JP Morgan has a nice discussion today on a topic I’ve been glancing at recently: what exactly is a bubble when yields everywhere are so low?

Investors continue to ask what is really worth buying in a world where everything is expensive and years of easy money must have produced a surfeit of asset bubbles. But where are all these bubbles then? We would like to argue here that world assets are only expensive on a view that markets and economies will return in the not-too-distant future to prefinancial crisis conditions. This is not our view.

An asset is expensive if its internal rate of return (IRR) is below the level it ought to be given its economic and market fundamentals. A bubble is an extreme form of expensiveness, typically driven by speculative momentum, easy money, and leverage. Investors are right to be wary of such bubbles given that the past few business cycles each ended in the bursting of an asset bubble, that the global equity rally is now nearly 6 years old, and that money has never before been so easy. We like to argue that the world is not rapidly enough moving to more normal pre-crisis conditions and that financial assets are thus not in a bubble, even as we pinch ourselves that a bubble must be invisible for it to persist (we did not exactly see the previous ones coming either).

For an asset price to be too high, its IRR must thus be too low. The IRRs (yields) on bonds anywhere in the world are clearly way below any historic mean. Equity yields – the reverse of PE multiples – are low, especially when one recognizes profit margins themselves are well above average in many markets. Asset yields are low both because both the default-free rate and the risk premium over it are low. Assets are thus expensive and may be in bubble territory if the fundamental drivers of safe yields and risk premia are pointing straight up. We don’t think so, but let’s investigate.

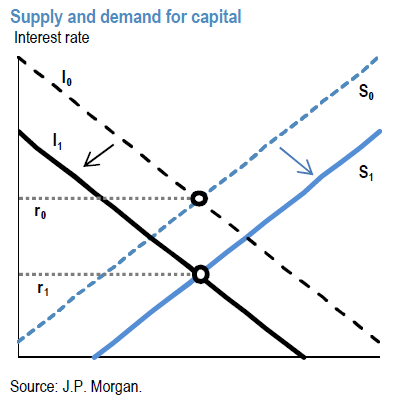

At the most fundamental level, “the” interest rate in the economy is set by the intersection of the supply for capital – saving – and the demand for capital — investment (chart on right). This analyst would argue that both curves have moved to imply lower equilibrium interest rates in this cycle. Numerous research reports have shown that in the aftermath of major financial crises, economic agents go into balance-sheet-repair mode by increasing their saving rates and reducing leverage, irrespective of how much the cost of borrowing comes down. That was the experience in Japan’s deflation of the last two decades. In the US, for example, household saving rates have stubbornly surprised on the upside and are now some 2% higher than past patterns suggest. The fiscal authorities of the G4 have been in systematic austerity mode over the past 4 years. And large financial institutions, central banks excepted, have also been in delevering mode. We are seeing little signs of this behavior changing.

On the demand side, this cycle has been characterized by a surprising collapse in global productivity growth (Chart 2 on right), that is now widely discussed as the “secular stagnation” problem. Ultimately, capital investment represents the return on capital. Low productivity growth implies a low return on investment and thus a low demand for capital. In effect, in this cycle, the supply of capital line has moved out and the demand for capital have moved in, both implying a lower equilibrium interest rate for the world. Central banks keep driving the world bond yield lower, through rate cuts and QE purchases, in a so-far-not- really-successful effort to push growth above trend.

Asset prices can be too high, and yields too low, if risk premia have become unrealistically low. Low global growth volatility and the lack of imminent recession risk suggest macro risk premia should be low now, but inflation volatility and how close we are to global deflation, in turn, suggest somewhat higher risk premia. The onset of Fed rate normalization this summer could also increase uncertainty and thus risk premia.

In short, the global drivers of balance sheet repair and low productivity growth are in our mind holding equilibrium asset yields/IRRs low, and keep us with the view that global assets are not that expensive. Uncertainty, in contrast, could easily rise this year, but probably not enough to create a dramatic repricing of assets. On net, this keeps us long duration in bonds, and OW equities, even as we have reduced this OW to a small position in response to the recent rise in volatility. What will make us more worried about asset repricing and bubbles: a significant upgrading of growth and inflation expectations that will force central banks, led by the Fed, into a more rapid normalization of policy rates.

In short, bad news is good news and so long as interest rates remain subdued the inflation of asset prices is a rational response.

My view is that there are two significant exceptions to this:

- long term low yields (and higher assets) guarantee that interest rate normalisation will be a shallow affair. Put another way, the neutral cash rate is much lower than it used to be and the point at which asset prices come under pressure is also much further down the interest rate curve.

- Australia and certain emerging markets attached to China remain true bubbles because their cost bases have not yet adjusted to this global deflationary reality.