by Chris Becker

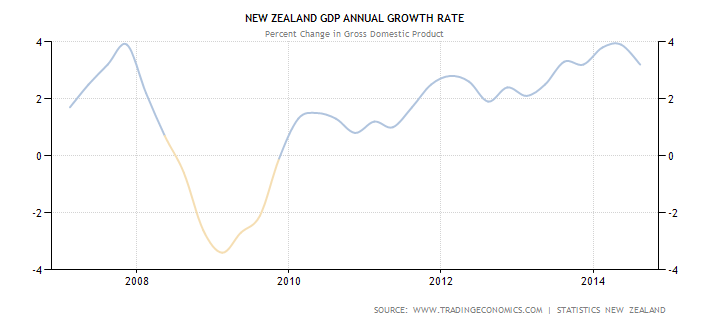

New Zealand’s economic growth in the third quarter of 2014 was slightly higher than expected at 1% versus 0.7% but annualised dipped to 3.2% from 3.9% in the last quarter:

While a very good result (one Australian Treasury officials would love to have) it might forestall PM John Key’s planned return to surplus this financial year, which recently had been pushed out by a year. This is of course a political goal not an economic one as the Kiwis have the same delusional focus on “surpluses forever” as the Australian economic/political quango when both nations need to be running deep deficits to fund infrastructure and domestic investment post-mining boom.

Where did most of the growth come from? Like Australia, the NZ economy is dominated by primary industries with both agriculture and mining providing the bulk of the growth output with households also increasing their spending with the highest increase since before the GFC.

More from NZ Treasury via interest.co.nz:

Treasury said weaker inflation, lower interest rates and a slump in the dairy payout had reduced forecast tax revenues, despite an increase in the economic growth outlook.

Treasury forecast the nominal size of the economy would be NZ$13.2 billion lower over the next four years because of that lower inflation, which would drag on expected GST, income tax and resident withholding tax revenues from term deposits

Westpac economists said the risks were for even stronger growth and lower inflation than Treasury was forecasting, which could endanger the surplus in 2015/16.

“Oil prices have fallen much further than the Treasury assumed when it finalised its forecasts last month. A sustained fall would mean lower inflation, lower wage demands and lower interest rates than forecast, which all point to lower Government revenue,” they said.

That’s some nice risks to have in a restructuring post-Christchurch earthquake environment although the housing bubble in Auckland that has effected the rest of the nation and lack of genuine reform past initial macroprudential controls will still weigh in the medium term.

There has been no move in NZ’s sovereign rating with Moody’s still stating the AAA remains as net government debt is projected to remain well below the arbitrary (and somewhat ridiculous) 30% threshold.

From WSJ:

“We are very comfortable with our ratings stance at this point,” said Mr. Hess. “The magnitude of the deficit [in the year to June 2015] is really small and everything is moving in the right direction,” he said.

The Treasury’s half-year economic and fiscal update show the government will post an operating deficit before gains and losses of 572 million New Zealand dollars (US$446 million) this financial year versus a small surplus of NZ$297 million forecast in a pre-election update last August.

Finance Minister Bill English said Tuesday the aim is still to bring it down to 20% by 2020 and “we think, barring some other big shock, they can do that,” said Mr. Hess.

He said that one of the uncertainties continues to be the high exchange rate and that inflows of foreign capital from abroad to finance the current account deficit is “the major vulnerability we see for New Zealand.”

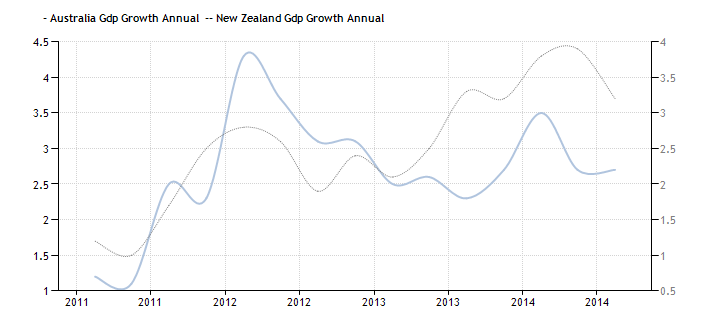

For Australian investors todays result is likely to see AUD move closer towards parity with the NZD, as the rate differential between the two nations is likely to widen. The RBA will cut again next year while the RBNZ holds fast as economic growth diverges (note the chart below Aust GDP is right Y-axis and is forecast to be below 2% in 2015):

AUDNZD dropped below 1.05 for the first time since a quick visit in January this year on the release this morning and remains under strong selling pressure.