It seems you cannot keep a dumb idea down, with Treasurer Joe Hockey reviving Independent senator, Nick Xenophon’s, dumb plan to allow first home buyers (FHBs) to access their superannuation savings to pay a house deposit. From The AFR:

Mr Hockey opened the door to making superannuation more “flexible” – such as by tapping super savings during periods of unemployment, retraining or even property purchases…

“I get a lot of people approaching me saying that young people should be able to use their superannuation to fund a deposit on their first home,” he said on Friday.

Mr Hockey said he was concerned about rising house prices and “accessibility to homes and home ownership for younger Australians. We need to have these conversations.”

Coalition senator Matthew Canavan – a member of the Senate’s economics committee –backed the notion of super for homes, saying Mr Hockey was absolutely right correct to argue for additional flexibility.

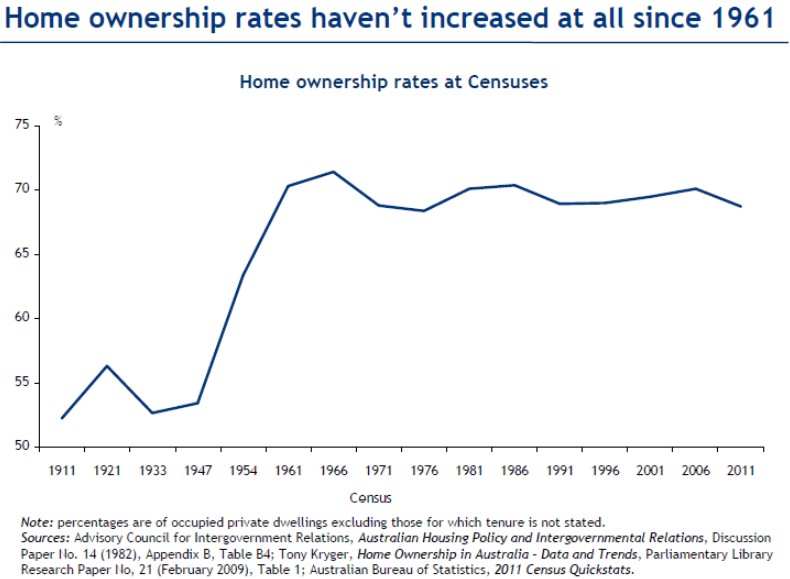

Saul Eslake’s 50 Years of Housing Policy Failure presentation showed us unequivocally that demand-side measures aimed at promoting “housing affordability” and home ownership do not work. Despite the massive decline in interest rates and the myriad of subsidies to first home buyers, the home ownership rate has decreased over the past 50 years (see next chart).

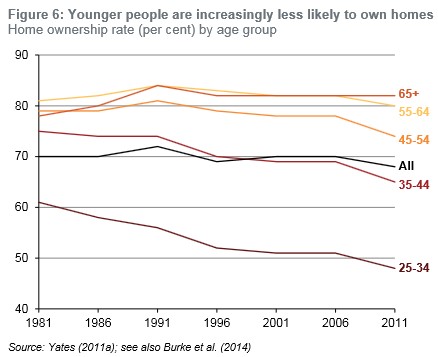

Moreover, home ownership rates have literally collapsed for FHBs:

Under Australia’s constipated planning system, Hockey’s proposal would be self-defeating as the extra capacity to pay would soon be capitalised into higher home prices. At the same time, younger Australian’s retirement savings would be compromised for little additional benefit, potentially placing further strain on the Aged Pension.

Moreover, Canada’s Garth Turner, who oversaw the introduction of a similar system in Canada in the 1990s, has admitted that it was a massive mistake, placing further upward pressure on Canadian house prices and putting at risk retirement savings:

I confess. Once I thought like you [Nick Xenophon]. I even supported realtors years ago when they cooked up this scheme to allow kids to dip into their retirement funds to buy a first home. At the time we were in a steep recession with real estate plunging and the economy in a funk. So, I voted in our Parliament for a temporary program to create the Home Buyer’s Plan in order to stabilize the market and try to revitalize the home-building business. It worked, kinda. Then subsequent governments (a) made the plan permanent and (b) doubled the amount people can suck out of their registered savings.

Now, Nick, we’re reaping the bitter harvest sown when that dumbass legislation passed. Allowing first-time buyers to remove tax-free money to buy a modest home they could not otherwise afford, then restore it to their long-term retirement savings makes perfect sense in theory. In practice and experience, just the opposite.

To date the HBP has been used about 2.5 million times, with roughly $30 billion removed from savings and investments and plowed into real estate. When combined with dirt-cheap mortgage rates (I notice Aussie banks just slashed five-year rates to an all-time low) and voracious, carnivorous bankers, it’s helped push home prices into the clouds. The cost of an average detached house in two of our major cities now exceeds $1 million. (I see median home prices in Sydney rocketed 17% in the past year, to $812,000. So you know what I mean.)

In other words, if you think letting people steal money from their financial futures in order to buy houses today which they really can’t afford is going to make real estate more affordable, you’ve been spending too many evenings with the goat. The opposite is probable. In Canada, it’s fact.

But it gets worse. The evidence also shows when you allow this kind of distorting financial activity to take place, people respond badly. They borrow their brains out, Nicky. Total horniness. As I wrote on this pathetic but repentant blog recently, the kids aren’t even paying this money back – which means we’ve not only goosed houses, increased the risk of a serious correction and skewed the condo economy further – but there are billions less being saved and invested for our pensionless future…

So, buddy, back off. The goal of a caring politician isn’t to shoehorn more people into debt and bad decisions, just because they want it. Instead, your role is to lead, to stand up for common sense, and battle the forces of cheap expediency and sleazy solutions.

If Hockey was truly concerned about home ownership, the best thing he could do is to lobby for an end to policies that distort the housing market and force-up its cost, as he has done with the Government’s tightening of foreign ownership rules. These include winding back negative gearing and removing planning-related bottlenecks, so that FHBs don’t get out-bid by investors and developers are better able to supply housing at a price that FHBs can afford.

unconventionaleconomist@hotmail.com