to maintain market share and expectations that high-cost producers will be forced to exit the market, while the lower costs associated with higher volumes help mitigate price declines.

While some capacity has come out of the iron ore market, the shut-downs pale in comparison to the expected new supply, Moody‘s says. Met coal likewise remains in oversupply, and US met coal producers’ announced cuts are taking longer than expected to be implemented.

And FMG slides deeper into junk:

Moody‘s Investors Service has downgraded

Fortescue Metals Group Ltd’s corporate family rating to Ba2 from Ba1. At the same time Moody‘s has downgraded FMG Resources (August 2006) Pty Ltd’s senior unsecured rating to Ba3 from Ba2 and senior secured rating to Ba1 from Baa3.The outlook on all ratings is negative.

RATINGS RATIONALE

“The downgrade of Fortescue’s corporate family rating reflects the very weak iron ore fundamentals and our expectation that iron ore prices will remain around the current weak levels through 2016”, says Matthew Moore, a Moody‘s Vice President and Senior Analyst. “Such price levels will lead to a substantial weakening of Fortescue’s earnings and key credit metrics compared to our previous expectation”, adds Moore.

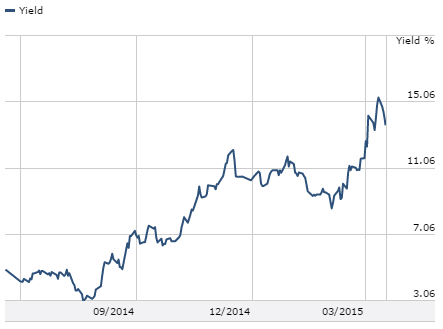

No shit! Let’s see what this does to FMG bonds. Yesterday saw the 2019 yield crash below 14%:

It’s all good!