Market dynamics change faster than expected

The changes in market dynamics following the shift to oversupply have come earlier than we expected. In particular, the period when marginal iron ore mines in China provide some support before the inevitable decline to sub US$80/t prices appears to have ended prematurely. Rather than gradually eroding the linkage between seaborne and domestic iron ore prices over a two-year period, the two markets have effectively decoupled in a matter of months. As the buffer of high-cost, price-sensitive mines in China is depleted and the Chinese cost curve becomes less relevant to the price outlook, the focus is shifting to the growing competition between seaborne producers.

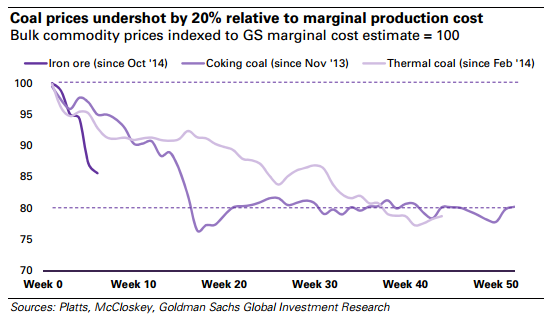

The precedent set by coal suggests further downside

Other bulk commodities further ahead in the supply cycle provide a useful reference point for the iron ore outlook. In the case of coal, the trough came in roughly 20% below our estimates of seaborne marginal cost for both thermal and metallurgical coal. However, the scale of supply growth and the pace of the price decline to date have been even greater in the case of iron ore. Our price forecasts remain unchanged partly due to the uncertainty related to recent Chinese statistics, but we believe the risks are clearly skewed to the downside. The need to incentivize mine closures and project delays ex-China will be the main price-setting mechanism during 2015-16, in our view. Over that period, we estimate that up to 130Mtpa of seaborne capacity will have to close, equivalent to 10% of current supply.

That’s roughly a $60 non-forecast with everything above FMG dead on the cost curve and probably Cloudbreak as well. A good base case.

I’m more bearish given:

I expect Chinese production to hold up better;

Chinese steel production to peak next year;

the iron ore surplus will dwarf that in coal;

cost-out to keep everyone alive too long as the price deck keeps falling;

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.