Brent oil rallied to a new high of $65.40 Friday. The main causes were some short term supply disruptions in Libya and further declines in the US rig count down 22 to 932:

The falls are definitely beginning to flatten out but the US shale production peak is also in sight. But for how long? With prices already into the mid-$65s and marching higher in the short term, US shale can swing back into production very quickly and nearly all of it is profitable at $80. The oil price rally is well ahead of fundamentals in my view, an argument shared by Citi:

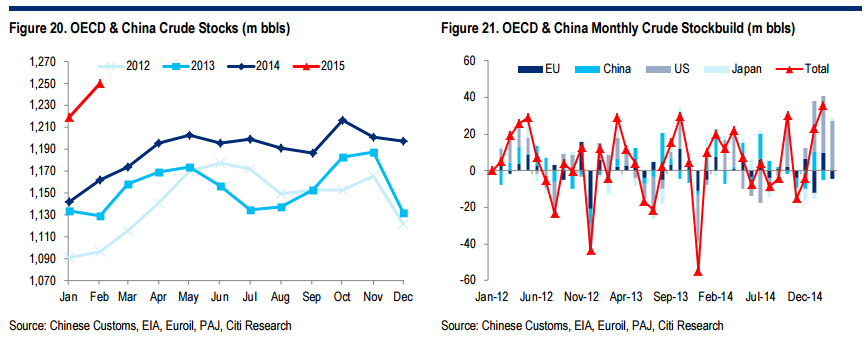

The oil market remains significantly oversupplied, yet macro waves of liquidity are buoying prices (as can be seen in the record managed money net length in Brent); the risk to the market is now that the rally has come too soon for supply to get meaningfully curtailed; raising the prospect of another price slump in 2H’15. The drop in the US rig count has bolstered enthusiasm for the rally and the recent weekly EIA data are taken as confirmation that US production is already rolling over yet Citi has repeatedly stressed that the weekly numbers on production are an estimated output of a model, rather than being observed data. Combined with a pause in the USD rally and some indications of better demand, this appears to be enough to let oil prices continue to make new highs for this year for the near future. Yet this rally is going to have consequences for the rest of the year. Painfully low prices were deemed a necessary corrective to address the oversupply which threatens to overwhelm storage capacity; the liquidity enthusiasts are similarly threatening to overwhelm the bearish market specialists, as can be seen in the withering gross money manager shorts in WTI.

Advertisement

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.