Andrew Preston, senior investment manager at one of BHP Billiton’s biggest shareholders, Aberdeen Asset Management, says investors will likely continue to support the rapid iron ore expansion strategies being run by BHP and Rio, as long as the two miners continue to make money.

Now that’s a question and not an entirely facetious one. Hear me out.

All media today focuses on one aspect of the crash, the big miners, from Bloomie:

“There’s a bit of a self-destructing behavior by the big miners,” Philip Kirchlechner, former head of marketing at Fortescue and former chief iron ore representative at Rio Tinto in Shanghai, said by phone on Monday. “They’re overproducing in the face of slowing demand conditions. And it’s hard to understand such behavior,” said Kirchlechner, director of Iron Ore Research Pty in Perth, Australia.

…“Mr. Forrest probably does speak the truth, in our view: the Big Miners can influence prices, if they could somehow (legally) act together to restrict supply growth,” Morgan Stanley analyst Tom Price wrote in a note, referring to Fortescue, Rio, BHP and Brazil’s Vale SA. The four control about 70 percent of global seaborne trade, Price wrote.

And the AFR:

Advertisement

…But Tim Schroeders, head of resources at Pengana Capital, said Mr Forrest’s comments “put more doubt on Fortescue than it does on either BHP or Rio”.

BHP and Rio were “clearly re-positioning their businesses, and eking-out synergies and de-bottlenecking the whole value chain”. Pengana Capital is an investor in both BHP and Rio.

Will they or won’t they? Should they or shouldn’t they? My answer is who cares.

The miners are not in control of the shakeout. This is not cyclical change, it is structural and there are five reasons why.

The first has been much discussed. Chinese steel demand has peaked. Assuming it falls 3% this year that will wipe out 40mt of iron ore demand, more than enough to offset any decline in local iron ore production.

The second reason is oversupply, which is already vast at around 50-100 million tonnes per annum with a mid-point that is 6% of the total seaborne market and 8% of the Chinese seaborne market. This is roughly as bad as the coking coal surplus at its worst. It fell 70% from its highs and a similar calculation gets us to mid-$50s for iron ore. So we’re near the bottom, right?

Alas, no. Coking coal is now falling again even though it’s spent several years shaking out supply. The reason is weak demand which has dissolved seller’s pricing power yet again.

For iron ore the calculus is much worse. The surplus is set to grow by another 100mtpa within 9 months. With a decline in steel demand effectively neutralising attrition in Chinese iron ore supply, that means the seaborne market surplus ratio will double to 11% globally and an astonishing 15% of total Chinese imports.

We will see junior shut-ins probably totaling 25mtpa this year, leaving a now reasonably competitive Anglo, Sino, Fortescue, Roy Hill, BHP, RIO and Vale fighting over the rest. That’s a lot of competition within a cartel, which is structural change number three.

The fourth structural change is that the traders that used to hoard iron ore the moment its price fell have all but disappeared. Sure the big trading houses are still operating. But competition has reduced their leverage too and tight Chinese credit materially reduced their influence. The broader community of traders in China has been prudentially targeted to achieve this end.

Contrary to the claims of Fortescue management that it’s all about pot-smoking short-sellers, this has left Chinese steel mills and their inventory management in complete control of the market. Iron ore is now far less of a speculative commodity than it has been since the price was floated and the result is that supply and demand are going to clear the market via price whatever that needs to be.

The final structural change is a reversal of the pro-cyclical polarities of the market. As prices rise, so do labour and hard capital costs, taxes and royalties. As prices fall the whole thing reverses. Labor, hard capital, royalties and taxes all tumble with the price. This enables miners to survive for far longer than expected. Cheap oil makes it worse.

The upshot is that there has never been such a current and pending surplus, nor such competition, nor such a boom and bust cycle in a bulk commodity and we really don’t know what it will do to the price. Cost curve and cyclical analysis is meaningless. Just about the only thing that gives us any guide to where the bottom is the respective balance sheets of big miners:

- BHP, RIO and Anglo have deep pockets

- Sino is state sponsored

- Roy Hill is a matter of pride for the world’s richest woman

- Vale is in trouble because its expansion is debt-funded and too late but it’s a formerly state-owned firm surely too big to fail

- there is only FMG and its debt pile but if it gets state sponsorship as well then the price must keep sinking.

On the back of an envelope, FMG has a breakeven somewhere in the mid-$50s but there are many ways to lower it short term so let’s say it can get it down to mid $40s in a panic and continue on even lower at marginal costs. That means we’ll need a price at $30 for ten months for it to run out of cash. But that’s only a wild guess. It could be higher for longer or lower for shorter. If the Chinese elect to save it then we’ll be going considerably lower for considerably longer.

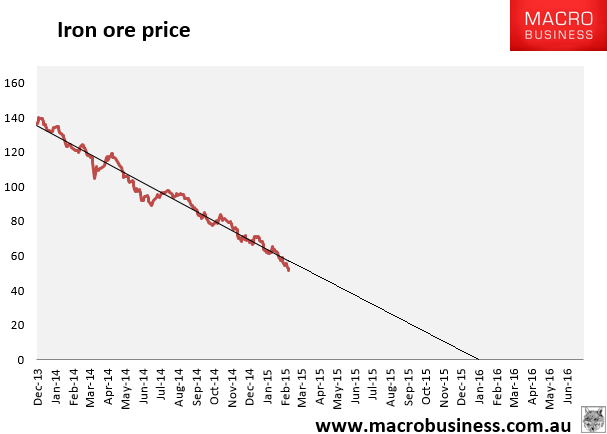

Back to my original question, then, the trend tells us we will be at zero by January next year:

That’s not going to happen but the bottom is much lower than anyone is currently contemplating, will be more enduring than everyone’s darkest fears and it appears we’ll very likely get there by Christmas.