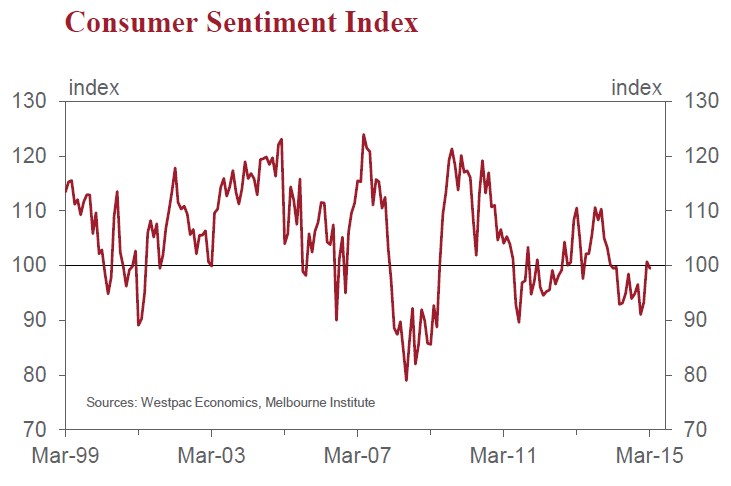

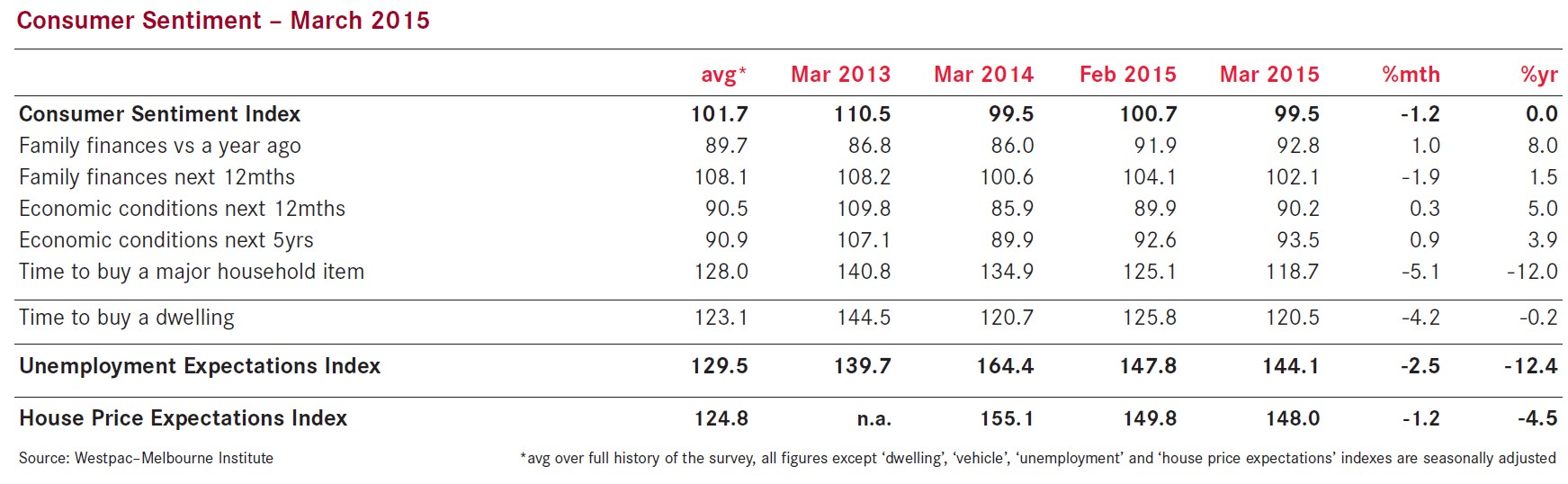

The Westpac–Melbourne Institute Index of Consumer Sentiment for March has been released, with sentiment dropping 1.2% over the month from 100.7 to 99.5, with pessimists now slightly outnumber optimists:

Some softening in sentiment was always likely in March given the big lift last month following the RBA’s surprise 25bp rate cut. Interest rate moves often generate a big initial reaction that dissipates over time. That pattern may have been dampened this time by the Reserve Bank’s move to an overt easing bias at its March meeting although many, including ourselves, had been expecting the Bank to make a further 25bp cut in rates.

The Index remains 9.2% above its December low and is on a par with the levels seen prior to the Budget in May last year.”

Other factors likely contributed to the softening in sentiment this month. In particular, petrol prices rose sharply in the month, pump prices up 14c a litre, reversing most of the 22c decline over the previous two months. The December quarter national accounts also presented another weak read on the economy with growth of just 0.5%qtr and 2.5%yr, the economy expanding at a sub-2% annual pace through the second half of the year. While disappointing, the December figures were less of a shock than the September quarter national accounts which saw many media references to an ‘income recession’.

These themes show through clearly in consumer responses to additional questions on news recall. These questions are included in the survey every three months. The last time they were run, back in December, the most recalled news topics were: ‘economic conditions’; ‘budget and taxation’; ‘international conditions’ and ‘employment’ with respondents assessing news on all of these topics as extremely unfavourable. Indeed, assessments were amongst the most negative responses recorded in the survey history back to 1975.

Responses in March continue to show high recall rates on these topics: ‘economic conditions’ (40% of respondents); ‘budget and taxation’ (42%); ‘international conditions’ (17%) and ‘employment’ (31%). However, the news on these issues is assessed as less dire than in December and counterbalanced by news around interest rates, recalled by over a third of respondents and seen as broadly ‘neutral’ rather than unfavourable.

The overall message seems to be that while consumers remain very concerned about the outlook for the economy and job security, they are less concerned than they were in December and acknowledge the more positive situation around interest rates. Individual components of the index were mostly stable between February and March. The sub-indexes tracking views on family finances were mixed with ‘finances vs a year ago’ up 1% but ‘family finances, next 12 months’ down 1.9%. Views on the economy improved marginally with the sub-indexes tracking expectations for ‘economic conditions, next 12 months’ and ‘economic conditions, next five years’ up 0.3% and 0.9% respectively.

Assessments of ‘time to buy a major household item’ were a notable weak spot this month with this sub-index falling 5.1% to be 9.3% below its long run average. While this is still well above its December low, March’s reading is the second weakest since 2009. It is very likely that at least part of this decline is a reaction to recent falls in the Australian dollar and the impact this is expected to have on the cost of imported goods.

Consumers are becoming less fearful of rising unemployment, although labour market expectations are still very weak. The Westpac-Melbourne Institute Unemployment Expectations Index declined 2.5% to 144, marking a 9.7% improvement since December (recall that a higher level indicates more consumers expect unemployment to rise over the next 12 months). This is the best reading since October 2013 but still well above the long run average reading of 129.5.

Views on housing softened after February’s rate cut induced rally. The index tracking assessments of ‘time to buy a dwelling’ fell 4.2% in March, reversing about half of last month’s 9.7% gain. At 120.5, buyer sentiment is a touch below its long run average of 123 but notably firmer than the average 113.4 read over the second half of 2014. It is a similar story around price expectations: the Westpac-Melbourne Institute House PriceExpectations Index dipping 1.2% in March but following a sharp 6.9% gain in February. At 148 the Index is still in solidly positive territory with over 61% of consumers expecting prices to rise over the next year.

Respondents have become less risk averse in their preferences for their savings. The proportion of respondents nominating ‘bank deposits’ as the wisest place for savings declined from 37% in December to 29.8% in March with a corresponding rise in the proportion nominating ‘real estate’ from 20% in December to 25.5% in March. The proportion of consumers favouring ‘pay down debt’ declined marginally from 17.6% to 16.5%. The overall mix of responses is very similar to that seen in September last year.

The Reserve Bank Board next meets on April 7. We continue to see a clear case for lower rates. Although there were some encouraging details in the December quarter national accounts, growth momentum remains well below the Reserve Bank’s assessed ‘trend’ pace of 3.25%. There are also some encouraging details in the March Consumer Sentiment survey. However, confidence remains lacklustre overall, with sentiment neutral rather than optimistic and, we suspect, still quite fragile. With concerns that sub-trend growth may persist for longer than had been assumed through most of last year, that points to continued downside risks to the outlook. In effect, neither the national accounts nor sentiment have delivered enough ‘good news’ to tilt the balance of risks back to even. As such, we continue to expect another rate cut of 0.25% in the April/May ‘window’.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.