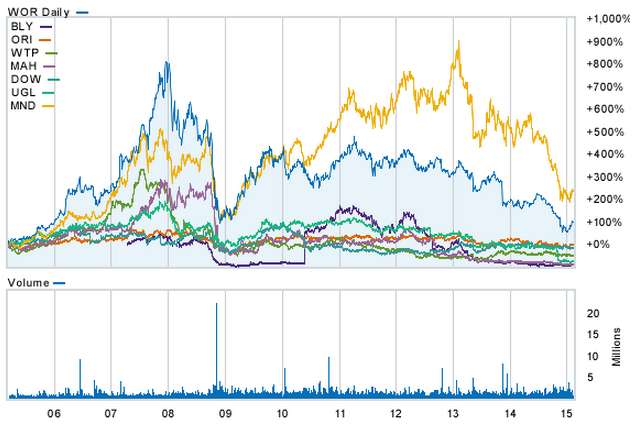

Worley Parsons was Australia’s greatest mining services firm powering to spectacular returns up to 2008 and then running strongly again afterwards (in blue):

But today it’s all over with another dour profit result and, worse, delusional management, from The Australian:

WorelyParsons (WOR) shares drop 11% to a 3-week low of $10.01 after reporting weak revenue growth and disappointing earnings guidance.

FY15 underlying NPAT rose 3.6% to $104 million, but revenue fell 4.7%.

And while second half earnings were guided to be greater than the first half, consensus FY15 earnings of $265 million implies a 1H/2H mix of 39%/61% according to CLSA, which is now very unlikely to be achieved in their view.

“If there was ever a result and company outlook that has little to do with where the share price will be in 12 months this is it: the result in looking back at a world that no longer exists, and WorelyParsons has little visibility,” the broker says.

CLSA reiterates its Sell rating on WOR.

This is the kind of skepticism I expect to see for miners as well before this is over.