Social Services Minister, Scott Morrison, has launched a compromise deal to get the Government’s changes to the Aged Pension, announced in the 2014 May Budget, through the Senate.

Instead of indexing the Aged Pension to the consumer price index (CPI) from 2017 – as proposed in the May Budget – Morrison has proposed to undertake a three-yearly review of pension adequacy to allow the Pension to be adjusted above CPI in the event that it doesn’t meet community living standards.

However, there would be no obligation for the Government to act on the recommendations:

“This would be a matter for the government of the day because the government of the day has to be able to consider the broader fiscal issues at play here,” he told reporters in Sydney.

With Labor and the Greens opposing any changes to the Aged Pension, the Coalition is reliant on the support of at least six Senate cross-benchers to pass the plan – support that remains illusive.

Independent Senator, Nick Zenophon – often a good barometer of cross-bench views – has already given the proposal a cold response, branding the plan “problematic”, suggesting the cross-bench will not move in significant numbers to pass the legislation:

“If you have an independent review of pensions with no power to enforce its recommendations, it’s a case of having bark but no bite”…

“Obviously I’ll sit down and talk to the government about it but I’m quite sceptical. It’s quite problematic.”

In my view, Morrison is completely justified in attempting to curb the Aged Pension, which is utterly unsustainable under its current set-up.

Currently, the Aged Pension is adjusted twice yearly by the greater of male average earnings growth or the pensioner cost of living allowance or the CPI.

This means that pensioners get to enjoy income growth that exceeds the growth in average incomes. This is because they receive increases in line with male earnings when income growth is strong and then increases in line with the pensioner cost of living index or CPI (whichever is higher) when income growth is soft, as is likely to be the case over the next few years. If only we were all so lucky!

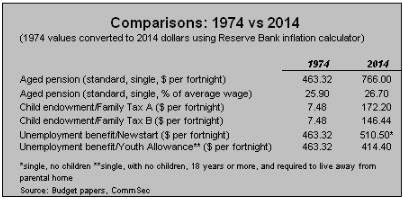

As highlighted by CommSec last year, pensioners have been a key beneficiary of Budget largesse, enjoying a 65% real (inflation-adjusted) increase in the Aged Pension over the past 40 years, with the Aged Pension also growing at a faster rate than wages, increasing from 25.9% of the average wage in 1974 to 26.7% in 2014 (see next table).

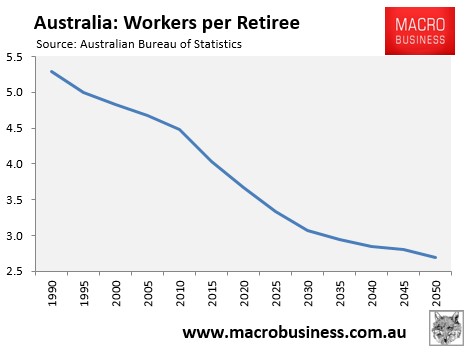

In light of the above, along with the rapid ageing of the population and the declining share of workers supporting the elderly (see next chart), Morrison is right to deem that such generous pension arrangements are neither justifiable nor sustainable.

Put simply, it is wrong to continually increase the tax burden on the working-aged population, just so pensioners can maintain income growth well above the general level of inflation (something not awarded to other welfare recipients), as well as above average earnings growth. Something has to give.

Either indexation arrangements have to be wound-back so that the Aged Pension rate does not increase significantly in real terms, or the eligibility criteria to qualify for the Aged Pension has to be tightened, so that only those that genuinely need it qualify.

Politically at least, it might be easier to focus on the latter approach: focusing on tightening means testing for the Aged Pension, including placing one’s principal place of residence (or part thereof) in the assets test.

It is hard to deny that the Aged Pension is poorly targeted, with far too many wealthy seniors receiving welfare, as illustrated by the below extracts from the latest Intergenerational Report:

A pensioner can continue to receive some payment and the Pensioner Concession Card with assets (excluding their primary residence) up to $771,750 for single homeowners and $1,145,500 combined for couple homeowners. A single person who does not own a home can have assets up to $918,250 and a couple up to $1,292,000 combined and still receive a part pension. A single pensioner can also earn up to $1,868.60 per fortnight (approximately $48,580 per annum) in income and continue to receive a part pension, while a couple can earn up to $2,860 per fortnight combined (approximately $74,360 per annum).

For example:

• Kathleen and Steve are 68, own their home and have $1.1 million in superannuation, shares and bank accounts. They have no other income. They will receive a part-rate pension.

• Liam is 75 is single and has superannuation, an investment property and shares valued at $910,000. He does not own a home and has no other income. He also receives a part-rate pension.

• Lillian is 85, single and lives in her own home worth $1.5 million. She has bank accounts valued at $50,000 but has no other income. Lillian receives a full-rate pension.

Unfortunately, Scott Morrison has already ruled-out counting one’s principal place of residence (or part thereof) in the assets test for the Aged Pension, instead putting forward the ingeniously stupid plan to allow pensioners to sell-off their expensive large homes, pocket the money, but continue collecting the pension.

Therefore, Morrison is left trying to contain the blowout in expenditure by reducing the rate of increase in the Aged Pension, rather than addressing the bigger problem of too many wealthy oldies receiving taxpayer support.

Of course, the situation is not helped by Labor and the Greens, who have shunned pension reform altogether, and seem to think that it’s okay for younger Australians (“generation rent”) to be called on to support their wealthier parents (“generation home owner”) via never-ending tax increases and growing public debt.

It’s a diabolical situation that will need to be resolved sooner or later, one way or another.