The Reserve Bank of New Zealand’s (RBNZ) quarterly Bulletin contained the below interesting excerpt explaining how a low inflationary/interest rate environment prolongs the pain associated with high household debt, increasing financial stability risks in the process:

In addition to being more exposed to shocks due to high debt levels, households can also be exposed for longer when there is low inflation (Debelle, 2004). When inflation is low the real value of debt erodes slowly, and for a given household, the debt-to-income and debt servicing ratio (principal and interest payments relative to income) also decline more slowly over the life of the mortgage.

Households could be surprised in later years by the share of income still required to service debt. With debt service therefore persisting as a significant share of income for a longer time, it is more likely that the average household will experience a period of unemployment during that time, all else equal.

It is possible, for example, that some younger households buying property today believe that house prices reliably rise (even relative to incomes), based on their parents’ experience as homeowners. They may also be comfortable with a large share of income being used to repay the mortgage, because their parents’ generation, which faced interest rates as high as 20 percent or more, also experienced that situation. However, for that generation, high inflation during the 1980s meant that mortgage payments quickly diminished relative to nominal income. Assumptions based on a relatively short historical experience can lead to the burden associated with mortgage debt being underestimated.

The RBNZ has touched upon something that is not well understood by baby boomers, many of whom wrongly believe that today’s low inflationary/interest rate environment is a boon for young home buyers and means that affordability is no worse today than in yesteryear (I’m looking at you, Malcolm Maiden).

The fact is, when most baby boomers purchased their first homes in the 1970s and 1980s, inflation was high, which meant that their debt loads were eroded quickly as their incomes caught up. What seemed like a large mortgage at the time quickly became a small mortgage, thanks to inflation and centrally indexed wages.

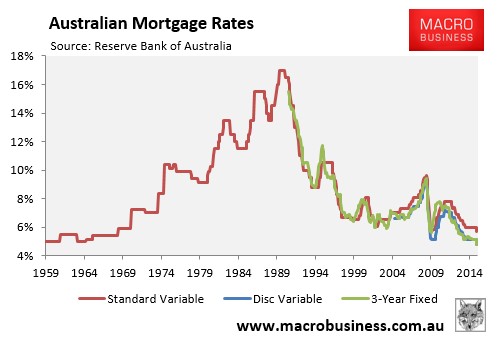

By contrast, today’s first home buyer faces a low inflationary environment, and with it, record low nominal interest rates (see next chart). However, because inflation and wages growth are so low, it means that today’s mega-mortgage will still be a large mortgage in a decade’s time, extending the pain felt by today’s younger generations.

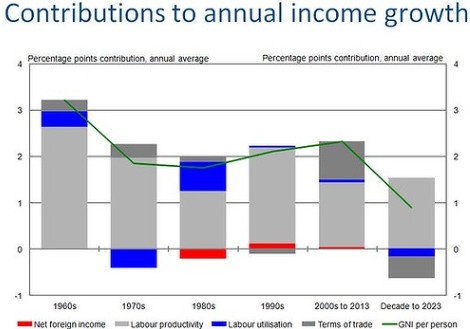

Indeed, as noted by the Australian Treasury last year, average income growth is expected to be the weakest in at least 60 years over the coming decade, which is going to make paying-off today’s mega mortgage far more difficult (see next chart).

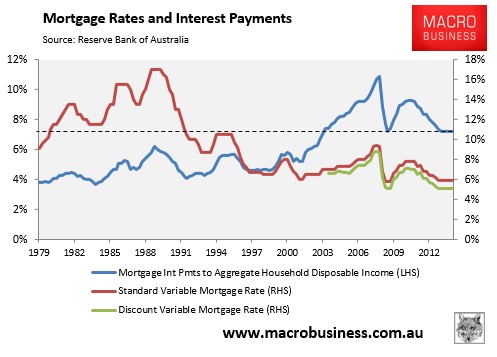

It might surprise some readers that despite the lowest nominal mortgage rates in history, the humungous stock of outstanding mortgage debt has meant that today’s mortgage slaves are sacrificing a higher proportion of their disposable incomes servicing their mortgage debts (let alone principal) than when nominal mortgage rates were at 17% (see next chart).

As shown above, the proportion of aggregate household disposable income being sacrificed on mortgage interest repayments was 7.2% as at December 2014 – 17% above the late-1980s peak!

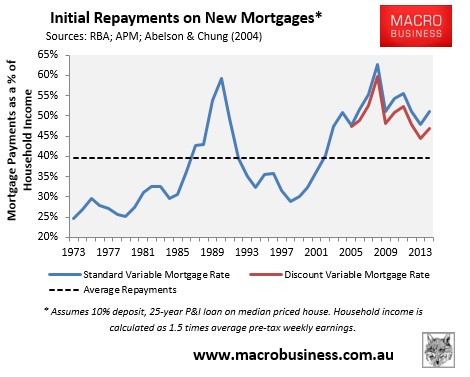

Further, while initial repayments on new mortgages are lower than the late-1980s and early-1990s, they remain well above the 40-year average (see next chart). And remember, these high debt loads will still be around in a decade, thanks to low inflation and anaemic wages growth.

Rather than being a benefit to today’s home buyers, the low inflation/interest rate environment that exists today is a curse that will act as a millstone around their mortgaged necks for decades to come.