Some bright young spark at Bloomberg has declared that iron ore is in a new bull market:

Iron ore advanced into a bull market after BHP Billiton curbed expansion plans and supplies from higher-cost mines dropped, easing concern global output will outpace demand and feed a global glut.

Iron ore jumped this week after BHP said it was curbing the pace of its expansion by deferring port works in Australia. A floor in prices may now be forming, according to Australia & New Zealand Banking Group Ltd. and Pacific Investment Management Co. There’ll be no net growth in supply in 2015 as new low-cost output is offset by mine closures, CLSA Ltd. said on Tuesday.

“The major Australian producers are sending a signal that expansions are slowing, so the oversupply will start to ease,” Wu Zhili, an analyst at Shenhua Futures Co. in Shenzhen, said by phone on Friday before the price data was released.

One doesn’t wish to disparage this hope but it is indicative of just the opposite. Last week’s explosion of iron ore prices and exuberance, as well as the fantastically thin excuses doled out to explain it, is not characteristic of a bull market. Such high irrationality and volatility is the stuff of historic bear markets.

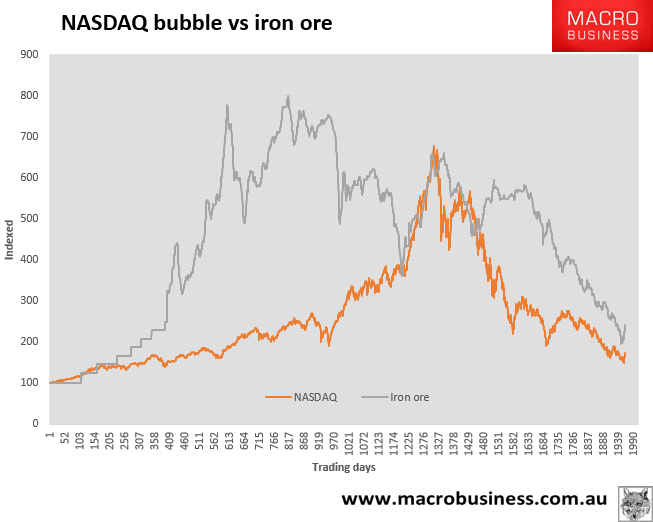

To explain I’ve charted below the course of the iron ore boom against the NASDAQ bubble and bust of the millennium:

The purpose of this juxtaposition is not to declare that iron ore is or was a bubble, we can leave that to the historians, but to make two points:

- the iron ore boom was among the greatest bull markets of all time, and

- great bear markets are full of bull traps on the way down.

The chart is indexed to 100 so captures percentage moves. Note the huge rallies in the NASDAQ as various points on its way down, some as great as 100%, as markets declared the bear market over. Iron ore has also enjoyed several moves of magnitude similar to last week in its decline.

A persistent bear market remains clear in the fundamentals. As I noted many times last week, the sudden flowering of optimism around iron ore has actually condemned it to an even worse fate given it helped Fortescue refinance its debt, extending oversupply. Thus, in terms of the above NASDAQ analogy, my guess is that we are somewhere around day 1600. Lots of steep damage done, a bull trap in full roar, yet a rough halving of prices (or more) still in prospect.

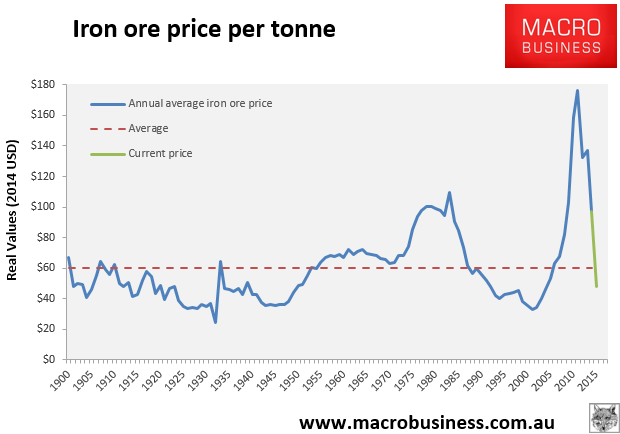

Those seeking a new “price floor” because iron ore has “overshot” are kind of right. The average real historic price for iron ore is $60:

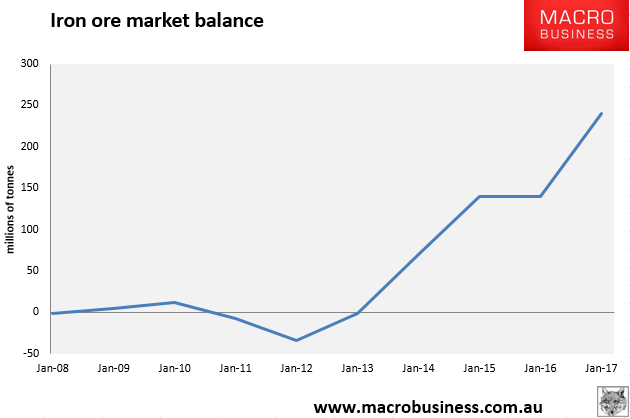

But that’s not the point. The question that needs to be asked is how big an overshoot for how long will be needed to clear the market of oversupply? The above history of real iron ore prices shows that overshoots can run very deep and literally for decades, and the impending oversupply of this cycle is gigantic. Perhaps 70mt today. Double that by year end. More than triple within two years:

The assumptions behind this chart include:

- Chinese steel output falls 2.5% per year;

- Chinese iron ore output falls from 330mt to 25omt;

- all global iron ore juniors in the seaborne market are wiped out in the next 18 months, and

- Sino, Anglo, Roy Hill, Fortescue, RIO and BHP are left to duke it out.

More conservative assumptions don’t change the picture much. If Chinese steel output remains stable and its iron ore output falls to 200mt then 2017 oversupply is still 150mt. And the bigger risk is probably the reverse, that Chinese steel output falls faster and keep falling after 2017.

There is no way that all major iron ore producers can survive. You can pick your winners and losers but if 150-250mt has to be shut-in to find a market balance among these six miners, the clearing price is going to have to go much lower.

The present rally is good value for well-timed longs but don’t be fooled, Australia is still only part way through one of the greatest bear markets in history.