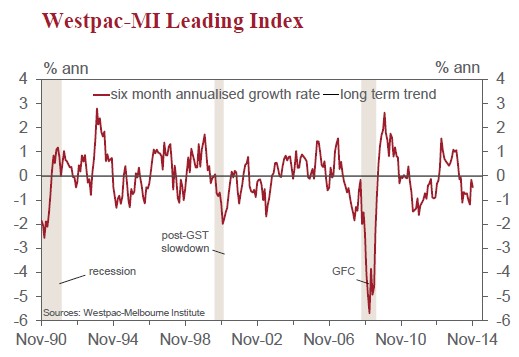

The six month annualised deviation from trend growth rate of the Westpac Melbourne Institute Leading Index which indicates the likely pace of economic growth three to nine months into the future fell from –0.15% in October to –0.47% in November.

This is the tenth consecutive month where the growth rate in the Index has been below trend. That follows thirteen consecutive months to February this year when the growth rate was above trend. The index continues to indicate that we can expect growth in the Australian economy to stay below trend in the final quarter of 2014 and well into 2015.

Indeed, following the release of the September quarter national accounts we have revised down our growth forecasts for the next three quarters. We had been expecting the annualised growth pace in private demand over the three quarters from December 2014 to June 2015 to be 2%. This has now been downgraded to 1.2%. With net exports still providing a solid boost to growth, GDP is still forecast to run ahead of private demand. However, we have also revised down our annualised GDP growth forecasts over that period from 3.2% to 2.7% – from trend growth to markedly below trend.

We still expect that growth momentum in the second half of 2015 will be around 3.2% reflecting the impact of rate cuts in the first half of 2015; an improving world economy including some lift from a modest improvement in the terms of trade, and the benefits of a much lower AUD than had previously been factored into our thinking. Of course, the Leading Index (being below trend for the last 10 months), had already been signalling that weakness.

Over the last six months the index’s growth rate has remained at a below trend growth pace. In June, when the index’s growth rate was 0.74% below trend, the key drivers were: the RBA commodity price index in AUD terms (–0.74ppts); the yield spread (–0.27ppts); and the Westpac –MI Consumer Sentiment Expectations index (–0.19ppts). Offsetting those negative effects were US industrial production (+0.26ppts) and aggregate monthly hours worked (+0.25ppts). The Westpac MI UE index; dwelling approvals; and the ASX 200 had minimal impact on the growth rate.

The Reserve Bank Board does not meet again until February 3. With official growth forecasts of below trend growth in 2015; well contained inflation pressures and an overvalued AUD the case for rate cuts seems respectable. Indeed on December 4 Westpac revised its rate forecast for two consecutive 25bp cuts in February and March. In the minutes to the Board’s meeting on December 2 it was noted that the Board discussed lower rates in the context of market pricing pointing to some chance of a cut. However, recent missives from the Reserve Bank indicate that the Governor is most focussed on boosting confidence and has questioned whether cutting rates might send the wrong signal. On the other hand, he does acknowledge that low inflation might be a positive reason to ease policy.

The Governor’s comments are discouraging for our call for an early cut. Nevertheless, the next meeting is six weeks away. February is always a better time to move policy than March (which is favoured by markets) because it coincides with the Bank’s quarterly Statement on Monetary Policy which allows the Bank to explain its decision. We are retaining our rate call given that much can change over the next six weeks.

I agree with Evans’ call for further rate cuts, although the timing is uncertain. But as for his view that the Aussie economy will rebound significantly in the second half of 2015 on the back of “the impact of rate cuts in the first half of 2015; an improving world economy including some lift from a modest improvement in the terms of trade, and the benefits of a much lower AUD”, I disagree. If anything, the country that matters most to Australia – China – will weaken further, as will commodity prices and the terms-of-trade, not to mention the ongoing falls in mining investment.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.