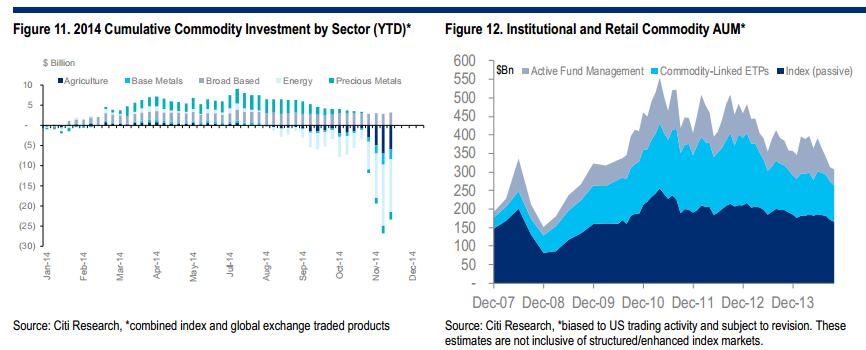

Retail and institutional commodity assets under management estimates for October suggest a 2% drop m/m and 20% decline y/y to c$307Bn (not inclusive of structured/OTC products) and we expect final November data will send this figure below c$300Bn for the first time since 4Q’09. Such a level would be at least c$255Bn shy of the recent commodity AUM peak in April 2011 during the height of the Libyan civil war and MENA spring. The total gross market value of OTC commodity derivatives have plunged nearly c$390Bn since the 2007 pre-Financial Crisis high to c$270Bn at the end of 2Q’14. Final 2014 annual data are likely to show that this level will be significantly lower. Stricter capital requirements, investors shifting to exchange-traded and cleared products for vanilla commodity transactions and fewer dealers in the space have significantly curtailed the amount of notional contracts outstanding for OTC commodity derivatives from a 2007 peak of c$8.3Tn to around c$2.7Tn since 2010 (see: Doshi, Aakash “OTC Commodity Derivatives: A Changing Market Structure.” Citigroup: 19 June 2012).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.