Westpac has released its Coast-to-Coast report, which provides an update on Australia’s state economies. The report provides some interesting analysis showing that New South Wales is driving demand and consumption nationally on the back of its booming housing market:

Economic conditions softened in the September quarter and growth remains uneven. These two points are clear from an analysis of the state economies.

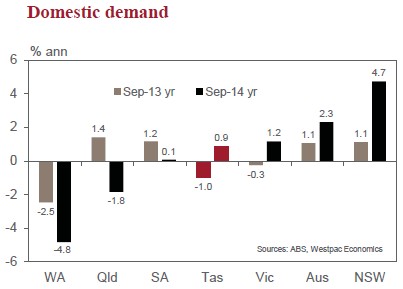

Nationally, domestic demand contracted by 0.3% in the quarter and annual growth slowed to 0.9%. NSW was the only state to record an increase in final demand in the quarter, up a sharp 1.3%. Tasmania and South Australia experienced flat demand, while sizeable falls were recorded for Victoria, WA and Qld.

Key negatives in the quarter were: mining investment; an unexpectedly sharp dip in public demand and an income squeeze from the falling terms of trade.

In Q3, weakness in Victoria and Tasmania was exaggerated by a slump in public investment, directly subtracting around 1.4ppts off state demand. More generally, only in NSW has public demand added to growth over the past year.

Wage incomes, with the exception of NSW, are under pressure against the backdrop of sluggish labour market conditions, the downturn in mining investment and a declining terms of trade.

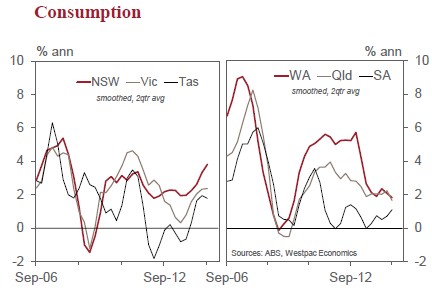

Consumer spending in the mining states of WA and Qld, where population growth is slowing, has been on a more modest growth path in 2013 and in 2014. Per capita spending is flat in Qld and declining in WA. In the southern states of Victoria and South Australia, structural change has been a key theme. Consumer spending has improved moderately in Victoria, as the savings ratio adjusts lower, while in SA per capita spending is flat. By contrast, in NSW, where population growth is accelerating and is above trend, consumption has strengthened to a well above trend pace. Tasmania also experienced an acceleration in consumer spending in 2014 as home building activity rebounded sharply.

Going forward, while consumer spending momentum and overall economic conditions will continue to be constrained by the mining investment downturn, there are some potential positives.

We anticipate a policy response, in the form of interest rate cuts by the RBA early in 2015. In addition, a partial adjustment in the currency is underway. The Australian dollar, currently around US82¢ is 10% lower than in the September quarter and 20% down on the start of 2013. This will provide a much needed boost to the competitiveness of trade exposed sectors. Also, international conditions will become more supportive in 2015, with world growth strengthening and the terms of trade stabilising.

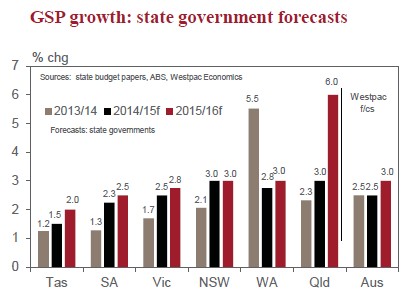

Each of the state governments, with the exception of WA, anticipates an improvement in state output in 2014/15 and a further improvement in 2015/16. This is premised on the key factors that we have identified, namely: particularly expansionary monetary conditions; a lower dollar; and a stronger world economy. This will lead to an improvement in consumer spending, although the risk is that building activity loses some momentum. Business is likely to respond to stronger demand, locally and globally, lifting spending on equipment investment, from low levels, and expanding employment.

As noted this morning, I strongly disagree with Westpac’s view that the Australian economy will rebound to above trend growth from the second half of 2015. The country that matters most to Australia – China – will weaken further, as will commodity prices and the terms-of-trade, not to mention the ongoing falls in mining investment. Then there is the closure of the local car industry by 2017, which will smash the Victorian and South Australian economies, in particular.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.