Cross-posted from The Conversation:

The half of the Australian population that has private health insurance can expect higher bills from Wednesday, as premiums increase by an industry average of 6.18%. The increase varies across different funds, ranging from 3.98% to 7.92% and will add around A$200 to A$300 a year to the average cost of hospital cover for families.

The increase is two to three times higher than inflation. So, how can the government approve such a hike? And how much profit are private health insurance companies making?

How are premium increases determined?

Under the Private Health Insurance Act 2007, health funds must apply to the health minister to change their premiums. The industry regulator, the Private Health Insurance Administration Council, individually assesses the applications and refers them to the minister.

To justify their application, health funds are required to provide projections of the anticipated changes in premium revenue and benefits outlay, and information about the financial performance of health funds, including operating margins and management expenses.

Premium increases are often justified as being necessary to ensure the solvency of health funds, and to maintain sufficient underwriting margins to meet its obligations.

The Act states the minister must approve the proposed change, unless it’s deemed as contrary to the public interest. The new premium rates come into effect each April.

So, what case do insurance companies have?

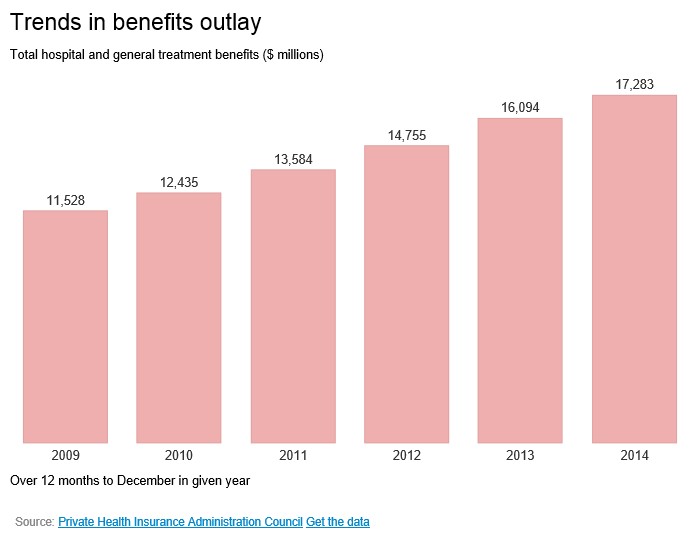

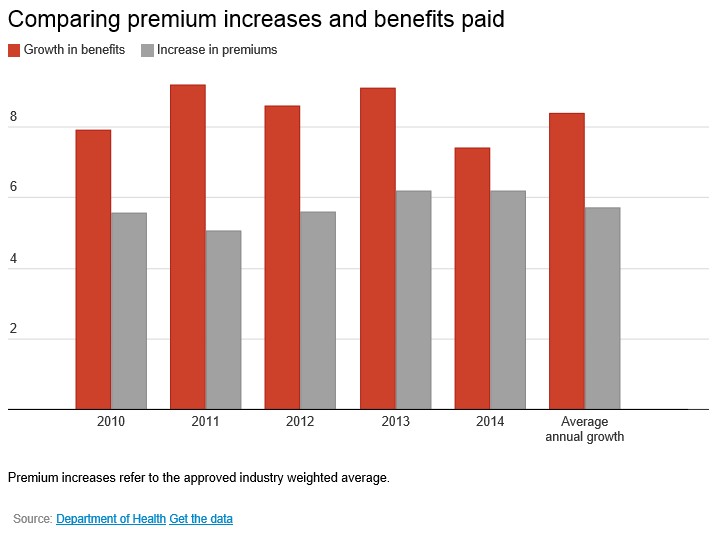

Premium increases vs benefits paid

The table below shows the total benefits paid by health funds for hospital and general treatment from 2009 to 2014. Over the six year period, benefits outlay grew by between 7.4% and 9.2%, with an average growth rate of 8.4% over the period.

This next table shows the approved (industry weighted) average increase in premiums. In every year, the increase in benefits paid out by health funds far exceeds the approved increase in premiums.

Benefits paid by health funds are influenced by the number of hospitalisation episodes (for things like hospital accommodation and operating theatre fees) and the number of general treatment services provided (such as physiotherapy visits), in addition to the level of benefit that each of these services attract.

In 2014, the number of hospital episodes and general treatment services grew by 5.2% and 3.9% in 2014, whereas total benefits paid in the same year increased by 7.4%.

This suggests that the growth in benefits is driven to a larger extent by an increase in the number of claims made, and to a smaller degree an increase in the average size of claims.

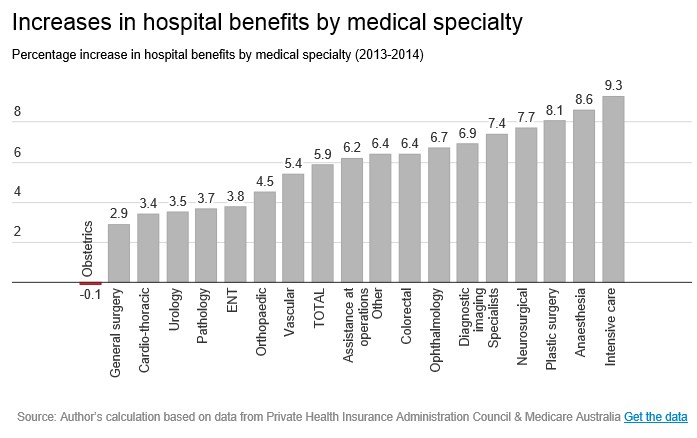

Where are the growth areas?

From 2013 to 2014, intensive care and anaesthesia grew by 9.3% and 8.6% respectively; the largest increase in benefits paid.

These increases are significantly higher than the average growth of 5.9% for all services.

On the other end, benefits for obstetrics actually fell slightly by 0.1%, and those from general surgery increased by 2.9%.

Are health funds making excessive profits?

With consecutive premium increases year on year, it’s reasonable to ask if health funds are making excessive profits. But it’s a difficult question to answer satisfactorily.

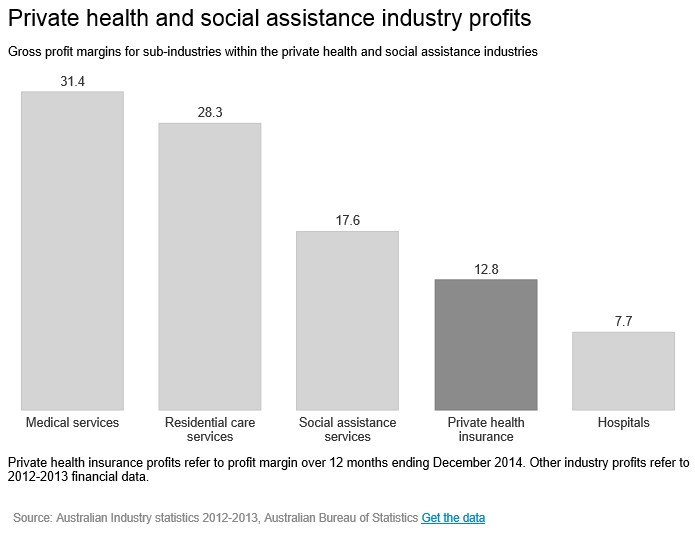

Let’s first look at the gross (pre-tax) and net profit margins, a commonly used measure of profitability. The table below shows the gross profit margins (as net margin data isn’t available) in private health insurance compared with other private health and social assistance industries.

So, the gross profit margin of the private health industry in 2014 is 12.8%, and the net margin is 4.4%. The gross margin is higher than private hospitals (7.7%), and is considerably lower than other sub-industries of private medical services (31.4%) and private residential care services (28.3%).

However, a research paper by the Private Health Insurance Administration Council notes that the profitability of the private health industry is “generally high by historical standards”, with net profit margins in the range of 3% to 6% since 2005. The report also notes that net profit margin is highest for for-profit funds with open enrolment.

In a very different institutional context of the United States health system, the profitability of health insurers has also been a topic of debate surrounding the Obama health care reform. The average profit margin in the US health insurance industry is 3.3%, which is substantially lower than related health care industries.

Impact of the premium rise

The increase in health insurance premiums will undoubtedly place further strains on household budgets. In the short term, higher premiums may lead to some individuals downgrading their cover, or dropping cover altogether.

The policies introduced by the Howard government to support the private health insurance industry (the Medicare Levy Surcharge and Lifetime Health Cover) will still provide strong incentives for individuals to continue to maintain coverage. Medium and high-income earners are often financially better off by taking out private health insurance rather than paying the higher tax rate.

There are, however, two groups that are more likely to feel financial pain from the premium increase. The first are individuals whose potential tax liability under the Medicare Levy Surcharge is only slightly larger than the premium cost.

The second are those whose incomes lie below the surcharge threshold, and choose to buy private health insurance for reasons other than to avoid the tax.

Challenges ahead

Premium increases are closely tied to the growth in benefits expenditure. So it’s important to study the factors driving the increasing use of private hospital care and general treatment services, as well as the prices private providers charge.

Sustained increases in premiums have significant implications on the private health industry, particularly if rising premiums lead to a significant fall in the proportion of the Australian population with private health insurance coverage.

We have gone down this path before. The Medicare Levy Surcharge and rebates for private health insurance were introduced from 1997 to 2001 to reverse the declining membership that resulted then from rapidly rising premiums. These solutions didn’t, and wouldn’t, work.

What Australia needs is to fundamentally rethink about the role of private health insurance, and private health care.

Article by Terence Cheng, Senior Lecturer, School of Economics at University of Adelaide