A sooner than expected decoupling from the Chinese cost curve and growing evidence of cost deflation lead us to downgrade our price forecasts to US$66/61/60/60 over the period 2015-18. In the short to medium term, prices will continue to underperform relative to costs in order to incentivize mine closures and project delays over the period 2015-17. This will unfold while marginal production costs are falling due to weaker commodity currencies, lower input costs and rising efficiency.

At approximately 6% of annual seaborne supply, the scale of the adjustment required each year during the period 2015-17 is testament to both the scale of overinvestment in previous years and the sudden deceleration in Chinese demand. The process to displace marginal iron ore capacity will be shaped by two basic market dynamics. First, prices must undershoot relative to marginal costs in order to incentivize mine closures. Placing a lossmaking mine on care and maintenance involves significant costs that any management team would try to postpone, ranging from the default on supplier contracts and the layoff of employees to the loss of option value on the mine itself.

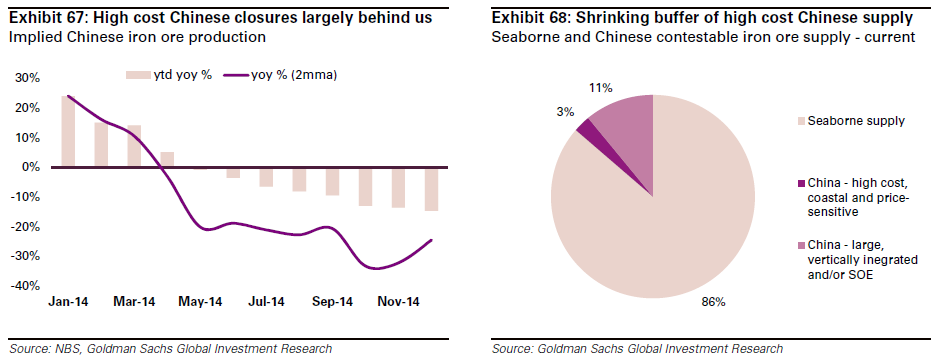

Second, the seaborne and Chinese iron ore markets have decoupled. Until recently, high cost mines in China acted as the marginal supplier and seaborne prices converged towards the Chinese price for domestic concentrate. However, this relationship has broken down. The buffer provided by Chinese iron ore mines that are both high cost and price sensitive provided scant support to prices when the market fell into oversupply during Q2 2014, and now that buffer has largely been displaced. In our view, China should play a less prominent role in balancing the iron ore market in the future and seaborne prices will therefore be determined by competition among marginal seaborne producers.

Wait for it…that’s roughly 80 million tonnes of seaborne displacement per annum for the next three years. That’s a calamitous number and Goldies’ own price forecasts remain far too bullish compared with the reality that they describe so well.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.