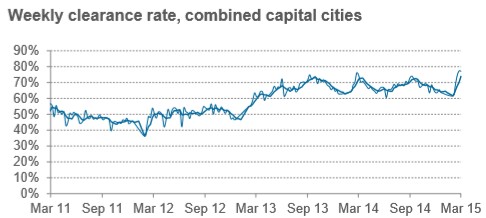

Just when you thought the Great Australian Housing Bubble was running out of steam, the national auction clearance rate delivered another frothy result, driven again by strong demand in Sydney and Melbourne.

The preliminary national clearance rate was a hot 77.1%, just a smidgen under last week’s 77.7% and comfortably above the 74.2% recorded at the same time last year.

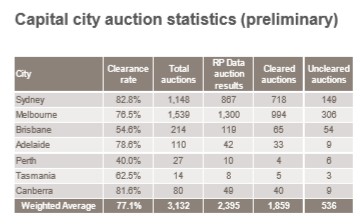

Sydney’s clearance rate fell 5.0% to 82.8%, whereas Melbourne’s rose by 1.6% to 76.5%. Clearances in Brisbane, which typically only has a small number of auctions, fall sharply to 54.6% from 68.9% last weekend. Overall auction volumes were massive (3,132) and up strongly on last weekend’s 2,248.

The Real Estate Institute of Victoria reported a preliminary clearance rate of 79% on 1,275 reported auctions, which was up from the 76% clearance rate on 826 auctions reported last weekend.

For Sydney, Domain (formerly APM) reported a preliminary clearance rate of 85% on 585 reported auctions, which was the same as the 85% clearance rate on 514 auctions reported last weekend.