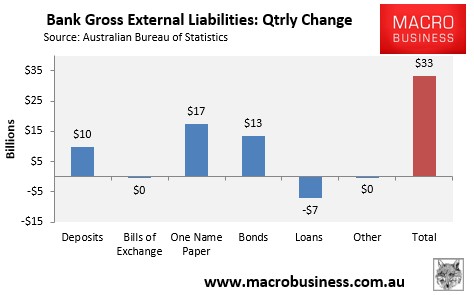

The release of the Australian Bureau of Statistics (ABS) National Financial Accounts yesterday revealed a large $33 billion (5%) jump in Australian banks’ gross external liabilities (offshore borrowings) in the December quarter, with borrowings now at all time record levels.

This surge in offshore borrowings was driven by increases in One Name Paper (+$17 billion) which is debt under one year maturity, Bonds (+$13 billion) and Deposits (+$10 billion), partly offset by falling loans (-$7 billion), as shown in the next chart: