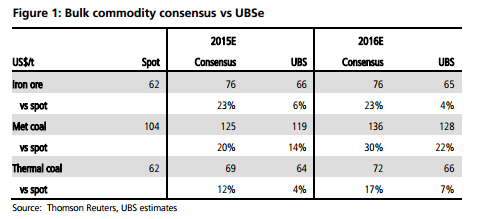

For 2015 and 2016, UBS’s iron ore price forecasts are below consensus. Consensus forecasts are US$76/dmt cfr for both 2015 and 2016, against our estimates of US$66/dmt cfr and US$65/t cfr for 2015/16, respectively. Our more bearish outlook stems from low demand growth (China property slowdown) and a further expansion of low cost supply from the 3 majors, Minas-Rio & Roy Hill. Although we estimate >25% of current production is loss making at current prices; not all of these players will exit (choosing to fight and cut costs instead), prolonging the supply glut. A lower oil price is also expected to flatten and lower the cost curve, adding further downside risk to our price forecasts.

UBS coal prices below consensus too

For met coal, consensus forecasts of US$125/t for 2015 & US$136/t in 2016, are both above UBS of US$119/t & US$128/t, respectively. Spot prices have been drifting lower recently, now US$104/t, outside the 2014H2 trading range of US$110-115/t. Our outlook is more negative than consensus because of ongoing withdrawal of demand from China (50Mt in 2015 vs 75Mt in 2013), supply growth from Australia, a lower A$ which enables Aussies to lower prices, & a lack of US cuts. For thermal coal, consensus forecasts Newcastle spot of US$69/t in 2015 & US$72/t in 2016, above UBS of US$64/t in & US$66/t in 2015/16. Spot has been volatile recently, some benchmarks lifting back towards US$70/t fob. We see this as due to small trades related to the upcoming JFY contract negotiation & bidding by producers for quality coals for blending (China quality compliance). The fundamentals remain weak for thermal prices in our view (China’s various policy moves, a strong USD, low oil price & a lack of supply cuts).

How to play the bulk commodities sector?

The outlook for 2015H1 is a difficult one for bulk equities to perform in the face of ongoing consensus downgrades. In a relative sense, we believe the best placed will be those with low costs and high quality product. In iron ore we prefer BHP Billiton and Rio Tinto, with valuation support and progressive dividend yields of >5%. In the coal space, Whitehaven has high-quality coal products that may attract favourable prices for blending, while the lower A$ contributes to an almost doubling margins and supporting a debt refi.

Even though the analysis is right, the price forecasts are far too bullish (despite being better than the hilarious consensus numbers). The way to play the sector is to short it, or sell and wait for the blood to flow.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.