Over the weekend, VOX published interesting research paper examining long-run house price trends across 14 advanced economies and some of the reasons behind the rapid global escalation of house price costs since the 1970s.

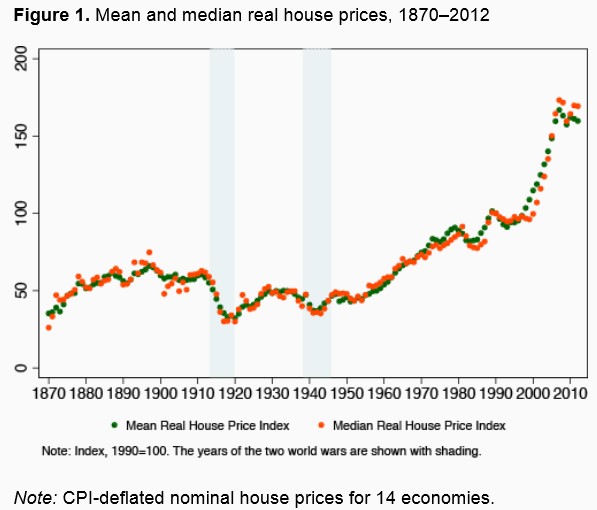

First, the paper presents the (unweighted) mean and median of the 14 house price indices since 1870, which shows that “house prices in the early 21st century are well above their late 19th-century level, and increased in all advanced economies in the long run”. It also shows that house prices have exhibited “a hockey-stick pattern” whereby “real house prices remained broadly stable from the late 19th century to the mid-20th century, and increased strongly in the following decades”. The end result is that “real house prices have approximately tripled since 1900, with virtually all of the increase occurring in the second half of the 20th century” (see next chart).

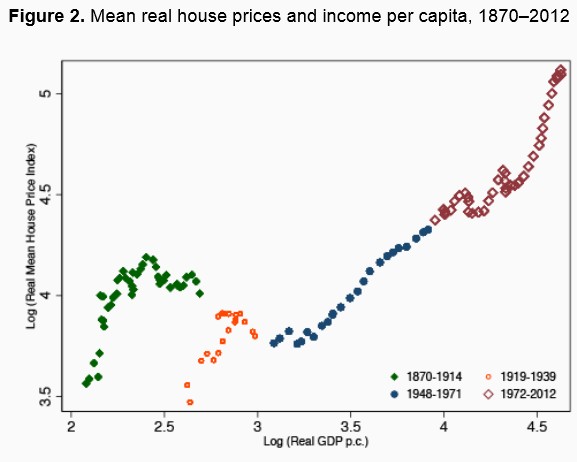

House prices have also outpaced incomes, particularly over the past few decades (see next chart).

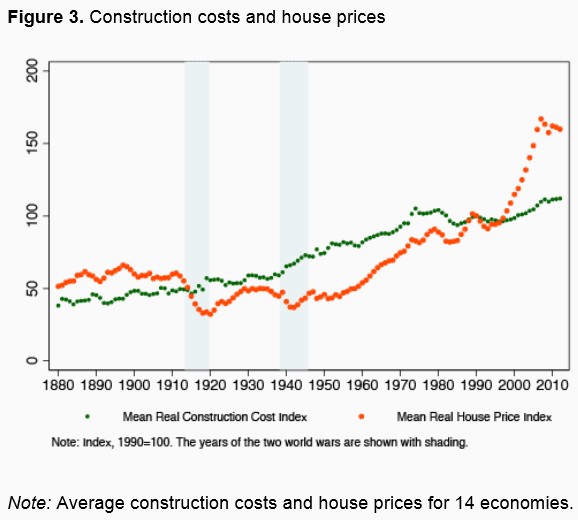

As has been frequently argued on this site, the paper attributes the lion’s share of the growth in house prices to escalating land values, rather than construction costs:

While construction costs have flat-lined in the past four decades, sharp increases in residential land prices have driven up international house prices. Our decomposition suggests that up to 80% of the increase in house prices between 1950 and 2012 can be attributed to land price appreciation alone.

The paper pins the escalation of land prices globally on a cocktail of demand and supply-side factors:

From the 19th to the early 20th century, the transport revolution – mostly the construction of the railway network, but also the introduction of steam shipping – led to a massive and well-documented drop in transport cost. An important side effect of the transport revolution was to substantially augment the supply of economically usable land.

…this land-augmenting decline in transport costs subside[d] in the second half of the 20th century, so that land increasingly became a fixed factor.

At the same time, zoning regulations and other restrictions on land use also inhibited the utilisation of additional land in recent decades, while rising expenditure shares for housing services added further to rising demand for land. Yet our stylised facts are also compatible with other explanations that help explain surging land prices in the past few decades, such as growing subsidies for home ownership or easy borrowing condition…

The paper’s conclusions are correct, in my view. While the escalation of house prices has been largely a global phenomenon, markets that have had 1) liberal land supply/planning and/or 2) have not juiced demand via tax incentives or easy credit, have tended experience far less price appreciation.

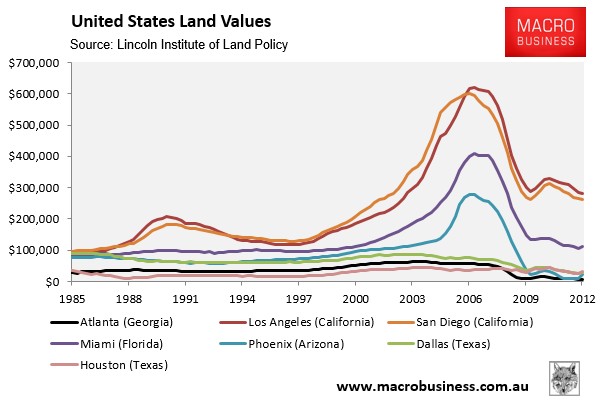

Examples of the former include many markets in the US where there are few regulatory or geographical constraints on land-use, such as Texas and Georgia. There, land/house prices remained relatively stable and affordable, when compared against the supply constrained “bubble” markets, even in the lead-up to the US housing bubble (see next chart).

Germany is another market that has bucked the global trend (for reasons explained previously). There, house prices have remained roughly stable since the early 1970s in real terms, despite strong growth in incomes and positive population growth until 2006.

Obvious policy lessons arising from the paper are to remove artificial restrictions on land-use and planning, remove policies that artificially raise demand, such as tax concessions (negative gearing) and subsidies to first home buyers, as well as facilitating the adoption of ‘telecommuting’ so that workers no longer need to travel to a central location for work.

Expensive land/housing is not a fait accompli, but rather the manifestation of poor policies on both the demand and supply-sides.