In August last year, Treasurer Joe Hockey made headlines for twice claiming on national television that “higher-income households pay half their income in tax”. Hockey was at it again last week when he told Fairfax radio that Australians paid nearly half their incomes in tax:

“When Australians spend the first six months of the year working for the government with tax rates nearly 50 cents in the dollar it is a disincentive,” he said.

“You’re working July, August, September, October, November, December just for the government and then you start working for yourself and your own household income after that for another six months – it is a disincentive.”

Hockey’s claims never passed scrutiny. The existence of the tax free threshold and progressive tax rates up to $180,000 mean that virtually no one in Australia loses half their earnings in income taxes.

That Hockey’s comments are way off the mark are confirmed in a new report by the Australian Council of Social Service (ACOSS), which argues that contrary to popular belief, higher income earners pay on average just 20% of their incomes in tax:

Advertisement

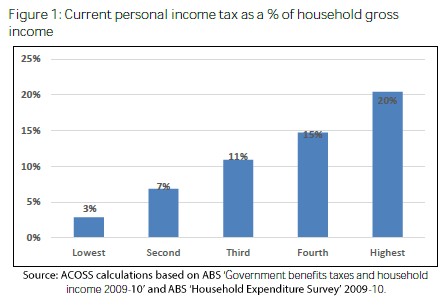

The bottom 20% pays an average of 3% of their income. This is low because for most people the tax free threshold is at least $20,000 and most of the bottom 20% have social security payments as their main income.

The top 20% pays an average of 20% of their income. This is higher due to the progressive income tax scale. Most of the ‘primary’ income earners in these households have incomes above $80,000 and are on one of the top two marginal tax rates (37% and 45% plus the Medicare Levy). However, they do not pay tax on all their incomes at these rates, only ‘slices’ of their incomes above $80,000 and $180,000 respectively, so the tax rate on all of their income is much less than this.

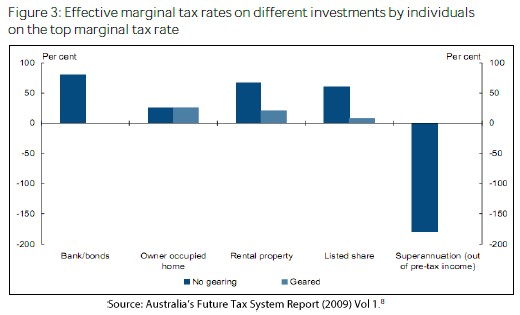

The main reason for the relatively low tax rates applied on higher income earners is that Australia’s myriad of tax expenditures – including superannuation concessions, negative gearing, and capital gains tax concessions – have eroded the income tax base and effectively exempted large swathes of earnings from tax:

…the income tax ‘base’ is narrow – that is, many forms of income are either exempted from income tax altogether or taxed at a lower rate, for example, under superannuation, negative gearing, dividends, capital gains and partnership and trust arrangements…

As Figure 1 shows, the combined effects of the different tax treatment of different forms of income is that the personal income tax system is progressive, but not as progressive as people might think.

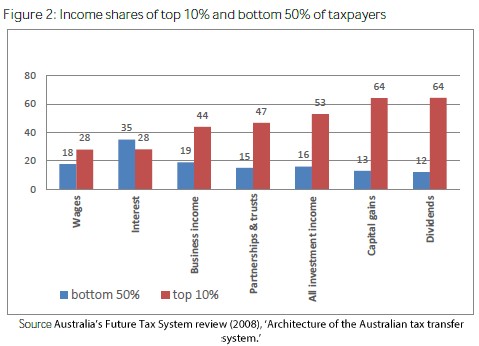

To understand why tax expenditures and loopholes disproportionately benefit those on higher incomes and make the system less progressive, Figure 2 then compares how different forms of income are distributed.

As we might expect, income from investments is more unequally distributed than wages. This applies especially to capital gains increases in the value of assets such as property and shares (64% of capital gains accrue to the top 10% of taxpayers); and dividends from shares (again, 64% of dividends accrue to by the top 10% of taxpayers); and income from partnerships and trusts (47% of which accrues to the top 10%). This is due to both deliberate ‘tax expenditures’ and tax avoidance activities that exploit unintended loopholes in the system…

The problem from both an efficiency and equity point of view is that different kinds of investment incomes are often taxed at different rates for no valid reason. Those mainly received by people with high incomes (such as capital gains) are taxed less than those mainly used by low and middle income earners (such as bank interest). These inconsistencies not only increase income inequality, they distort investment decisions (especially towards speculative investment in asset values)…

Advertisement

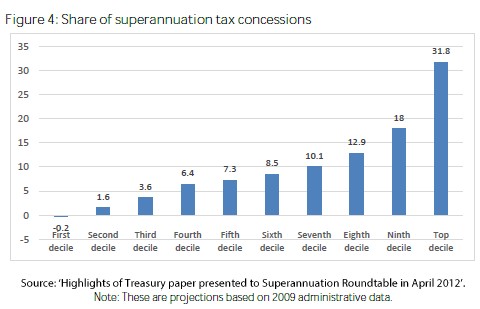

ACOSS is rightfully scathing of Australia’s superannuation system, which has become a mechanism of tax avoidance for Australia’s wealthy, rather than a genuine retirement system:

Some tax concessions are very poorly targeted for their purpose. A good example is the tax breaks for contributions to superannuation. These are usually justified on the grounds that they assist people to achieve an adequate income in retirement, encourage saving, and reduce the cost of the age pension. If these are their main purposes, then they should target people on low and middle incomes, who are less likely to save anyway or have adequate retirement incomes without government support (or compulsion), and more likely to rely on the Age Pension.

Yet, as a Commonwealth Treasury analysis summarised in Figure 4 shows, rather than encourage retirement savings by those on average or low incomes, tax concessions disproportionately benefit the top 10% of taxpayers who receive over 30% of the overall value of these concessions.

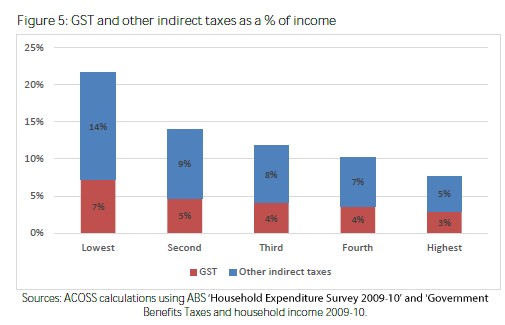

Meanwhile, ACOSS shows that Australia’s indirect taxes, while more efficient than direct taxes on incomes, fall most heavily on lower income households, reducing the overall progressiveness of the tax system:

Advertisement

On average the bottom 20% spend 125% of their gross (before tax) income while the top 20% spend 75% of theirs. This means that a tax on all consumption would fall on 125% of the income of low income households but only 75% of the incomes of high income households…

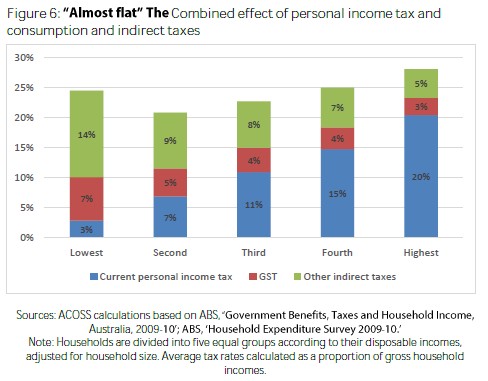

Figure 6 below shows that when the three types of taxes discussed above income tax, GST and other indirect taxes – are added together, their overall effect on households much less progressive than often believed – with a rate, similar to that of a flat rate tax on incomes of around 25% (+ or up to 4 %) on all income groups. The progressive effect of the personal income tax is substantially offset by the GST and other indirect taxes, so that:

1) The bottom 20% pays an average of $129pw or 24% of their income.

2) The top 20% pays an average of $1,006pw or 28% of their income…

ACOSS’ analysis highlights, once again, why the Coalition Government is misguided on tax. If it genuinely wants to reform entitlements and improve the the Budget, it should cut into higher-income welfare, such as superannuation tax concessions and negative gearing. Reforming these tax lurks would deliver substantial Budget savings while improving the overall progressiveness and equity of the tax and welfare systems.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.