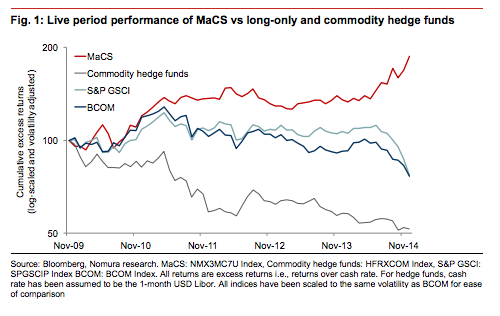

This strategy is based on the view that commodities are more like currencies than equities. Rather than hold long-only positions in liquid commodity futures, the strategy is based on indicators used for macro assets, such as momentum, carry, and slope. The past five years have been turbulent for long-only commodities and many commodity hedge funds. However, MaCS has delivered robust and consistent outperformance over these benchmarks (Fig. 1).The Sharpe ratio of MaCS has been materially higher than that of long-only commodities and commodity hedge funds as shown in Fig. 2. Furthermore, this outperformance has come with lower drawdowns and positive skew.

There is often a tendency to think of commodities as something ‘different’. However, as we argue in this section, commodities are as much of a macro asset class as equities or fixed income. Hence the same principles that hold true for equities and fixed-income investing can also be readily extended to commodities.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.